By Ron Shamgar

In investing, there are moments when the market slowly recognises value and rewards patient shareholders. Then there are moments when value is crystallised suddenly through corporate action. The recent takeover proposal for ClearView Wealth (ASX: CVW) sits squarely in the second category.

ClearView has long been a fascinating case study in the Australian small and mid cap insurance landscape. For years the company traded at a discount to its underlying economics. Investors often struggled to reconcile the company’s improving operational performance with the modest valuation placed on the stock by the market.

![]()

That dynamic shifted meaningfully in the last month following the announcement that Zurich intends to acquire ClearView via a scheme of arrangement. The proposal values the company at 65 cents per share in cash, with the possibility of a fully franked dividend worth up to 5 cents per share, delivering approximately 2.14 cents of additional franking credits to shareholders.

The announcement arrives alongside ClearView’s strong first half FY26 results, which highlight just how much operational momentum has been building within the business. While the takeover proposal has understandably captured investor attention, the underlying results tell an equally important story about the company’s progress and the strength of the life insurance franchise it has built.

A Business That Has Been Quietly Improving

ClearView’s first half FY26 results illustrate a company gaining momentum across multiple operational fronts.

New business sales rose by an impressive 29 percent to $21.0 million. This growth reflects both stronger distribution relationships and increased competitiveness in product offerings. Life insurance distribution in Australia is a highly competitive space, where advisers and brokers have many product providers to choose from. For ClearView to deliver this level of growth suggests the company’s offering is resonating increasingly well with the adviser community.

Market share gains appear to be following. Management estimates that ClearView’s share of the new business market has increased by roughly 10 to 11 percent, a notable shift in what is typically a relatively stable industry structure.

Importantly, this growth in new sales is not simply a one off spike in activity. Life insurance businesses benefit from recurring revenue dynamics once policies are written. As new policies are added, the base of in force premiums expands, creating an annuity like income stream over time.

This dynamic is clearly visible in the numbers. In force premiums increased 13 percent to $436 million. This figure represents the company’s annual recurring premium base and is a critical indicator of long term earnings power within the business.

Gross premium revenue followed a similar trajectory, also rising 13 percent to $215.6 million for the half. This growth reflects both new policy additions and strong policy retention. In a sector where customer retention is essential to long term profitability, these figures point to a business with improving underlying health.

Claims Stability Supports Earnings Visibility

Insurance companies ultimately succeed or fail based on the balance between premiums collected and claims paid. ClearView’s claims experience during the period remained stable and well within management expectations. The company reported a gross claims loss ratio of 51 percent, broadly consistent with its long term average of around 52 percent.

This level of stability is particularly important for investors analysing insurance businesses. Claims volatility can materially impact profitability, especially for smaller insurers with more concentrated policy books.

The fact that ClearView continues to deliver claims ratios aligned with historical averages suggests that its underwriting standards remain disciplined. It also supports the view that the company’s earnings profile is becoming more predictable as the policy base matures and expands. In simple terms, the company is writing profitable business and managing risk effectively.

Earnings Growth Accelerates

One of the most striking aspects of the first half results was the magnitude of earnings growth. Life insurance underlying net profit after tax increased by 59 percent to $24.1 million. At the group level, underlying net profit rose 77 percent to $22.1 million. This growth reflects a combination of expanding premium revenue, stable claims performance, and operating leverage within the business model.

Insurance platforms benefit from scale. Once the fixed cost base is established, incremental policies can be added with relatively modest increases in operating expenses. As a result, revenue growth tends to translate into faster earnings growth over time.

ClearView’s results demonstrate this dynamic clearly. Underlying earnings per share increased 84 percent to 3.5 cents for the half, highlighting the strong operating leverage embedded within the business. For long term investors who have followed the company over several years, these results represent the culmination of a multi year effort to reposition and strengthen the business.

Balance Sheet and Embedded Value

Another area worth highlighting is the company’s balance sheet and underlying economic value. ClearView reported surplus capital of $11.3 million at the end of the half, alongside total net assets of $348.4 million. On a per share basis, this equates to approximately 55.9 cents per share.

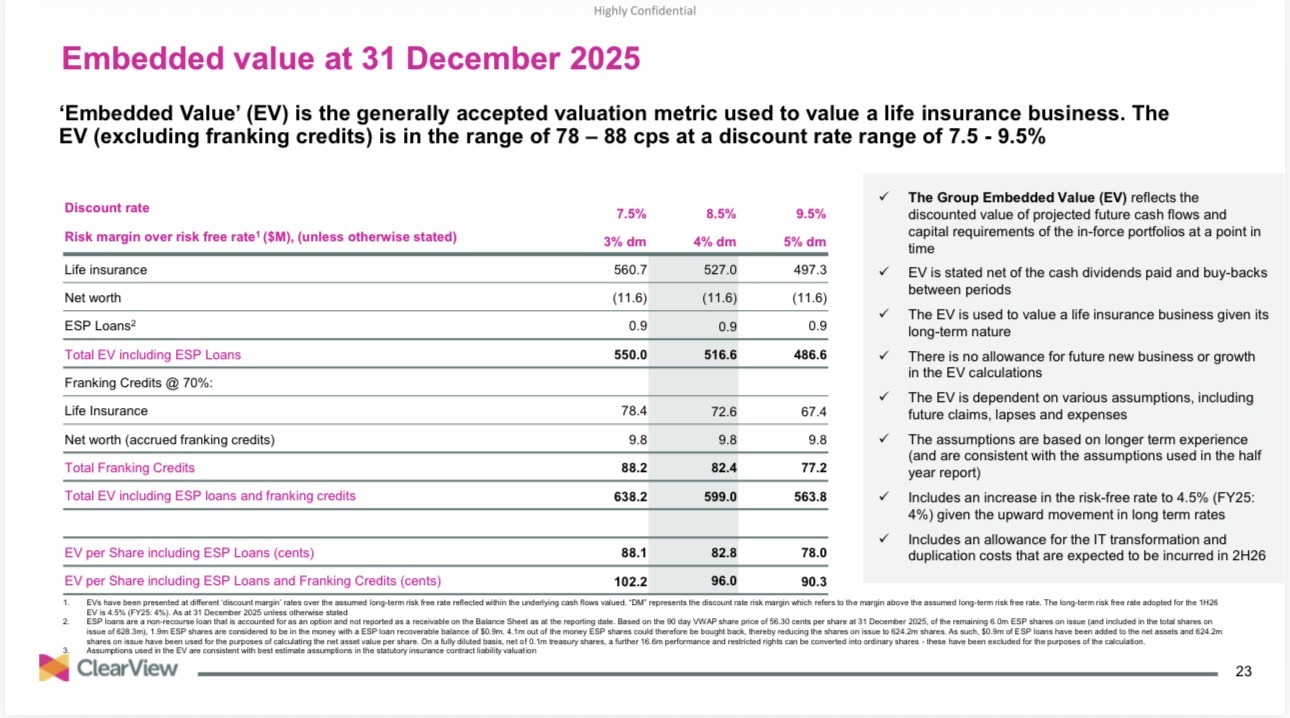

However, the more relevant metric for many life insurance businesses is embedded value. Embedded value attempts to estimate the present value of future profits expected from the existing policy book.

For ClearView, embedded value excluding franking credits was estimated at between 78 and 88 cents per share. This figure is particularly notable when compared with the current takeover proposal of 65 cents per share. Even before considering the value of franking credits attached to potential dividends, the offer sits meaningfully below the company’s embedded value estimate.

From a purely financial perspective, this suggests that Zurich’s proposal captures ClearView at a relatively modest valuation relative to the future profits expected from its existing policies.

Technology Transformation Underway

Beyond the headline financial metrics, ClearView has also been undertaking a significant technology transformation designed to simplify and modernise its operating platform. Historically, many life insurers have operated with complex legacy systems built over decades. These systems can create operational inefficiencies and limit the speed at which companies can innovate or introduce new products.

ClearView is addressing this challenge through a migration to a single cloud based core insurance platform. This transition is intended to reduce system complexity, streamline operations, and lower long term costs.

A new digital front end platform is scheduled for release during the second half of FY26. This system is expected to enhance the experience for both advisers and policyholders by improving application processes and policy management.

At the same time, legacy systems are gradually being decommissioned. Removing these older platforms reduces duplication and allows the company to operate with a simpler and more scalable technology architecture. These initiatives may not capture daily market headlines, but they play a crucial role in shaping the long term competitiveness of the business.

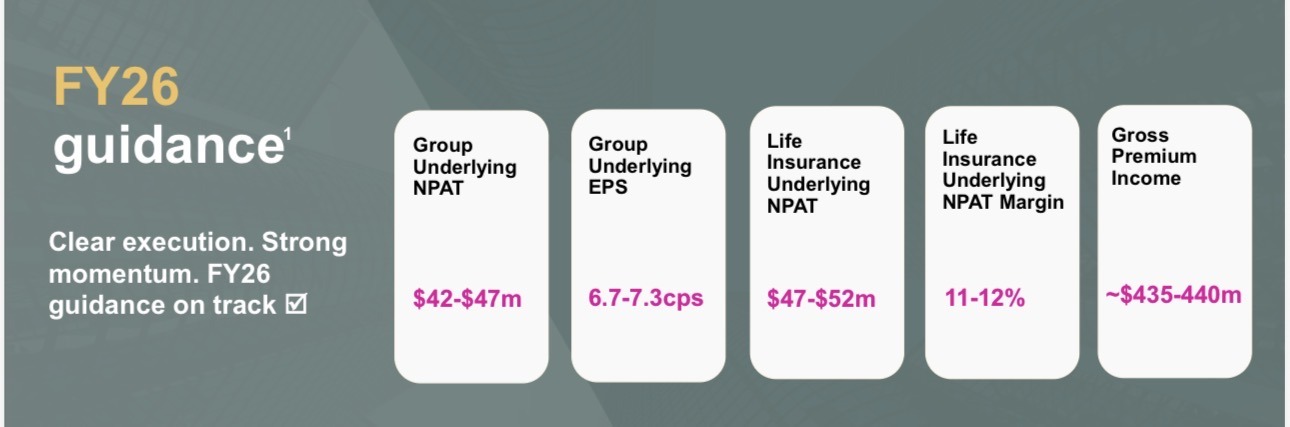

FY26 Outlook Remains Positive

Looking ahead, management has reaffirmed a constructive outlook for the remainder of FY26. The guidance incorporates the February 2026 industry repricing cycle and suggests continued premium growth. Gross premium revenue for the full year is expected to fall between $435 million and $445 million. Given that in force premiums have already reached $436 million, the second half of the year is expected to begin with a strong revenue run rate.

Group underlying net profit after tax is forecast to land between $42 million and $47 million for FY26, with earnings per share expected to reach between 6.7 cents and 7.3 cents.

At the proposed takeover price of 65 cents per share, this equates to a forward price earnings multiple of approximately 9.3 times at the midpoint of guidance. For a business delivering double digit revenue growth and significant earnings expansion, this valuation appears modest by most standards.

The Zurich Proposal

Against this backdrop, Zurich’s takeover proposal takes on greater significance. The scheme of arrangement offers shareholders 65 cents in cash per share, valuing the company’s equity at approximately $415 million. The proposal also allows for up to 5 cents per share in fully franked dividends, which would add approximately 2.14 cents of franking credits for investors.

ClearView’s board has unanimously recommended that shareholders vote in favour of the scheme. The company’s largest shareholder, Crescent Capital, which holds roughly 53 percent of the shares, has indicated its intention to support the transaction.

The proposal remains subject to regulatory approvals from both the Australian Competition and Consumer Commission and the Australian Prudential Regulation Authority. If these approvals are received, a scheme meeting is expected to take place around mid August 2026.

Is There Room for a Higher Bid?

While the Zurich proposal represents a clear pathway to liquidity for shareholders, it also raises an important question. Is this the best price ClearView could achieve?

Based on the company’s embedded value estimates of between 78 and 88 cents per share, the current offer sits at a meaningful discount to the estimated long term economic value of the business.

The offer also represents a relatively modest earnings multiple given the company’s growth trajectory. In our view, this leaves open the possibility of a competing proposal emerging in the coming months. A rival bidder offering between 70 and 75 cents per share would not be difficult to justify financially, particularly for a strategic buyer seeking to expand its presence in the Australian life insurance market.

Whether such a bid materialises remains uncertain. Corporate transactions are influenced by many factors beyond simple valuation metrics, including strategic fit, regulatory considerations, and shareholder dynamics.

The Crescent Factor

Another element that has historically influenced investor perception of ClearView is the presence of Crescent Capital as the majority shareholder. Large controlling shareholders can sometimes create an overhang for minority investors, particularly when the timing of potential exits is unclear.

By placing the company in play through the Zurich scheme proposal, Crescent has effectively removed that uncertainty. The market now has a clear timeline for a potential transaction and a defined valuation benchmark. For investors who have held the stock for several years, this represents an important development.

What Happens Next

Over the next few months, the market will watch closely to see whether any alternative proposals emerge. If a competing bidder appears, shareholders may ultimately receive a higher price for the business. If not, the Zurich scheme will likely proceed as planned. Either outcome provides clarity for investors.

If the scheme completes at the current price, it effectively sets the final valuation the market was willing to place on the business at this point in time. While that valuation may sit below embedded value estimates, it reflects the realities of market demand and corporate transaction dynamics.

If a higher offer does emerge, it will confirm that the underlying economics of the business are worth more than the current proposal suggests.

TAMIM Takeaway

ClearView’s first half FY26 results demonstrate a business that is performing strongly operationally. Sales momentum is accelerating, claims experience remains stable, and earnings are growing rapidly. The company’s embedded value also suggests that the long term economics of the business may be worth significantly more than the current takeover proposal.

Zurich’s offer at 65 cents per share provides a clear exit pathway for shareholders and establishes a baseline valuation for the company. However, the offer sits at a relatively modest earnings multiple and below the company’s embedded value range.

In our view, the coming months will determine whether another bidder emerges with a higher proposal. A competing offer in the range of 70 to 75 cents would not be difficult to justify based on the company’s financial performance and growth trajectory.

If no alternative proposal appears, the scheme will likely proceed and provide closure for investors who have followed the ClearView story for several years. Either way, this situation highlights an enduring truth in small cap investing. Value can remain hidden for long periods of time, but when it is finally recognised, it often happens quickly.

_______________________________________________________________________________________________

Disclaimer: ClearView Wealth (ASX: CVW) is held in TAMIM Portfolios as at date of article publication. Holdings can change substantially at any given time.