Reporting Season is drawing to a close with just one week remaining. With this in mind, we thought it would be appropriate to provide an analysis of two of the bigger names to report so far. Guy Carson, manager of the TAMIM Australian Equity All Cap Value IMA, provides his thoughts on Telstra (TLS.ASX) and Brambles (BXB.ASX).

Reporting Season Analysis: Telstra & Brambles Guy Carson

With a week of reporting season left to go, it is fair to say that the divergence amongst results has been high. As expected, the mining companies have led profit growth with Rio Tinto reporting 12% growth in underlying earnings for the full year and BHP reporting a 157% increase in their half year earnings. This has translated into increased payouts for shareholders. Of course, given the sharp rally in commodity prices the results were largely in line with analysts’ expectations. It’s at the other end of the spectrum, the disappointments, where we find lessons on what signs we can use to avoid companies. Two of the top twenty companies have issued profits that missed expectations, these were Telstra and Brambles.

Telstra (TLS.ASX)

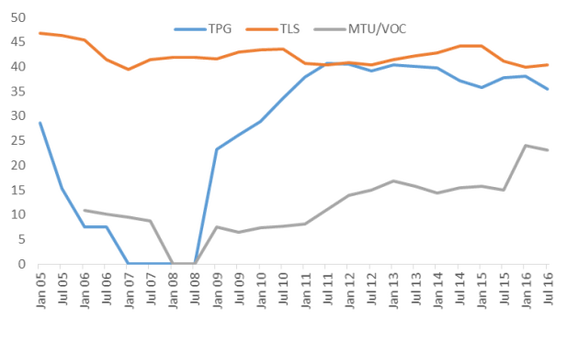

Telstra’s problems are largely not of their own doing. The industry is coming through significant change with the rollout of the National Broadband Network (NBN) and the end of Telstra’s natural monopoly. The NBN is publicly owned and levels the playing field in terms of competition. Hence, Telstra will potentially suffer the most from its introduction. Despite this assessment, last year we saw a significant selloff in the price of their competitors TPG Telecom and Vocus. Of course those companies were trading on significantly higher valuations, but nevertheless Telstra seemed to get off lightly.

The major reason Telstra is set to be the big loser from the NBN is that it effectively loses its place as the lowest cost participant in the market. This will have the impact of reducing margin both through having to pay connectivity fees to the NBN and increased competition. Telstra has historically enjoyed significantly higher margins than the industry and they are clearly set to fall.

Source: Telstra company filings

In fact, the company has been kind enough to quantify the impact of the NBN for shareholders. Between now and 2022, the company will lose $2-3bn of recurring EBITDA. Total EBITDA in the last financial year was $10.5bn.

Source: Telstra company filings

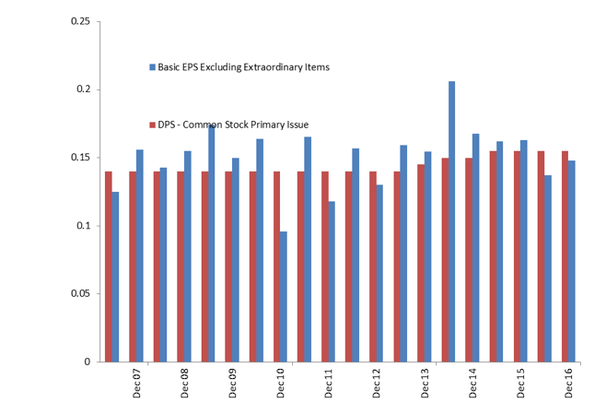

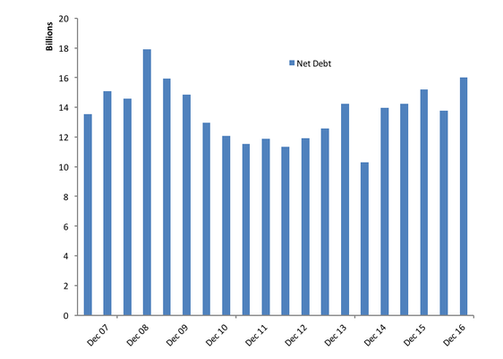

So in all likelihood earnings are going to fall over coming years. In addition to the impact quantified above there is the unknown aspect of competition. The signs in the most recent report are that the company is losing market share ever so slightly. Yet despite all this the company has maintained its dividend in recent periods despite paying out over 100% of earnings.

Source: Telstra company filings

This situation is unsustainable particularly when one factors in the $2-3bn impact of the NBN into the company’s earnings. In the meantime, the company is borrowing to pay shareholders.

Source: Telstra company filings

As a result we expect that Telstra will be forced to cut their dividend sooner rather than later.

Brambles (BXB.ASX)

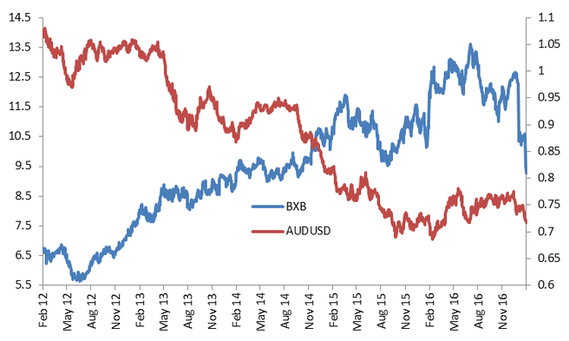

Brambles had been somewhat of a market darling over the last four years with the share price having gone from a low of around $6 in 2013 to a high of over $13.50 last year. One of the big drivers in the share price rise was the fall in Australian dollar from levels of over $1.05 to lows around the $0.70 mark. A popular trade in recent amongst “active” Australian Equities managers was to overweight International earners in order to take advantage of an elevated currency. Stocks such as Amcor and Brambles were noticeable beneficiaries of this trade.

Source: Brambles company filings

Now in the case of Amcor, the rerating was justified as the operation performance of the company improved significantly but in the case of Brambles we don’t think this is the case.

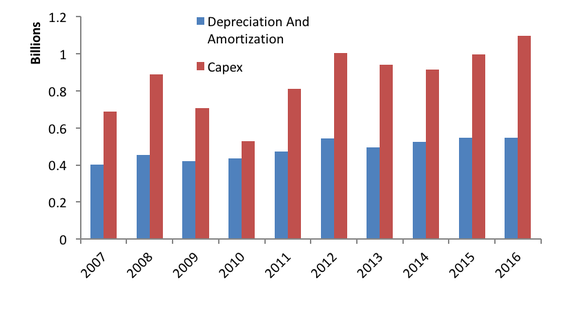

The first warning sign with regards to Brambles was the Free Cash Flow (FCF). Whilst the company has reported reasonable profit outcomes since 2013, the FCF has lagged significantly. This is particularly the case in the last 18 months.

Source: Brambles company filings

The reason for the FCF lagging is quite simple. The company has spent significantly more on Capital Expenditure (Capex) than has gone through the Profit and Loss statement as Depreciation and Amortisation.

Source: Brambles company filings

Now this isn’t necessarily a bad thing. Increased Capex, if used to invest in growth with a positive net present value, can be positive and increased the value of a company. The problem for Brambles is that despite this elevated level of Capex, revenues have barely moved. In fact since the end of the 2012 financial year, Brambles have spent over $2bn of additional Capex and yet revenues been broadly flat. With that in mind, It’s not surprising the company has withdrawn its previous 2019 target for Return on Capital Invested.

Source: Brambles company filings

This brings is to one of two conclusions. The first possibility is that Brambles is underestimating their depreciation charge and as a result is overstating profit. The second possibility is that issues in the business have been papered over by aggressive growth in other areas. Either way the rally in the share price over recent years looks unjustified.