The green energy movement has emerged as a transformative force in the global economy.

Driven by the urgent need to mitigate climate change and reduce our dependence on finite fossil fuel resources, the concepts of recycling, regenerating, and reusing products have gained prominence. These practices are not only environmentally responsible but also present significant economic opportunities for companies operating within the green sector. In this article we’re taking a look at one of TAMIM’s holdings, Close the Loop (ASX: CLG), a small-cap ASX-listed business at the forefront of this movement.

The Business

Close the Loop is a global player in sustainable solutions, operating across Australia, Europe, South Africa, and the United States.

The innovative company specialises in creating eco-friendly products and packaging with a strong emphasis on recyclable and recycled materials. Furthermore, Close the Loop plays a pivotal role in resource management by collecting, sorting, reclaiming, and reusing materials that would otherwise end up in landfills. The company’s expertise spans a wide spectrum of sectors, including electronics, print consumables, eyewear, cosmetics, plastics, paper, and cartons.

Notably, Close the Loop excels in transforming post-consumer soft plastics and toner into valuable resources, highlighted by their groundbreaking asphalt additive, TonerPlas.

Close the Loop’s strategic positioning within the circular economy came about by the merger of the O F Pack Group with Close the Loop Limited in November 2021, coupled with its ASX listing. The successful $12 million IPO in December of 2021 has enabled the company to provide end-to-end solutions across packaging and consumables, serving diverse markets. With a keen focus on innovation, product development, and comprehensive end-of-life recovery systems, Close the Loop is steadfastly committed to reducing waste sent to landfills.

The Financial Position

Close the Loop reported its FY 2023 results at the end of August showcasing strong revenue growth of 52%.

The significant growth was driven by acquisitions which we’ll touch on later, the company detailed organic growth of 19%. The impressive revenue growth flowed through the profit and loss with Earnings Before Interest Tax Depreciation & Amortisation (EBITDA) up 70% to $24.3 million and Net Profit Before Tax (NPBT) up 113% to $14.9 million.

Chief Executive Officer Joe Foster commented:

“We are delighted to be reporting strong performance across the CTL group. In the financial year, our existing businesses have demonstrated substantial growth, showcasing a 19% increase in revenue. We have also continued to deliver on our inorganic global strategy and achieve the goals we set at the time of our IPO.”

The business produced strong improvement in its cash flows with operating cash flow for the year of $22 million up from an outflow of $3 million in the prior period. Following a number of acquisitions, a capital raise and debt funding, Close the Loop finished FY 2023 with a cash balance of $49 million.

Growth by Acquisition

Close the Loop has been incredibly busy acquiring businesses over the last financial year.

There were several minor acquisitions completed including Alliance Paper Pty Ltd, The Pouch Shop, Oceanic Agencies, In-Plas Recycling and Crasti & Company Pty Ltd assisting the business expand overseas and into new and existing areas.

Its largest investment was the successful acquisition of ISP Tek Services LLC and Captive Trade Corporation (ISP Tek), a US-based electronics refurbishing and trading platform, for up to US$66 million (A$99.7 million).

The strategic purchase, completed on April 28, 2023, significantly bolsters Close the Loop’s capabilities in consumer and commercial electronics remanufacturing, expands its presence in the US sales and trading market, and extends its distribution networks. It also enriches the company’s service portfolio by adding reuse capabilities, enhancing support for original equipment manufacturers (OEMs), and promoting sustainability and circular economy initiatives.

The acquisition was funded through a combination of debt and equity placement, aligning with the company’s capital management strategy. Close the Loop conducted a A$45 million placement of new fully paid ordinary shares to sophisticated and institutional investors. Additionally, Close the Loop partnered with Pricoa Private Capital to secure a US$40.0 million senior secured term loan, a US$7.5 million revolving credit facility, and a US$5.0 million delayed draw term loan facility to support the acquisition and future growth aspirations.

ISP Tek, in the brief two-month period under Close the Loop’s control, generated a substantial revenue of $16.362 million. This acquisition is poised to improve Close the Loop’s profitability by expanding its market reach, enhancing its technological capabilities, and solidifying its position as a leader in electronics remanufacturing and trading in the US.

Outlook

Close the Loop management is bullish on its FY 2024 outlook expecting revenue of $200 million and EBITDA of $43 million, growth of 47% and 77% respectively. With its dedication to sustainability and a circular economy, Close the Loop is well-positioned for a promising future, offering investors an optimistic outlook on their growth potential in the environmentally conscious market landscape.

Japan went through an historic boom that peaked in the late 1980s and early 1990s. Asset prices rose at an incredible pace, with the price of land absolutely rampant, increasing by as much as 5,000 per cent between 1956 and 1986. So distorted were land prices that land constituted a phenomenal 65% of Japan’s national wealth (compared to just 2.5% for the United Kingdom at the time), and Tokyo real estate sold for as much as US$139,000 per square foot–nearly 350 times the equivalent in Manhattan.

In hindsight the comparisons seem ludicrous (similar to other bubble periods), and eventually the market came to realise this as well. Property prices began to stagnate and then fall, and the Nikkei 225 (an index of Japan’s largest 225 stocks) fell by more than half its 1989 peak of 38,957 within just three years. Such was the incredible boom and bust of this period that the Japanese stock market continued to fall until the Global Financial Crisis, which kept the Nikkei 225 in the doldrums for several more years.

Since that time, however, contrarians who put aside the nearly two decades of declines have been richly rewarded. The Nikkei 225 has rallied nearly four-fold in the last decade, outpacing a number of the major global indices, including the ASX. The question now is, is there more to come?

Challenges of the Past

Historically, publicly-listed Japanese companies were notorious for poor corporate governance. It’s common for them to have numerous cross-holdings with other companies (making them more difficult to understand), and they are often accused of having inefficient operations–largely from having too many employees as a result of cultural norms to provide lifelong employment. (The story of former Renault/Nissan CEO Carlos Ghosn presents an interesting light on this, which Netflix recently made a documentary on).

Japanese companies also have a history of stockpiling cash on the balance sheet (rather than engaging in dividends or share buybacks), as a way of ensuring the longevity of the company. (Japan has some of the oldest continuously-operating companies in the world, and management are typically conservative by nature). These factors have meant generally low return on equity (ROE) for Japanese companies, which has often dissuaded overseas investors who are already deterred by the language and cultural barriers. But could this be changing?

Early Signs of Progress

The Japanese government has made a number of changes in an attempt to make publicly-traded companies less resistant to change. Since 2013, there have been various new regulatory directives, including requiring outside directors on corporate boards, tax law changes, and a change in market structure for the Japan Stock Exchange. These moves have placed both pressure and financial incentives on public companies to remove their publicly-traded subsidiaries by either an acquisition or a spin-off. This has led to a significant rise in corporate restructurings, parent companies acquiring subsidiaries, and interestingly, hostile takeovers (which were previously a rarer occurrence).

This has inspired an increasing interest from so-called “activist” investors, that were previously loath to breach the corporate, cultural and language challenges. (Activist investors buy a significant minority stake in a publicly-traded company and request changes to the operations or capital allocation. They are usually specialised hedge funds, such as Bill Ackman’s Pershing Square and Danile Loeb’s Third Point). The activists see significant opportunity to improve the operations of many Japanese corporations, driving down costs and raising returns on capital. They are also attracted to the under-utilised (so-called “lazy”) balance sheets, a favourite of activists, particularly the notorious corporate raider-types such as Carl Icahn.

Valuations Remain Attractive

Despite the strong performance of the Japanese share market since the GFC, it remains attractively valued. In fact, TAMIM’s global high conviction portfolio manager, Rob Swift recently stated that he believes the current price-to-earnings (P/E) ratio of the Japanese stock market (as measured by the Japan MSCI Index) is implying essentially no growth in earnings.

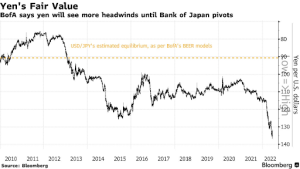

What’s more, the Japanese government is one of the few around the world that is actively encouraging a higher level of inflation. While this might seem strange to those of us struggling with high rates of inflation in Australia, Japan has struggled to generate much inflation for quite some time, which has concerned the country’s leaders due to the high level of government debt. As a result, the Bank of Japan is likely to tolerate much greater inflation before increasing interest rates–creating a more supportive environment for equity values. Even if interest rates do increase somewhat, it’s likely to have a much more muted impact compared to other developed nations given the public companies’ low valuations and cash-rich (largely debt-free) balance sheets.The nation’s currency, the Japanese yen, also looks attractively valued. It recently plumbed to a 24-year low against the U.S. Dollar, causing Bloomberg to call it “the most structurally undervalued” of the major world currencies. Bank of America also sees the Yen as undervalued, as you can see from the chart below. This significantly lowers the “currency risk” for Australian investors (the risk that an investor would lose money on the exchange rate, with the Japanese Yen declining against the Australian Dollar), and even increases the chances that the exchange rate may provide additional returns for investors (if the Japanese Yen were to appreciate).

Buffett Sees Value

If there were still any scepticism about the lingering value in Japan, the endorsement of investing great Warren Buffett should dispel any doubt. In 2020 (right around his 90th birthday), the chairman and CEO of Berkshire Hathaway (NYSE: BRK.B) ploughed slightly more than $6 billion into five of the major “sogo shosha” or general trading companies–Mitsubishi Corporation, Mitsui & Co., Itochu Corporation, Sumitomo Corporation and Marubeni Corporation. Buffett was sure to make clear that Berkshire would be a passive investor, and over time would be looking to increase the 5% stake in each of these businesses.”

In April of this year, Buffett met with the management of each of the five trading houses on a trip to Japan with Berkshire’s Chairman-Non Insurance Greg Abel, following which Buffett revealed that Berkshire had increased its ownership in each to 7.4%. This has since been raised to an average holding of 8.5%, with the market value of these 5 stakes considerably higher than Berkshire’s investments in any other country outside of the United States. Buffett and Abel also said that they “hope, eventually, to own 9.9% of each of the five companies.” High praise indeed from the Oracle of Omaha.

Diversification with a Difference

Australians seeking to diversify their portfolios internationally usually look to the United States because of the huge market opportunity, high-profile brand names and a history of wealth creation by well-incentivised management teams. Japan, on the other hand, has historically been left to the most motivated of value investors because of the language, cultural, and corporate governance challenges.

However, times are changing in Japan, and there are many high-quality businesses with cash-rich balance sheets ripe for corporate improvement. The country is a leader in many industries, including automotive production and semiconductors, and many stocks in these industries do not receive the same publicity (and therefore valuations) as their North American or other international peers. Advantest Corp (TYO: 6857), for example, is a leading manufacturer of semiconductor equipment that has performed well yet remains valued substantially below its international peers, while Tokyo Gas (TYO: 9531) trades at a meagre 4.5 times earnings and remains a key part of Japan’s energy future.With cheap valuations, a depressed currency, and corporate change all moving in the right direction, following Buffett into Japan might be a great opportunity to boost your portfolio’s returns.