From Doom to Boom: The Story of 2023’s Economic Surprises23/11/2023 As we highlighted in last week’s article “The Power of Positive Thinking,” 2023 began with many dire predictions about the economy and asset prices. So far, these forecasts have not borne fruit, with the economy, real estate and equities all showing resilience in the face of rapid interest rate increases, inflationary pressures and an increasingly uncertain geopolitical environment.  Australian house prices have increased, the S&P 500 has rallied strongly on the back of developments in Artificial Intelligence (AI), and even the S&P/ASX 200 is modestly in the green (in addition to the healthy dividends investors receive). In fact, the surprising strength in the economy has led to a resumption in interest rate rises by the Reserve Bank of Australia (RBA) by new chair Michele Bullock, with early indications that there could be further increases to come. In the world’s largest economy, the United States, the majority of commentary from the 3Q 2023 financial reporting season highlighted an economy that continues to grow at a modest pace. Although it has slowed from earlier in the year, third quarter economic growth in the U.S. was a blockbuster 4.9% year-over-year (YoY)–above the consensus of 4.7% YoY and the fastest pace in nearly two years.

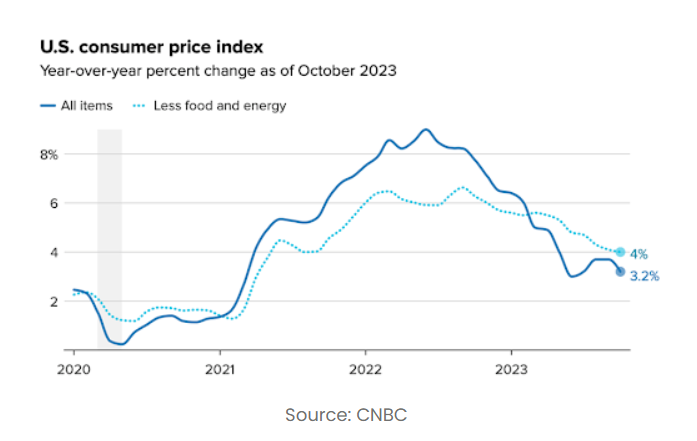

Inflation Numbers Spark Market RallyIn more positive news, the most recent U.S. inflation data came in better than expected. The October Consumer Price Index (CPI) was flat versus the prior month and increased just 3.2% YoY from a year ago. While this remains above the inflation rate of 2 percent over the long run targeted by the Federal Open Market Committee (FOMC), it was below the market’s expectations and a significant improvement from June 2022 when monthly inflation peaked at 9.1% YoY. (The FOMC is the branch of the Federal Reserve System (the U.S. version of the RBA) that determines the direction of monetary policy at eight regularly scheduled meetings each year).

From Transitory to Soft LandingThere has been heavy criticism throughout chair Jerome Powell’s tenure, particularly regarding the Federal Reserve’s hesitancy to commence raising interest rates and early descriptions of inflationary as “transitory.” Yet the Fed’s aggressive monetary policy actions over the past couple of years appear to be paying off, and there is increasing confidence that the economy can proceed with a so-called “soft landing” (meaning that economic growth will slow, unemployment will rise to a sustainable level and inflation will fall to the target level, all without causing a recession).

This is despite the more challenging mechanisms for the Federal Reserve to implement monetary policy in the U.S. In particular, mortgages are available on fixed rates for durations of 10-30 years, which limits the impact of regular interest rate increases in slowing down the economy. For example, when interest rates are increased in Australia, this effect is passed through very quickly to the incomes of most homeowners, most of whom have variable rate mortgages. In the U.S., interest rate increases will certainly affect corporations as well as new homeowners, but many existing homeowners will be much less directly affected.

Heavy Lifting Appears to be CompleteSince March 2022, the Federal Reserve has raised the benchmark Federal Funds Rate (the equivalent of the RBA’s “overnight cash rate”) 11 times. It now sits at 5.25%-5.50%, a 22-year high. Powell has recently said that the “resilience” of economic growth and the labour market “could warrant further tightening of monetary policy.” However, he appears in no hurry to raise the benchmark interest rate further, and the recent cooling of inflationary pressures provides strong support for rates to remain on hold.

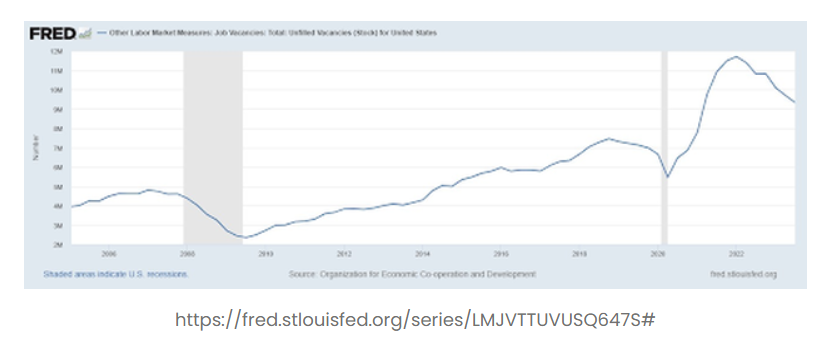

Employment data in the U.S. also supports a more sanguine period for interest rates. The most recent month showed that nonfarm payrolls had increased by just 150,000, a significant deceleration from prior months that may indicate an easing in the imbalance between the supply and demand for workers. While slower unemployment is usually seen as a negative, the staggering number of unfilled jobs in the U.S. had been a large contributor to the inflation over the last couple of years, with high wage increases and signing bonuses needed to entice people back into the workforce. Unemployment in the most recent month rose to 3.9%, the highest since January 2022 but still a strong level with approximately 9.5 million unfilled positions still available.

Outlook Remains FavourableWhile it is exceptionally challenging to predict the short-term direction of markets, the end of interest rate increases has been a positive signal for equity markets over the past 30 years. Over the past 5 cycles (ending 1989, 1995, 2000, 2006 and 2018), the S&P 500 has increased an average of 12.4% in the 6 months after the final rate hike, and 15.4% over the following year. (The only exception since the early 1980s was the dotcom bubble in 2000).

As previously mentioned, results and commentary from the majority of companies during the most recent (3Q 2023) financial reporting season support the view that the economy continues to progress. In further support, the outlook for the 2024 profits of the S&P 500 companies is for growth over 2023 levels. While not a direct one-for-one correlation, when earnings rise, stocks typically follow.

Markets Climb a Wall of WorryThe macroeconomic environment is notoriously unpredictable and constantly evolving, so it’s important not to place too much weight on each individual data point (especially when they can include large anomalies such as canal or port blockages, strikes, or geopolitical events). The outlook as ever looks challenging, with war in Ukraine and the Middle East, increasing political tensions as the U.S. approaches as Presidential year, and ongoing consumer challenges in the face of inflationary and housing stresses. Yet the economic picture as a whole appears to be more positive than the pundits would suggest.

Overall, in both the U.S. and Australia, employment remains healthy, economic growth is continuing and inflation has been slowing (even if not at the desired pace). The rapid increase in interest rates has not led to the predicted doom and gloom of bankruptcies, falling real estate prices (particularly offices) and mass unemployment that fear mongering had suggested, and most successful corporations have managed to deliver very healthy profits and dividends for shareholders.Finally, it’s important to keep in mind that the long-term trend for the market is up. In fact, since 1950 there have been a total of 21 years where stocks were in the red and 20 times they saw a 20% gain–the odds of a 20% gain being nearly the same as a down year might surprise a lot of investors. |

From Doom to Boom: The Story of 2023’s Economic Surprises

From Doom to Boom: The Story of 2023’s Economic Surprises

Written by