By Ron Shamgar

Markets have a curious habit of extrapolating the recent past far into the future. When a company experiences a difficult period, investors tend to assume that weakness will persist indefinitely. Yet history shows that some of the most compelling opportunities arise precisely when sentiment is weakest but the underlying business is quietly being rebuilt.

In our view, EML Payments may be approaching that moment.

Over the past two years the company has gone through a significant transition. Operational changes, regulatory remediation, portfolio simplification, and technology upgrades have dominated management’s agenda. These initiatives have inevitably weighed on near-term growth and investor confidence.

But transitions eventually end. And when they do, the market often rediscovers businesses that look very different from the ones it had previously written off.

Today, EML appears to be entering the final phase of its reset.

A Transitional Year Approaching Completion

Management has been clear that FY26 represents a rebuilding year. The objective has not been to maximise short-term growth but to stabilise the platform, modernise technology infrastructure, and rebuild the commercial pipeline. From that perspective, the first half of FY26 looked exactly like a company in transition.

Revenue for the half came in at $108 million, representing a 6 percent decline year on year and slightly below market expectations. The weakness was primarily driven by two factors.

First, interest income declined by 12 percent, reflecting changes in interest rate dynamics and balance structures across several programs. Second, customer revenue declined 4 percent, largely reflecting the lingering effects of program attrition that had already been flagged in earlier updates. At the surface level, those numbers understandably disappointed investors. However, focusing only on the revenue line risks missing the broader picture.

EML has spent the past year aggressively reshaping its cost base and operating model. As a result, overhead expenses remained flat at $53 million, demonstrating the company’s ability to maintain discipline despite continued investment in technology and product development.

This cost control helped preserve profitability, with underlying EBITDA of $28 million for the half, broadly in line with market expectations. In other words, while revenue softened, the business remained resilient. More importantly, the groundwork for the next growth phase continued to take shape behind the scenes.

Sentiment Weakness Created the Opportunity

Investor sentiment towards EML weakened significantly following the company’s first quarter update in November 2025. At the time, management warned that the early part of the year would be soft as customer transitions and legacy program impacts continued to flow through the system. The market reacted quickly, raising concerns that the company might struggle to meet its full-year guidance.

Yet the subsequent quarter told a more balanced story. The second quarter delivered EBITDA of $22 million, driven largely by seasonal strength in the Gifting and Incentives segment, which traditionally performs well during the holiday period. More importantly, the improved quarter provided management with sufficient confidence to reaffirm full-year guidance, tightening the expected EBITDA range to $58 million to $60 million.

This confirmation was important. It signalled that the transitional weakness was both anticipated and manageable. For long-term investors, the key takeaway was not the softness in the first half. It was the fact that management continued to demonstrate confidence in the trajectory of the business.

The Strategic Reset Is Beginning to Show Results

Behind the headline numbers sits a far more important story. Over the past year EML has been quietly executing a strategic reset that aims to reposition the company for the next phase of growth.

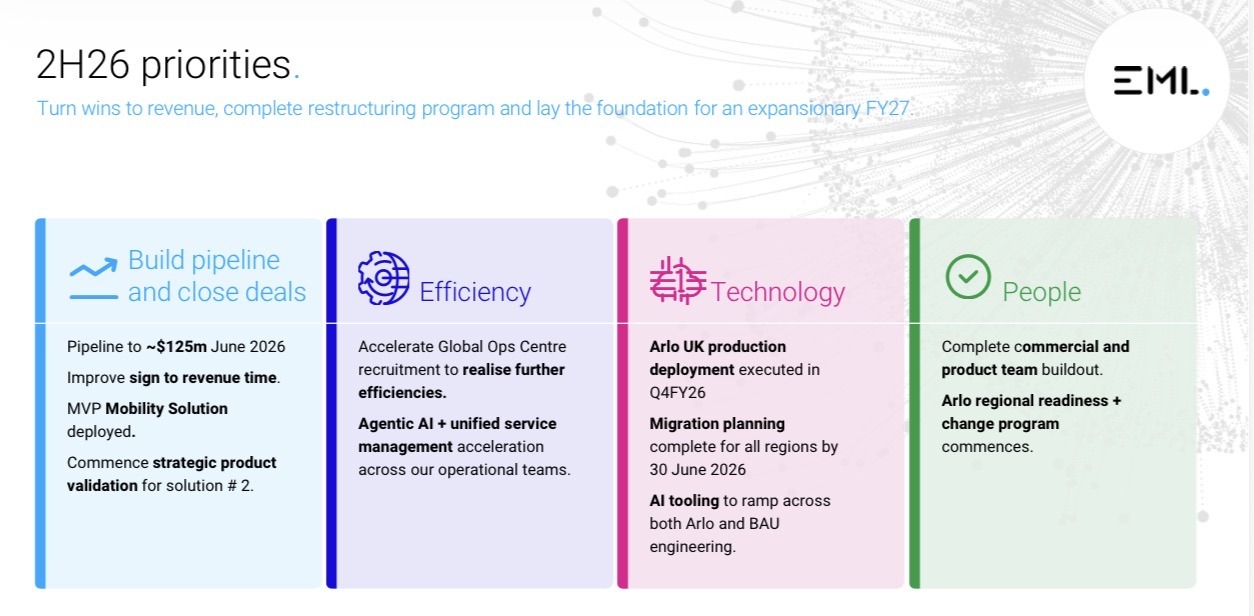

Four key pillars define that strategy. First, the company has been rebuilding its commercial pipeline, re-engaging with customers and partners following the regulatory disruptions of prior years. Second, EML has invested heavily in modernising its technology infrastructure, including migrating programs onto a more scalable and flexible processing environment. Third, management has expanded the company’s product capabilities, enabling new revenue streams that were not previously available within the platform. Finally, the business has pursued targeted cost efficiencies, improving operating leverage and lowering the cost to serve customers.

Importantly, these initiatives are not theoretical. They are already beginning to show up in operational metrics. And investors may begin to see the full impact as early as the upcoming August result, when the benefits of the reset become more visible in forward guidance.

Enter the Mobility Payments Opportunity

Perhaps the most interesting development emerging from the reset is EML’s entry into the mobility payments sector. This vertical, which includes fuel card and mobility expense solutions, represents a trillion dollar global payments market. It is also a space where EML’s capabilities in program management, transaction processing, and corporate expense solutions translate naturally.

The company plans to launch its Mobility Minimum Viable Product (MVP) later this year. At the same time, customers will begin migrating onto Pismo, EML’s modern processing platform. The strategic importance of this transition should not be underestimated. Pismo provides a highly scalable, cloud-native payments infrastructure that allows EML to deliver new products faster and at lower operating cost. It also enables higher-margin revenue streams driven by product functionality rather than simply transaction volume.

In practical terms, the platform should reduce the company’s cost-to-serve while simultaneously expanding its ability to monetise payment programs. That combination is powerful. Lower costs and higher margins create operating leverage that can significantly enhance profitability once revenue growth returns.

Existing Customers Provide a Natural Adoption Base

One of the advantages EML enjoys in launching the mobility vertical is its existing customer relationships. In particular, the company already services a number of salary packaging providers, many of whom operate programs that involve transportation or fuel-related expenses. Management believes these existing customers represent a natural adoption opportunity for mobility solutions.

Instead of starting from zero, EML can leverage established partnerships to introduce the new product suite. If adoption occurs as expected, the mobility offering could accelerate revenue growth over time while strengthening customer relationships. Importantly, management has emphasised that investment into the vertical will remain disciplined.

Capital will only be allocated to initiatives where there is clear commercial demand and identifiable revenue pathways. In other words, the mobility strategy is not an open-ended experiment. It is a targeted expansion built on existing capabilities and customer relationships.

A Pipeline That Has Quietly Reappeared

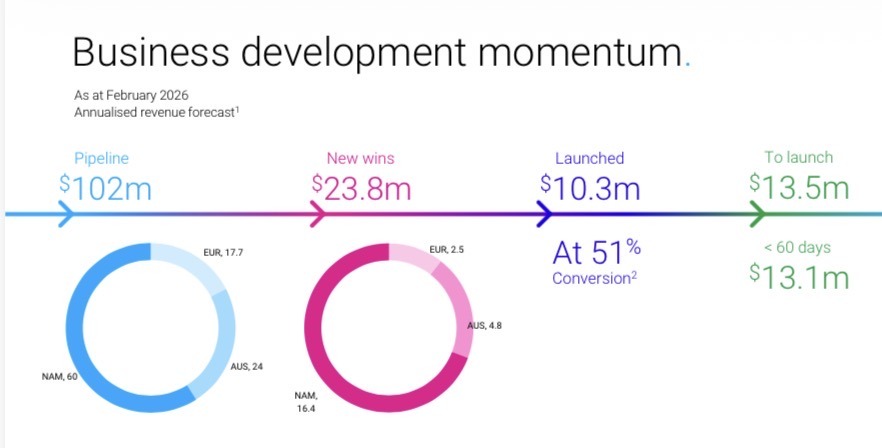

Perhaps the most telling indicator of the reset’s success is the re-emergence of EML’s commercial pipeline. Twelve months ago the company’s pipeline had effectively disappeared following the disruptions of prior years. Today it has rebuilt to $102 million, exceeding internal targets.

Even more encouraging is the revenue visibility attached to that pipeline. New customer wins are expected to generate approximately $24 million in annualised revenue once fully launched during the second half of FY26. At the same time, the attrition impacts that weighed on the business over the past two years are expected to ease significantly through the remainder of FY26.

Taken together, these two factors create a more constructive growth profile heading into FY27. Management believes that roughly half of all new revenue will ultimately drop through to EBITDA. That level of incremental margin suggests meaningful operating leverage once growth resumes.

Incentives Matter

One of the most interesting aspects of EML’s story today lies not in the business itself but in the incentives driving management. There are currently 63 million performance shares allocated to the leadership team. These shares only vest if the company’s share price reaches $1.50 by August 2027. If that target is achieved, management stands to receive approximately $95 million of value.

If it is not achieved, the performance shares are worthless. Few structures align management and shareholders more clearly than that.

The late Charlie Munger once famously said:

“Show me the incentive and I’ll tell you the outcome.”

While outcomes are never guaranteed, incentive structures like this create a powerful motivation for management to deliver. With roughly sixteen months remaining before the vesting window closes, the leadership team has a clear reason to ensure that the next phase of EML’s growth story becomes visible to the market. That visibility will likely begin with the upcoming August result, where forward guidance may play a crucial role in shaping investor sentiment.

A Valuation Disconnect

Despite the progress taking place within the business, EML continues to trade at a valuation significantly below global peers. Payments companies with similar growth potential typically trade between eight and twelve times EBITDA.

EML currently trades at approximately 4.5 times EV to EBITDA, falling below four times on FY27 estimates. On management’s FY28 target of $95 million in EBITDA, the multiple falls below three times. Such valuations are typically associated with businesses facing structural decline or significant operational risk.

Yet EML’s situation appears increasingly different. Regulatory remediation has been completed. The balance sheet has improved. Technology infrastructure is being modernised. And the commercial pipeline is rebuilding. If the company successfully executes the next phase of its strategy, the valuation gap may prove difficult to justify.

Three Potential Catalysts Ahead

For investors considering the opportunity today, the next twelve months could prove pivotal. Three potential catalysts may drive a shift in sentiment. The first relates to mobility payments. News flow surrounding the launch of the mobility vertical and the onboarding of foundational clients could demonstrate the commercial potential of the new platform. The second catalyst is strategic interest. Given the company’s low valuation and improving operational profile, the possibility of a takeover cannot be ignored. Payments infrastructure businesses with strong platforms often attract interest once legacy issues have been resolved. The third and perhaps most immediate catalyst will be the August result and FY27 guidance. If management demonstrates clear revenue momentum and reiterates confidence in its medium-term targets, investors may begin to reassess the company’s growth prospects.

Looking Toward FY27

Current market consensus expects FY27 EBITDA of approximately $66 million. Based on the operational improvements already underway, we believe management may be capable of delivering closer to $70 million. If that level of performance is achieved, and the company simultaneously reaffirms its FY28 target of $95 million, the market’s perception of EML could change rapidly.

In that scenario, the valuation multiple may begin to expand toward industry norms. Even a move from the current four times multiple toward eight times EBITDA, still below global peer averages, would imply a substantial re-rating in the share price.

The Tamim Takeaway

Investment opportunities often emerge when companies are transitioning from a period of difficulty toward a new phase of growth. EML appears to be approaching exactly that point.

The business has spent the past two years addressing legacy issues, rebuilding its commercial pipeline, modernising its technology platform, and strengthening operational efficiency. Those efforts are now beginning to bear fruit.

At the same time, the launch of the mobility payments vertical and the migration onto the Pismo platform provide the foundation for future product-led growth. With management strongly incentivised to deliver results and the company trading at a valuation well below global peers, the coming months may prove decisive.

If execution continues and guidance begins to reflect the underlying improvements in the business, EML’s current valuation may look increasingly difficult to justify. Transitions eventually end. When they do, markets often rediscover companies that have quietly rebuilt themselves. EML may be approaching that moment.

_______________________________________________________________________________________________

Disclaimer: EML Payments (ASX: EML) is held in TAMIM Portfolios as at date of article publication. Holdings can change substantially at any given time.