Scott Maddock

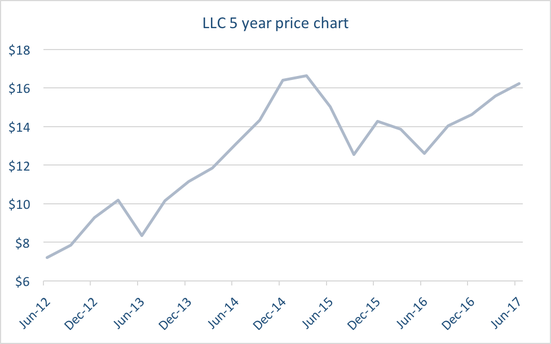

LLC is a leading development, construction and investment management business, operating in 9 countries. We believe the company is positively leveraged to global economic activity. Operationally the company has been on a path of continuous improvement since their last major construction losses in 2004. Delivering a strong operational track record, generating 14% ROE. We expect LLC to have net cash within 18 months (5% gearing currently).

The current dividend does not seem high at first glance; however, LLC has a history of paying excess cash to shareholders – notably following the sale of a major Shopping Centre development for $1.3bn in the UK in 2014. We feel LLC will have the opportunity to deliver more cash to shareholders as current projects mature.

The Australian housing cycle is a fixation for most of us and we assume all our readers have a strong view regarding the near-term path of housing prices. We feel it’s clear that as housing construction activity peaks in Sydney and Melbourne this year, that housing prices will also peak. This process is assisted by controls on bank lending – both internal and those imposed by the bank regulator, APRA.

In this context, many would say LLC is a risky investment – and that’s true to an extent – contracting and construction businesses have inherent risks which we do consider. However, the housing cycle is less of a risk than you would think at first glance;

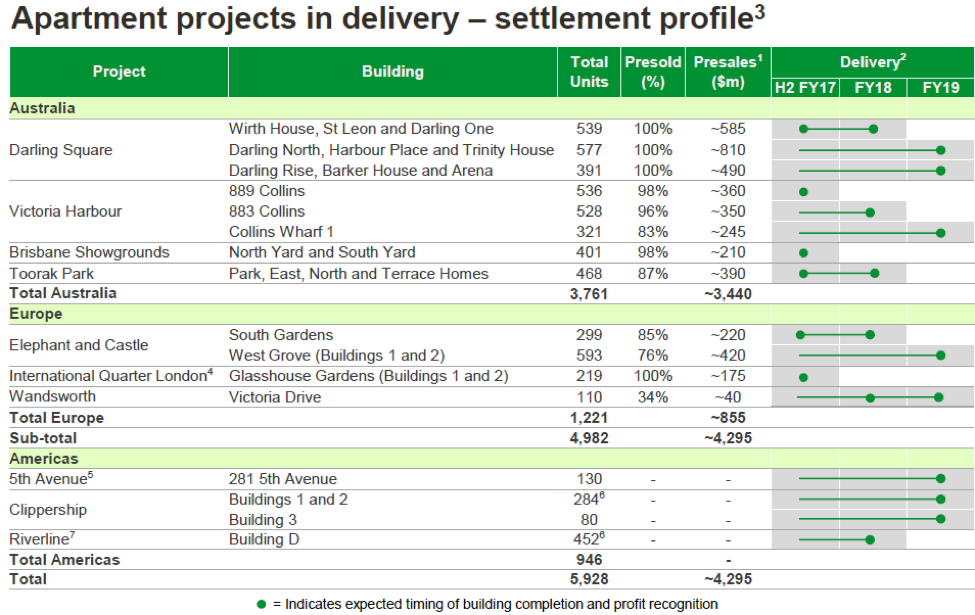

- LLC’s exposure to Australian apartment earnings peaks this year at only 20% of group earnings.

- Developments are 80-90% (and higher) pre-sold and most purchasers (especially from overseas) are holding a significant unrealised profit. This suggests there will be a low final payment default rate as buildings are completed.

- Even during the GFC both LLC and Mirvac Group observed less than a 3% default rate, recently defaults are running at less than 1%.

- Lend Lease’s apartment construction business includes projects in the UK and USA, further diversifying the sources of likely cash flow.

In summary, our investment thesis is that LLC has invested ahead of the economic cycle, has significant pre-sold revenue for work in progress, with buyers having paid 10% deposits and sitting on capital gains – therefore significant defaults or losses for LLC are unlikely. We expect that as most projects are finalized during the next twelve months (see table) we will see significant cash generated. Since LLC has relatively low levels of debt, cash should be available to increase dividends or potentially allow a capital return.

We believe valuation remains attractive vs. history and global peers, on a 12x forward PE vs 17x for similar global listed construction companies. LLC is likely to deliver more cash to shareholders along with a positive share price return.