Top 3 International Shares for 2024

|

Global equity markets finished the year on a tear as investors gained confidence that inflation had abated and interest rate hikes were in the rear vision mirror. There was a clear bifurcation however, with the bounce led by a small number of suspects (we’re looking at you big tech) while 70% of companies in the S&P500 underperformed the index in 2023.

|

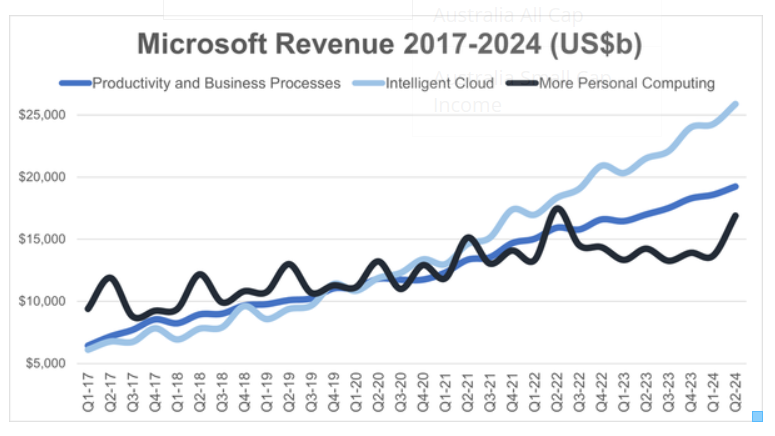

Microsoft’s results were also impressive, which they needed to be following the company’s addition to the $3 trillion market cap club. Revenue of $62.0 billion increased 18% YoY (16% excluding the impacts of currency changes), and net profit was $21.9 billion, 33% higher than the pcp (or 26% ex-currency). Intelligent Cloud was again a key driver of Microsoft’s performance, with revenue growing 20% YoY to $26 billion, including a strong 30% YoY performance from Azure and other cloud services. Unsurprisingly given its investment in ChatGPT developer OpenAI, AI dominated the conference call. Examples included approximately 53,000 clients using its cloud-based AI platform Azure AI (one-third of which were new to Azure this past year) and an AI-infused Office was released for business users. Microsoft also completed its highly publicised acquisition of Activision Blizzard on October 13, which juiced Microsoft’s More Personal Computing division, which saw 19% revenue growth including 61% growth at Xbox. Guidance for the upcoming quarter was strong, and shareholders were rewarded with $8.4 billion in dividends and buybacks. They should be very satisfied with the company’s performance.

Microsoft’s results were also impressive, which they needed to be following the company’s addition to the $3 trillion market cap club. Revenue of $62.0 billion increased 18% YoY (16% excluding the impacts of currency changes), and net profit was $21.9 billion, 33% higher than the pcp (or 26% ex-currency). Intelligent Cloud was again a key driver of Microsoft’s performance, with revenue growing 20% YoY to $26 billion, including a strong 30% YoY performance from Azure and other cloud services. Unsurprisingly given its investment in ChatGPT developer OpenAI, AI dominated the conference call. Examples included approximately 53,000 clients using its cloud-based AI platform Azure AI (one-third of which were new to Azure this past year) and an AI-infused Office was released for business users. Microsoft also completed its highly publicised acquisition of Activision Blizzard on October 13, which juiced Microsoft’s More Personal Computing division, which saw 19% revenue growth including 61% growth at Xbox. Guidance for the upcoming quarter was strong, and shareholders were rewarded with $8.4 billion in dividends and buybacks. They should be very satisfied with the company’s performance. The Alphabet share price took a hit the day of its earnings release, but there was actually much to like about the search giant’s results. Revenue rose 13% YoY, with a further improvement in Google advertising revenue, which revenue increased 11% YoY to $59.0 billion, from +9.5% YoY in the prior quarter and +3.3% YoY in 3Q 2023. Google Search revenue increased 13% YoY and YouTube ads increased 16% while Google Networks remained weak (fortunately this contributes less than 10% of the company total). Google Cloud revenue increased 26% YoY, and perhaps even more importantly, Cloud profitability has accelerated since breaking even early in 2023, reaching a 9.4% operating margin in 4Q 2023. Like Meta, Alphabet showed better cost control, with CFO Ruth Porat showing the benefits of the 2023 cost drive. The employee count was 4% lower at the end of the year and another round of layoffs have begun already in 2024. CEO Sundar Pichai was very optimistic about the company’s ability to implement AI initiatives, and combining this with better efficiency could lead to some healthy profit growth in years to come. The share count also continues to decline, with a further $16 billion of share repurchases in 4Q bringing the 2023 total to $72 billion. Overall, a solid performance from Alphabet.

The Alphabet share price took a hit the day of its earnings release, but there was actually much to like about the search giant’s results. Revenue rose 13% YoY, with a further improvement in Google advertising revenue, which revenue increased 11% YoY to $59.0 billion, from +9.5% YoY in the prior quarter and +3.3% YoY in 3Q 2023. Google Search revenue increased 13% YoY and YouTube ads increased 16% while Google Networks remained weak (fortunately this contributes less than 10% of the company total). Google Cloud revenue increased 26% YoY, and perhaps even more importantly, Cloud profitability has accelerated since breaking even early in 2023, reaching a 9.4% operating margin in 4Q 2023. Like Meta, Alphabet showed better cost control, with CFO Ruth Porat showing the benefits of the 2023 cost drive. The employee count was 4% lower at the end of the year and another round of layoffs have begun already in 2024. CEO Sundar Pichai was very optimistic about the company’s ability to implement AI initiatives, and combining this with better efficiency could lead to some healthy profit growth in years to come. The share count also continues to decline, with a further $16 billion of share repurchases in 4Q bringing the 2023 total to $72 billion. Overall, a solid performance from Alphabet. The most lacklustre of the Magnificent Seven to report was undoubtedly Tesla. Revenue grew a very modest 3% YoY to $25.2 billion and shares have fallen nearly 10% since a less-than-impressive earnings call. In particular, investors likely focused on comments by CFO Vaibhav Taneja that volume growth in 2024 will likely be lower than in prior periods as the company focuses on the launch of the next-generation vehicle. This comes amidst a challenging time for Tesla given a general slowdown in the EV market and significantly greater EV competition (particularly in China and by Chinese exporter BYD). As has been frequent throughout Elon Musk’s career, there have also been a number of other recent distractions, including the overturning of his extraordinary $55 billion compensation package, the possible relocation of the company’s incorporation from Delaware to Texas, media reports about drug use, comments about launching an unaffiliated AI/robotics entity, and of course, the severe decline in profitability at X (formerly known as Twitter) following his take-private transaction in 2022. Musk undoubtedly has a loyal base of supporters and has proven his ability to navigate challenging environments before, and it appears that 2024 will be another busy year.

The most lacklustre of the Magnificent Seven to report was undoubtedly Tesla. Revenue grew a very modest 3% YoY to $25.2 billion and shares have fallen nearly 10% since a less-than-impressive earnings call. In particular, investors likely focused on comments by CFO Vaibhav Taneja that volume growth in 2024 will likely be lower than in prior periods as the company focuses on the launch of the next-generation vehicle. This comes amidst a challenging time for Tesla given a general slowdown in the EV market and significantly greater EV competition (particularly in China and by Chinese exporter BYD). As has been frequent throughout Elon Musk’s career, there have also been a number of other recent distractions, including the overturning of his extraordinary $55 billion compensation package, the possible relocation of the company’s incorporation from Delaware to Texas, media reports about drug use, comments about launching an unaffiliated AI/robotics entity, and of course, the severe decline in profitability at X (formerly known as Twitter) following his take-private transaction in 2022. Musk undoubtedly has a loyal base of supporters and has proven his ability to navigate challenging environments before, and it appears that 2024 will be another busy year.