Guy Carson, manager of the TAMIM Australian All Cap Value portfolio, has had an excellent year to date. This success has come from not only picking good stocks but also from managing the portfolio risk when he occasionally picks the wrong stock. This week, to illustrate how to minimise losses and maximise gains, Guy takes a look at one of his recent mistakes alongside some of his better picks.

One of the most common questions we have received in recent months is why do we hold so much cash (currently c. 37%). The answer to this is that it is a result of our bottom up process and is a function of two things: Firstly the number of stock ideas that we have at any given time and secondly the amount of exposure we are willing to take in each position. At the moment we hold 20 companies; this is the highest number we have for some time but our cash level remains elevated as the average position size is smaller. This is a function of us having less overall conviction in the current ideas due to either high valuations or greater risk in the business models.

As stock pickers we are aware that we are not going to get 100% of our calls right and hence we need to manage the risk within the portfolio. The key for us here is trying to minimise the downside from those we get wrong and maximise the upside from those that we get right. This is the key reason behind why we vary the weights of the stocks in the portfolio. In order to explore this concept further we wish to take a look at some of the calls we have either got wrong or right this year and how we have managed those positions over time.

One we got wrong: minimising losses

Recently we wrote about a company that we like called Inabox (IAB.ASX). For those who don’t follow the company, the company has since our write-up downgraded earnings on the back of a recent acquisition.

“It must be pointed out that this is a very small company with a little bit of debt so an investment is certainly not without risk. Whilst it may not be our largest position, we believe it is worthy investment for part of our capital.”

– Guy Carson, Telcos: Thinking outside of the box

Whilst we liked the story and believed the market was undervaluing the business, we were hesitant to place too much of our capital into the stock (taking a position of just 2%). When investing in small and micro-cap companies it is always important to remember that scale provides a form of protection. Things can go wrong very quickly and very easily for a small company and that was the case for Inabox through their acquisition of Hostworks.

Hostworks is a cloud services business that had achieved revenue of $22m and EBITDA of $0.6m in FY16. On acquisition, Inabox believed that they could achieve $2.9m of cost synergies primarily through reducing staff and rent costs. This meant the business would add meaningfully to EBITDA in FY18. The problem though comes when we look at the spread of its revenue across clients. The largest client represents over $3m of revenue (as you can see below); if this client was to leave then the profitability of the business is more or less wiped out.

Source: Company filings

This is the key risk with businesses of this size. One contract or client can make a big difference both on the downside and on the upside if gaining new clients. In the instance of Hostworks, revenue is now expected to be $15m in FY18 suggesting the loss of multiple clients.

As a result of this risk, these positions in our portfolio are always going to be small, they will grow if the story plays out and the company grows. In the case of Inabox, the story has not played out as we envisaged and our small weighting has limited our downside. Our initial weighting in the stock was 2%, the price had rallied since we bought it and the weighting stood at 2.2% at the time of the downgrade.

From our initial 2% position, Inabox has cost us approximately 0.8%. Despite this we still remain in positive territory for the month of November and up over 12% year to date. Thankfully we have got more right than we have got wrong.

Two we got right: maximising gains

The below table outlines our top five holdings at the start of the year (first published back in our 2017 Outlook).

When we look through the year to date returns, we have some significant success.

Gentrack has returned 57% including dividends;

IMF Bentham has returned 36% including dividends;

Altium has returned 58% including dividends;

Greys Ecommerce Group was taken over, we sold our position for a profit prior to the takeover;

Integrated Research has returned 44%.

Due to the nature of these, our current top five looks quite different as we have taken profits and locked in gains. In order to give you an understanding of how we have managed these positions we thought we would work through two quite different examples.

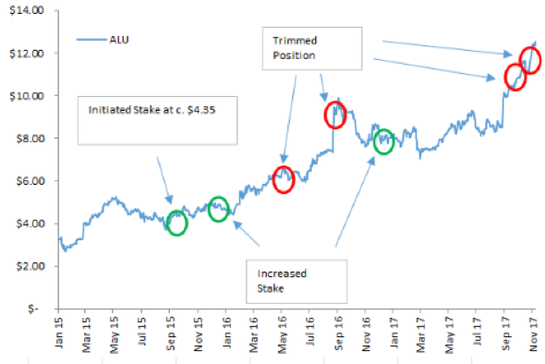

Altium (ALU.ASX)

Altium was our third largest position at the start of the year with a weight of 5.3%. We first acquired Altium back in 2015 at c. $4.35; we were attracted to the quality of the business and believed the market was under valuing the potential growth. As the stock rallied we took advantage and locked in some profits, most notably on its FY16 result when it almost hit $10. When the stock fell in the broader market selloff late last year we again took advantage and topped up our position to 5%. Altium is a very high quality company with global revenue and a sticky client base; as a result we are happy to take significantly more exposure to the company than the likes of Inabox.

The company recently reported a very strong set of FY17 numbers and the stock price has gone from $8.50 to above $12.50. Once again we have used this significant share price strength to rebalance our position, whilst we still hold Altium we do see increased valuation risk and as a result we have reduced our position to c. 2.5%. The company in our opinion remains the highest quality IT company listed in Australia. If the company does achieve its 2020 goals of becoming the market leader in PCB software and achieves its $200m target then over the medium term it will offer a good return, however short term risks have been amplified.

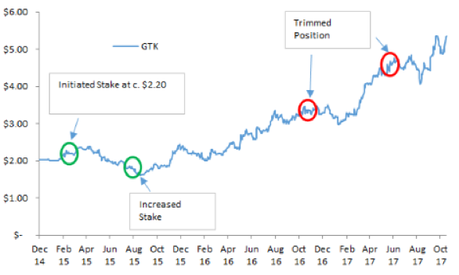

Gentrack (GTK.ASX)

Gentrack was our largest position at the start of the year (7.5%) and it remains that way now (7.5%). We have been shareholders since early 2015 shortly after the company’s IPO. The company made the cardinal sin of downgrading barely 6 weeks after listing. For a newly listed company this can severely impact credibility with the institutional market. As a result the share price fell and was trading on 16x earnings, significantly below peers trading in the mid-20s. When the share price fell further we bought more.

We have been less active with Gentrack than Altium. The company still trades at a discount to peers (with more conservative accounting) and as a result we have only traded to keep our weight below our 10% maximum. Whilst the share price has run significantly, this has been backed by earnings growth, most notably through the acquisition of Junifer Systems in the UK.

Whilst Gentrack is not the largest company on the ASX, we feel comfortable with a large position due to the nature of its industry. Gentrack is a software company servicing both the utility and airport sectors. Once their software is embedded in a company’s operations it becomes difficult to switch and hence you get a business model that sees:

A high degree of recurring revenue (Gentrack estimate that 50-60% of their revenue is “highly likely” to reoccur);

Low additional costs of bringing on customers, leading to high margins;

And very low capital costs leading to high returns on capital.

Due to these characteristics, we are happy to carry our current 7.5% weight.

Conclusions:

No stock picker in the world gets every call right and we have to acknowledge that when we construct a portfolio. There are two areas of risk we focus on, inherent weakness or lack of quality in the business model and valuation risk. Unfortunately finding positions where the risk is minimal on both counts is rare, when we do find them as was the case with Gentrack we take a high conviction position. When we find potential investments that we like but do have risks then we take a smaller position. If the story doesn’t play out as we expect it therefore doesn’t hurt us as much. On the other hand if the story does plays out and the risks dissipate, we can always increase our exposure if and when the story derisks