Alphabet (GOOGL.NASDAQ)

Quickly touching on YouTube, Google bought the company in 2006 for $1.65bn USD. Since then, YouTube has become the second most popular website in the world. That $1.65bn is probably a small figure compared to what YouTube would attract if it were spun off today. YouTube is a unique asset in the sense that their business model is extremely tough to copy and anyone that tries to compete with YouTube can simply be copied or absorbed. Another feature of YouTube is that they can scale their service (add more users) and hardly increase their costs in doing so. The key revenue drivers for YouTube are its premium subscription service and Google Ads. YouTube-displayed ads currently account for around 10% of Google’s revenue.

Waymo

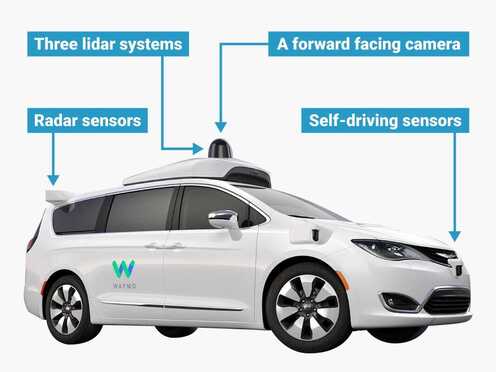

Waymo was first founded in 2009 as “Google’s self driving car project”. Waymo have developed the software that operates autonomous vehicles using, amongst other things, lidar systems and sensors. Since launch they have already achieved Level 4 autonomy. This means they can operate vehicles with full autonomy but with a few restrictions, such as weather and road conditions. Last year they launched Waymo One, a fully driverless ride-hailing service. This is an operation that means anyone in Phoenix with the Waymo app can hail a fully autonomous ride at the tap of a button. Competing with the Ubers and taxis of the world isn’t all Waymo is doing, they currently have a few segments to their business. They aren’t just looking to drive people, they are also looking to grab a piece of the commercial market through trucking, postal services and pizza delivery. Waymo was an early mover in the driverless car space and has made a lot of progress already having tested autonomous vehicles in 25 cities across the US. More recently, Waymo launched Waymo Via which is developing an autonomous trucking solution (directly addressing a pressing issue in the current environment given the US’ truck driver shortage).

Context: Aurora

There has recently been news of fellow autonomous tech company Aurora going public via a SPAC deal at a valuation of around $11bn. They are a fair way behind Waymo in terms of their capabilities (e.g. they haven’t reached Level 4 autonomy yet) and they have no existing operations, having only been founded in 2017. These kinds of deals show that the sector is beginning to heat up while also highlighting what Waymo could be worth as a stand-alone company. Given how far behind Aurora is and the extent of Waymo’s existing operations, it is certainly well north of $11bn.

Amazon (AMZN.NASDAQ)

Automation

Looking at Amazon, there is a huge opportunity to inject further automation (not entirely in the mobility sense either) into their business model, notably the e-commerce side. It will be a step function change in terms of their cost structure. Logistics is by far Amazon’s biggest expense. Any opportunity they get to automate anything, whether it’s picking within the warehouse, moving a package from warehouse to warehouse with autonomous systems, or anything along that front is going to be a step function change in their operating profit. We think that this development is something that the market is not paying attention to whatsoever. And that’s just one aspect of the business.

AWS

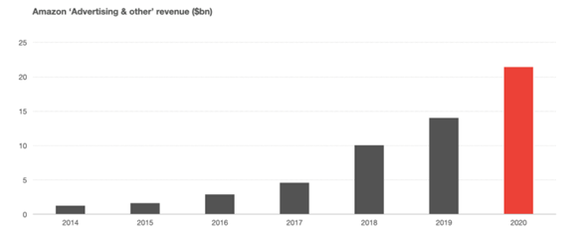

The other big aspect of the business is obviously AWS, their profit centre. AWS is providing on-demand cloud computing platforms and APIs to individuals, companies, and governments, on a metered pay-as-you-go basis They’re not getting credit for this business whatsoever and, in terms of it fitting within our mobility theme, Cloud solutions/technology in general is something that fits perfectly within the first pillar of sharing and connectivity, we consider it the network layer. Cloud infrastructure is critical, particularly as we talk about edge computing, and having vehicle to vehicle, vehicle to infrastructure, basically just low latency connections. As Cloud scales, Amazon is obviously the leader there. All of the Cloud players – Amazon, Microsoft, and Google – have autonomous efforts. They know that autonomy is going to be huge and, simply put, having Cloud in house when you also have autonomy is a significant advantage.

Zoox

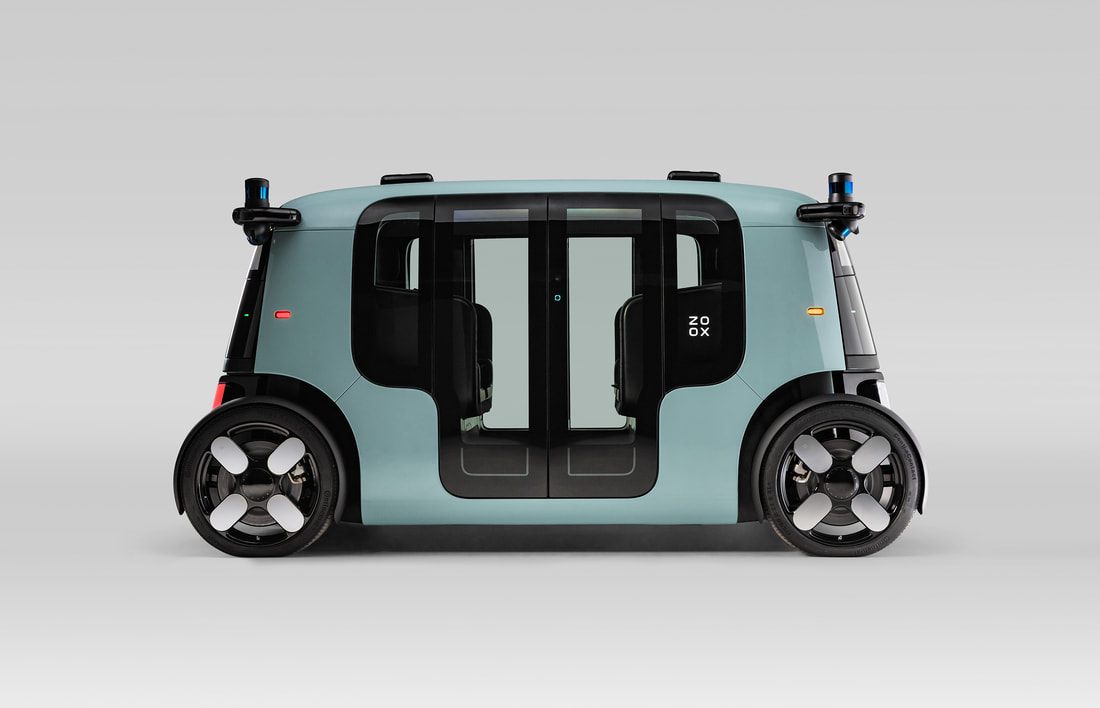

In 2020 Amazon acquired Zoox for approx. $1.3bn USD. Zoox is an autonomous vehicle company looking to reinvent personal transportation. Like Waymo, Zoox will provide mobility as a service in dense urban environments; they will handle the driving, charging, maintenance and upgrades for their fleet of vehicles. Riders will simply pay for the service. This is a key difference between these new autonomous solutions and the Ubers of the world. Amazon is a unique and growing company that uses its vast platform to disrupt any new business it enters; we saw what happened when Amazon bought Whole Foods, Walmart and Target took a big hit in market value. We can see them having the same impact in the autonomous driving industry. Zoox is something Amazon is getting negligible credit for. And that’s understandable. They’re a bit further behind in terms of the competition. But in terms of the opportunity set, it’s a massive one. And that’s not to mention anything else that Amazon has going on whether it’s pharmaceutical or Amazon Go, which is basically automation and something that we believe they’re going to probably license out over time and it will become a very high margin product.

Regulation

A risk that is commonly spoken about regarding the FAANG stocks is the perceived regulatory risk. There has been talk that regulators will step in and break up the Amazon’s into smaller entities, such as spinning off the AWS business, but so far it’s been a losing battle for lawmakers as they haven’t been able to force any of these changes yet. However, if Amazon or Google were to be broken up, we believe they would become more valuable as the market prices the spun off entities properly. It is relatively common for excellent companies with many different segments to be undervalued.

Thesis

Both Google and Amazon are pioneers in their respective fields but we believe these businesses are misunderstood and the market isn’t giving them enough value for their subsidiaries that would be worth a lot more as stand alone businesses. Both AMZN and GOOGL are investing in long term plays that create value for shareholders, e.g. AWS and YouTube, but we think their autonomous vehicle investments, Waymo and Zoox, may be their best ones yet.

Rewinding back to the early 2000s, Amazon was spending hundreds of millions of dollars on capex to build out AWS for years. It was a massive expense, very capital intensive and a huge drag on free cash flow. All the corporates, their potential competitors, thought they were crazy. They didn’t understand it, so they ignored it. And so, for years, they allowed AWS to take a huge lead in a multi hundred billion dollar plus market with literally no competition. Fast forward to today and it’s a business probably worth about a trillion dollars and Amazon is the clear leader of the pack. That’s how we expect these autonomous units to be viewed, big cash drags that are given negative to no value. Today, Google is given no value for Waymo. One day the market will catch up and quickly recognise how transformational it is.

|

Disclaimer: AMZN & GOOGL are held as a long positions in TAMIM’s Global Mobility portfolio. The TAMIM Global Mobility strategy seeks to to capitalise on the ongoing $7 trillion autonomous and electric vehicle revolution.

|