Listed Property

Investor Updates

December 2024 | Investor Update

Dear Investor,

The TAMIM Listed Property unit class delivered a -4.39% return for the month of December 2024. For comparison the A-REIT index was -6.93% while the G-REIT index was-2.63%.

Australian Listed REIT Portfolio (AUD)

For the last month of the year, the A-REIT market let slip and delivered a negative -6.93%. The portfolio beat the A-REIT market with a return of -5.88%. The ASX200 outpaced the A-REIT market in December, delivering -3.15%. For the full year however the A-REIT market (+18.50%) outperformed the ASX200 (+11.44%) by +7.06%. Global REITs were also in the red for December where the GPR 250 REIT World Index was down -7.46% (in USD) for the month. For the 2024-year A-REITs (+18.50%) also outperformed Global REITs (GPR 250 REIT World Index +12.72%) in AUD. Overall, we would say that it has been a good year for A-REITs compared to the global REIT market.

The best performing sector for the month was Retail (-5.1%), followed by Industrial (-5.5%) and then Office (-5.9%). There was however broad weakness in the market and no sector was spared. HMC dropped out of the ASX200 property index during December and was the worst performing holding for the month, delivering -20.03%. This was however not enough to dethrone it from the best performing REIT for the year of 2024, delivering 62.7%. The best performing REIT for the year in the ASX200 Property Index since HMC dropped out was Goodman Group (GMG), delivering 42.1%. GMG has had another stellar year and has increased its index weight from 36% at the end of 2023 to 43% at the end of 2024.

Last month’s top performing REITs (HMC +21.24%) and Lendlease (+5.60%) was this month’s two worst performing REITs, with HMC delivering -20.03% and LLC delivering -12.99%. HMC’s drop during December mainly stemmed from the exclusion from the Index (A-REIT 200), asset class rotation and probably some investors taking profit for the year. LLC has had a torrid year after its decision to exit global construction and development roughly halfway through the year. There was a lot of optimism from investors to have a focused Australian strategy, but it will seemingly take a lot of time to play out.

2024 was a turbulent year for the A-REIT market with the year starting off with investors expecting rate cuts which should have been a positive for the REIT market. This did not materialise as and when most expected and created substantial volatility in the market. 2025 is looking ever more set for rate cuts in Australia, although debate persists around the timing and magnitude of the cuts. The market is anticipating a cumulative 0.75% of cuts in 2025, with possibly another 0.50% of cuts in the first half of 2026. This should bring the terminal rate down to 3.10%. The RBA kept the cash rate constant at its meeting held on 10 December 2024, as expected. The Cash rate has now been 4.35% since November 2023, which was also the 9th straight meeting.

Headline inflation has eased substantially and is expected to remain lower for some time. There is still risk in the underlying inflation to rise again which could affect the goal of reaching the midpoint of 2-3% in 2026. It is expected that the new CPI reading should slightly increase to 2.2% for November. The RBA is in our opinion taking a fairly conservative approach, and decisions remain data dependent.

The ASX200 REIT Index was driven by Goodman Group’s standout performance (+42.1%) in 2024 and was all about its expansion into Data Centres. Globally we have seen similar trends with US REITs such as Digital Realty (DLR) and Equinix (EQIX) also delivering stellar performance with high demand for the next couple of years expected. If interest rate volatility starts subsiding in 2025, we would expect transaction volumes to pick up again and could aid sectors such as office, which has seen muted transaction volumes over recent years. The overall A-REIT market outlook is slightly positive, with some market participants and analysts expecting a 10-15% return in 2025. Australia’s strong economic institutions and policies provide a solid foundation for long-term stability and growth. However, the economy is likely to face short-term challenges, as tighter monetary policies are expected to remain in place for some time.

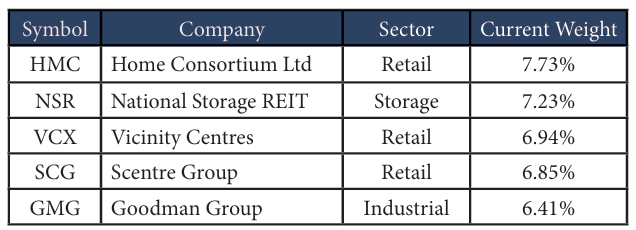

The current Australian portfolio component consists of 24 stocks. Below are the top 5 holdings:

Reitway Global Property Portfolio (USD)

The “Santa rally” for REITs was nowhere to be seen in December, more like the Grinch coming to steal it. December was a tough month for REITs with the Index (GPR 250 REIT World Index) retreating by 7.46%. This pushed the YTD return for 2024 down to only a slightly positive end to the year when compared to the start of the year, up 1.61% over 12 months. The fund was also down -8.27% for the month and this move pushed the total return for the year into the negative, -2.84%. December was the worst performing month for Global REITs for the whole year, indicating the current unclear path forward for the REIT market. To be fair, most global equities sold off in December on the back of the Federal Reserve’s hawkish-looking interest rate projections for 2025.

To put the month in perspective, we had no holding ending in the green for the month. The S&P 500 was down -2.50% for the month and the Dow Jones Industrial Average lost -5.27% in December. The best performing stock in the portfolio was Vornado Realty Trust (VNO -0.74%), an office REIT listed in the US. It was a standout performer in the sector for the month with many other office names down over 10%. VNO declared their dividend in December but had no specific news driving its resilience for the month. The second-best performer for the month was American Homes 4 Rent (AMH), down only -1.59%. The Apartment sector held up well during the month but slipped on the 17th of December in the lead up to the FOMC rate decision announcement.

The portfolio holdings that let us down the most during December was Iron Mountain (IRM -14.46%), SLG Green (SLG -12.81%) and Boardwalk REIT (BEI -12.23%). IRM is a record management services provider organised as a REIT and is expanding into the Data Centre realm. Their main revenue stream is from their storage business and has locations in 60 countries worldwide with a market cap of $32bn. One of the drivers for its inclusion in the portfolio is their Data Centre component of their business. There was no significant company news for IRM in December.

The storage sector (-12.66%) was the worst performing sector for December with most names in the sector significantly red. Over 1 year the sector was relatively flat, but IRM specifically has delivered a noteworthy 50% for 2024. Following that was Industrial (-8.25%), Health Care (-8.20%) and Speciality (-8.18%). The most resilient sectors for the month were Loding/Resorts (-0.48%), Manufactured Homes (-4.13%) and Regional Malls (-5.42%).

The global regions to the east delivered better returns for the month. The best region in the portfolio was Singapore (-3.60%) which was followed by Japan (-4.63%). Other regions in the benchmark to mention that was more resilient was Hong Kong (-2.78%) and India (-1.82%). Australia was the worst performing region (-10.79%) but that was on the back of a good year which still saw them end as one of the best regions for 2024. Canada was down -8.50% and the UK was also down -8.43% in December. In summary, there was just no place to hide for REIT investors in December.

On the 18th of December the US Federal Reserve cut interest rate by another 0.25%, as expected. This was the third consecutive rate cut this year, and it brought borrowing costs down to 4.50%. The so called dot plot indicates that policymakers are now anticipating only 2 rate cuts in 2025 by the Federal Reserve, totalling 0.50%. This has decreased from the 1.00% projected in the previous quarter. The Fed has revised its GDP growth forecasts upwards for 2024 and 2025 while remaining steady at 2% for 2026. Similarly, PCE inflation projections have been adjusted higher for 2024, 2025 and 2026. On the other hand, unemployment is seen lower this year and in 2025, while the forecast was kept at 4.3% for 2026. There is still a lot of upside risk to the inflation outlook due to recent stronger-than-expected readings on inflation and the potential changes in the trade and immigration policy.

The US Annual PCE inflation accelerated for the second month in a row to 2.4%. It was however below the expected increase of 2.5%. Interesting to note was the average PCE Price Index Annual Change in the United States was 3.29% from 1960 tot 2024, and it reached an all time high of 11.60% in March of 1980 and a record low of 1.47% in July of 2009. PCE Price Index provides a measure of the prices paid for domestic purchases of goods and services while the Consumer Price Index assumes a fixed basket of goods and uses expenditure weights that do not change over time for several years. The Federal Reserve currently uses the PCE data as its main gauge of inflationary data. The unemployment rate in the US for November which was released in December actually rose from 4.1% to 4.2%, in line with expectations.

Several sectors within the REIT (Real Estate Investment Trust) market have shown a modestly positive trend following what appears to have been the peak of the rate hiking cycle. Historically, REITs tend to outperform general equities in the aftermath of such cycles. However, there is an emerging consensus that interest rates may remain elevated for a longer period. Most central banks have initiated rate cuts and inflation readings generally fall within target ranges. Additionally, there exists considerable uncertainty due to various global factors, including a potential resurgence of inflation. Consequently, the precise impact on the global REIT market remains uncertain. Nevertheless, as global REIT market investors, we maintain a cautiously optimistic outlook for 2025.

Fund positioning remains roughly the same (quality, value, structural trend riders, and blend between offensive and defensive). The REIT market now has an increased appetite for risk in an easing cycle starting to unfold with global central banks starting their rate cutting cycles.

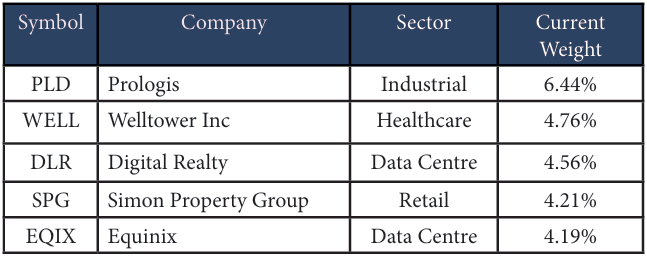

The Tamim global property portion invested in the Reitway Global Property Portfolio currently consists of 50 stocks. Below are the top 5 holdings:

We believe real estate fundamentals are still sound and remain steadfast in our belief that the asset class can post meaningful returns relative to stocks and bonds, even against a slower growth, higher inflation backdrop.

Fund Facts

Investment Parameters

| Management Style: | Active |

| Investments: | Listed property & property related securities |

| Number of securities: | 40-50 |

| Single security limit: | 10% |

| Region limit: | 70% |

| Sector limit: | 70% |

| Investable universe: | Listed property & property related securities |

| Market capitalisation: | N/A |

| Derivatives: | Yes – special instances & hedging |

| Leverage: | No |

| Portfolio turnover: | Typically < 25% p.a. |

| Cash level: | 0-100% (typically 0-20%) |

Fund Profile

| Investment Structure: | Unlisted Unit Trust (available to wholesale investors) |

| Minimum Investment: | $100,000 |

| Management Fee: | 0.98% p.a. |

| Admin & Expense Recovery: | Up to 0.25% |

| Performance Fee: | Nil |

| Hurdle: | N/A |

| Entry/Exit Fee: | Nil |

| Buy/Sell Spread: | +0.25% / -0.25% |

| Applications: | Monthly |

| Redemptions: | Monthly (with 30 day notice) |

| Distribution: | Quarterly |

| Investment Horizon: | 3-5+ years |