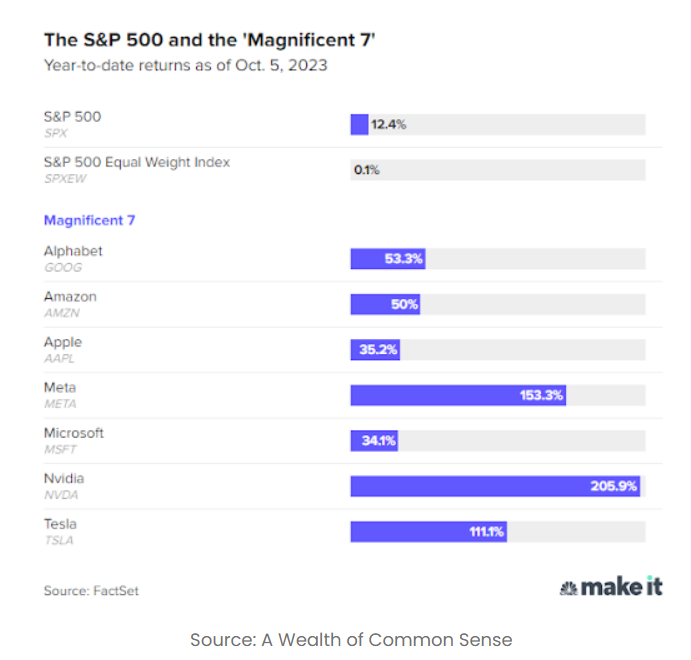

Why It Pays to be a Long Term Investor27/4/2023 Every year, index fund provider Vanguard makes a chart available that shows the returns of various asset classes over the past 30 years: shares (Australian, international and U.S.), bonds, Australian-listed property, and cash–-all ranked against the rate of inflation.

What’s important about this chart is the emphasis it places on a long-term investing horizon. The chart shows the total return an investor would receive over 30 years if they invested $10,000 in the various asset classes. Incredibly, between 1992 and 2022, $10,000 would have returned the following:

These returns compare to inflation as measured by the Consumer Price Index (CPI) of 2.9% p.a., which would have turned $10,000 in 1992 into $21,116 in 2022. The first thing that this chart tells us is that these long-term returns have occurred throughout (despite?) changes in governments overseas and in Australia (both political parties and all-too-often-of-late, Prime Ministers), acts of terrorism and war, natural disasters, and financial crises. Remember for example, how Donald Trump being elected was supposed to crash the market?

Never Interrupt It UnnecessarilyIt also shows the dramatic impact of compounding returns over time. What might look like small differences in those “p.a.” numbers above, turn out to be enormous amounts over time. For example, the 4.7% difference in the annual return between Australian Shares and Cash turns out to be a staggering 957% difference over 30 years. It’s often talked about but it bears repeating, the impact of compound interest is very difficult to conceptualise in your head–which is why Albert Einstein is often quoted (incorrectly) as saying: Compound interest is the eighth wonder of the world. He who understands it, earns it…he who doesn’t…pays it.” Or as Warren Buffett’s long-time companion and Vice-Chairman of Berkshire Hathaway Charlie Munger has said: “The first rule of compounding: Never interrupt it unnecessarily.”

This is particularly important to keep in mind as the current level of interest in savings accounts and term deposits might seem tempting after more than a decade of rock bottom rates. However, the Commonwealth Bank’s current 12-month term deposit of 4.35% is basically the same as the 30-year average of 4.3% p.a. While this is certainly worthwhile for any spare funds you might have sitting in a bank account (or under the mattress), it doesn’t even closely compare to the returns of the share market over longer periods of time.

Higher Interest Rates = Lower Share Market? Not So Fast.There is a commonly repeated assumption that makes intuitive sense: when the RBA (and Federal Reserve) raise interest rates, investors can take advantage of the higher risk-free (or close to it) returns in the form of term deposits and government bonds. However, looking back through history there isn’t actually a strong (or any) correlation between the level of interest rates and share market returns. The highest government bond yields were in the 1980s, where it may surprise you to learn, was also one of the highest returns on the share market. Yields were low in the 2000s, as were stock market returns. This could be due to the higher rates of inflation that accompany higher interest rates (stocks typically are able to keep pace with inflation relatively well), or other factors, such as economic growth or the starting valuation of the share market (certainly a factor in the 2000s following the ‘dotcom bubble’).

Regardless, it’s far too simplistic (and inaccurate based on history) that higher interest rates equate to lower share market returns. In fact, in the U.S., when the 3-month Treasury Bill (T-Bill) averaged 5% for the entire year (around the current level, 25 out of the past 89 years), the annual return for the S&P 500 in those 25 years was 11%. This might be counter-intuitive, but historically higher interest rates have in fact meant higher returns for the share market.

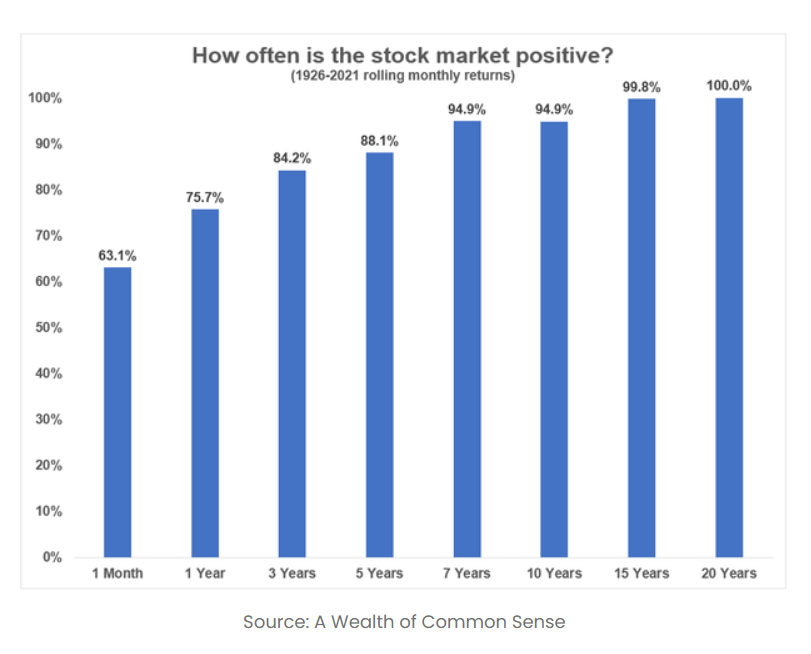

What the Averages Do (and Don’t) Tell UsWhile the Vanguard chart tells us that the “average” long-term return on the share market is typically between 9% and 10% (depending on factors such as which year the statistics start and end, and whether it’s Australian or U.S. shares), the actual return in any given year can be dramatically different. For example, the S&P 500 Index only had an annual return within 2% of the average six times between 1926 to 2018–a staggering 93 years.

There is in fact an enormous range in the share market returns in specific time periods, such as individual calendar years. However, if we extend our time horizon, the odds are stacked firmly in the investor’s favour: in each 20 year period of recorded stock market history, investor returns have been positive 100% of the time.

Small is BeautifulThe odds could prove even more favourable for investors willing to delve deep into the world of small cap companies. While the definition often varies, small cap(italisation) companies are typically those with less than a $500 million market capitalisation (perhaps extended up to $1 billion depending on factors such as the liquidity of the shares and the size of the company’s revenue and market cap). Since the GFC, small cap stocks had previously traded at a premium to both their own history and larger cap peers, but their valuations have since declined quite considerably as the risk of an economic slowdown has increased. In fact, in a recently published white paper from Jeremy Grantham’s GMO, the opportunity in “small cap quality” was highlighted, while Bank of America said that small caps are now at their cheapest level in 2 decades. While investors need to tread with caution (small caps’ operating performance can be more volatile in recessionary periods as they typically have less diversified business models and more customer and supplier concentration), there are undoubtedly some high quality small cap names currently trading at attractive valuations.

Is (Now + Small) the Recipe for Success?Annual share market returns can be highly volatile, but investing over the long term has historically delivered outstanding returns that far exceed both cash and inflation. With the overall stock market indices down in 2022, the probability of positive returns over the coming two decades looks even more promising. In fact, if history is any guide, returns over the coming 5 years could prove lucrative. Following previous crises dating back to the 1950s (including the likes of the 2008 Global Financial Crisis, 1987 “Black Monday” and the 1956 Suez Canal Crisis), only twice has the S&P 500 returned less than 85% over the subsequent 5-year period (following the 1970 recession and 1997-98 Asian crisis). Moreover, for those investors willing to do a little extra due diligence, small caps could prove especially fruitful.

|

Why It Pays to be a Long Term Investor

Why It Pays to be a Long Term Investor

Written by