Australian Equities

Australia All Cap

May 2025 | Investor Update

Dear Investor,

We provide this monthly report to you following conclusion of the month of May 2025.

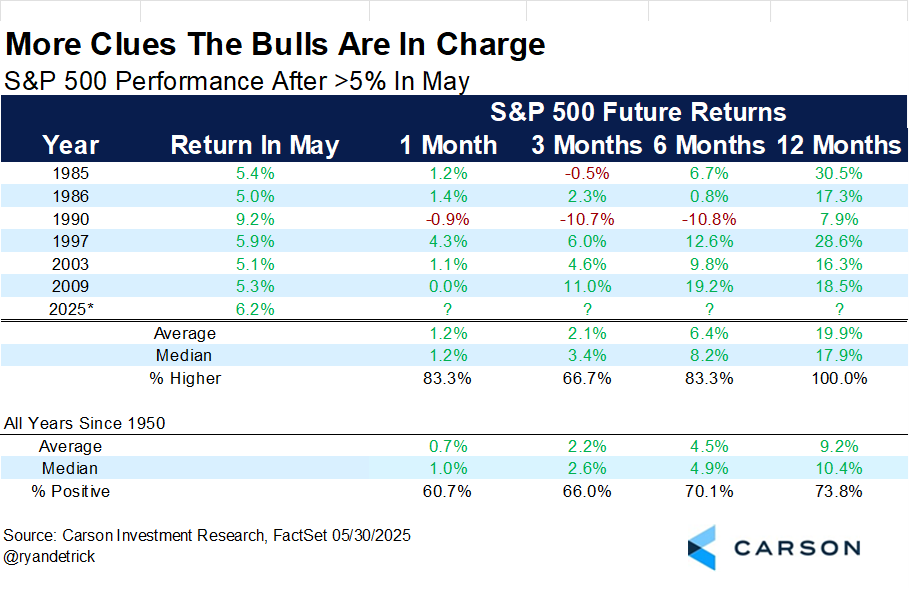

The TAMIM All Cap Fund was up +5.84% (net of fees) during the month, versus the Small Ords up +5.76% and the ASX300 up +4.20%.

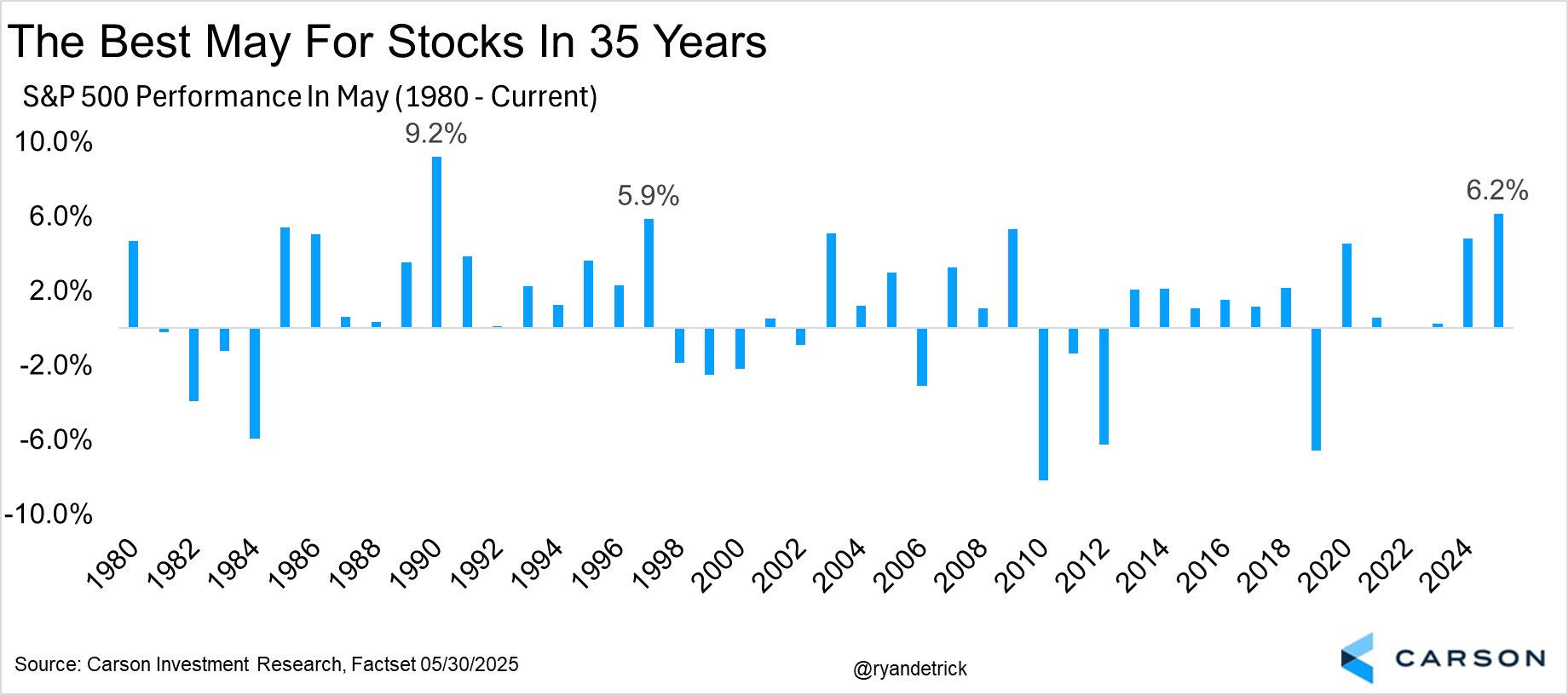

May was a strong month for markets both in the US and Australia. Even more promising is when the S&P 500 gains more than 5% in May (like 2025 6.2% return) the next 12 months have gained nearly 20% on average.

In fact, to place a more bullish perspective on this statistic – this was the best May for stocks in 35 yrs.

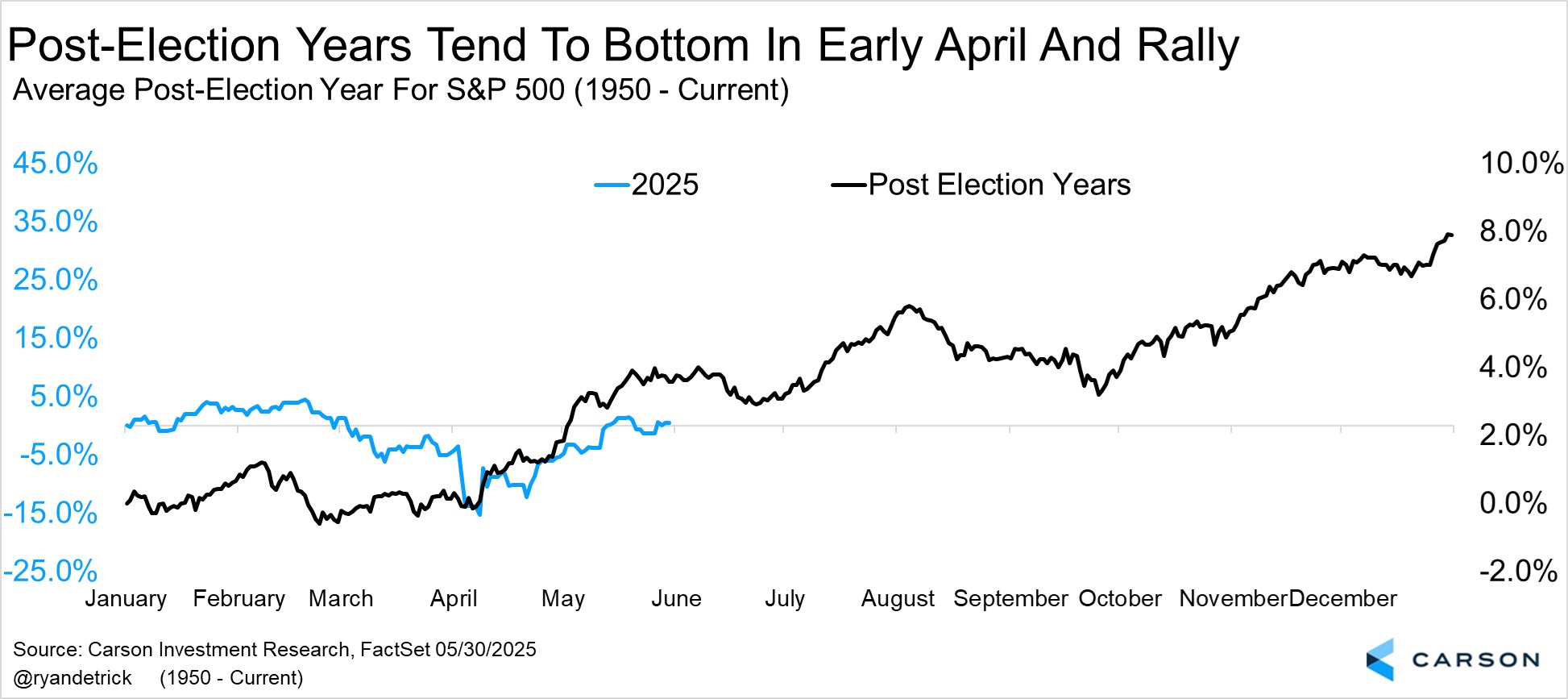

Earlier this year we also posted the average returns of the S&P500 in the first year of a new president. We highlighted to expect some sideways volatility in the first 5 months before starting to see the second half deliver strong returns.

As we mentioned, Post-election years tend to be weak early, then bottom in early April. Then they tend to rally hard in late April and May. This post-election year is playing out like they normally do – Although Trump 2.0 liberation day threw a “spanner in the works” initially with a panic selloff. If this continues, be open to a surprise 2H calendar year rally.

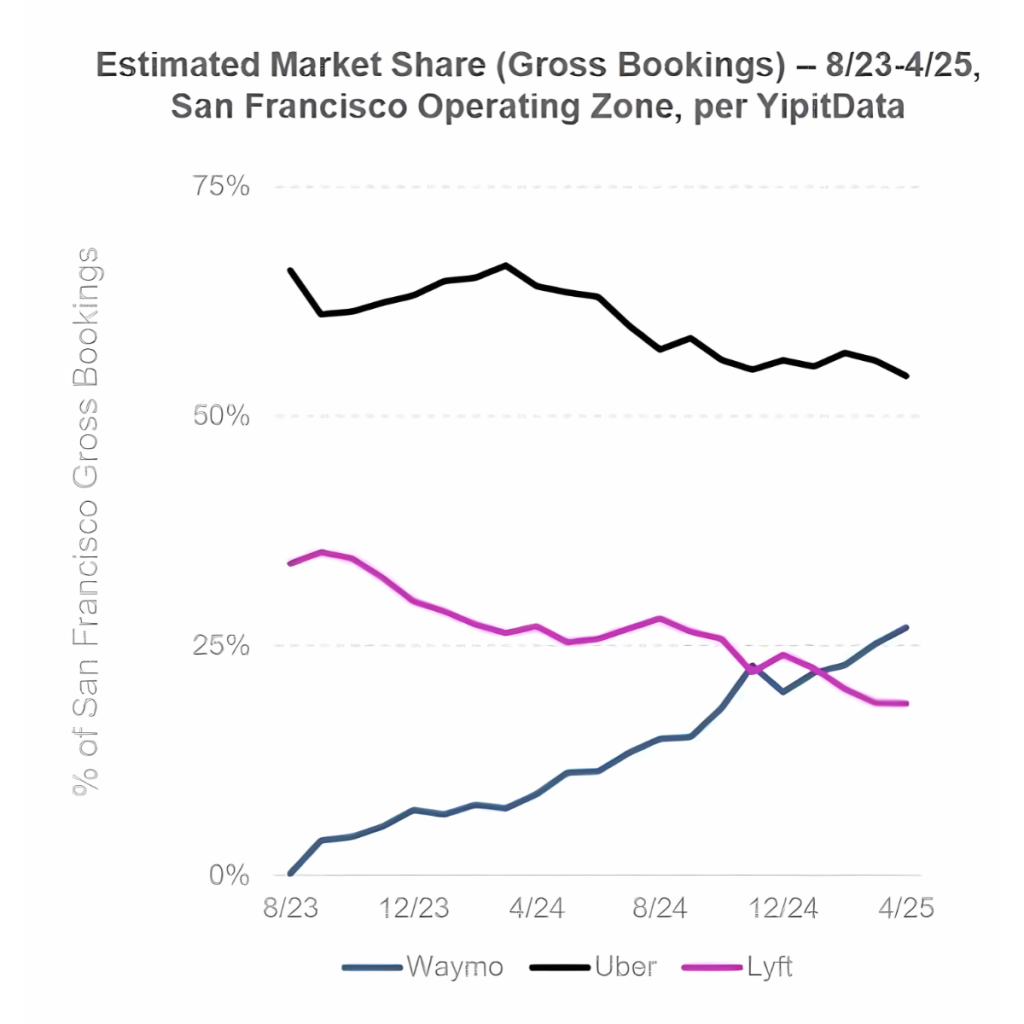

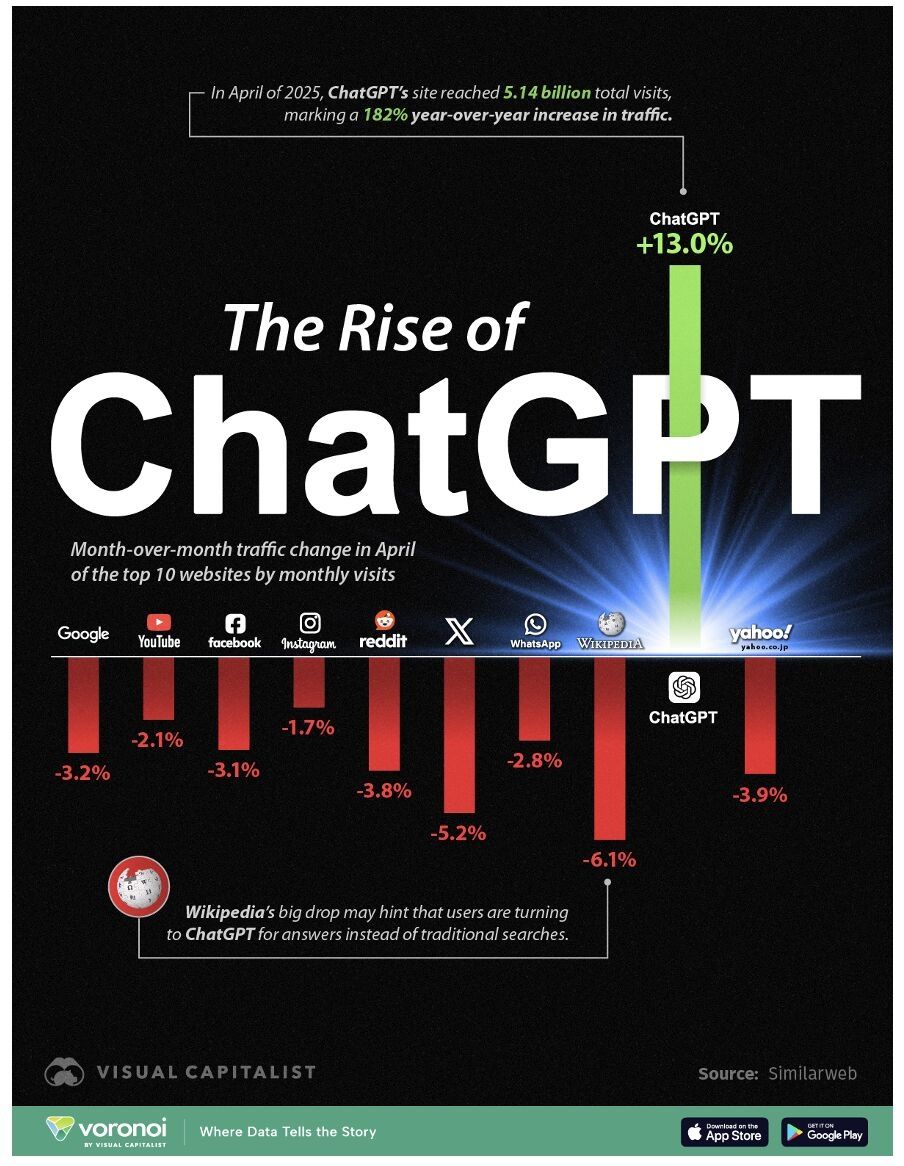

We continue to believe and as we explained in our April report, the AI thematic is gaining strength and validity. A good example is Waymo (autonomous taxis) surpasses Lyft and is on track to pass Uber in next 12 months.

And also ChatGPT taking significant online traffic share from traditional websites in April. Expect AI to disrupt certain business models we are all accustomed to and create many new ones we have not yet thought of.

Finally we provide a brief commentary on portfolio updates during the month in the portfolio section of the report. We look forward to providing further updates in our next monthly report in July.

Sincerely yours,

Ron Shamgar and the TAMIM Team.

Fund Performance

Portfolio Highlights

Webjet (ASX: WJL) reported their FY25 results in May which was overshadowed by corporate activity in the stock during the month. Back in March 2025 monthly report we wrote:

“WJL market cap is $200m with $100m of net cash. The company makes $36m of Ebitda and circa $16m of FCF. This places the stock on 3x EV/Ebitda which is incredibly cheap. Directors have been buying shares recently and so has

the fund. We believe the risk/reward opportunity here is one of the more attractive ones on the ASX. Whether management succeeds (with the new strategy) is uncertain, but we believe the company is vulnerable to an opportunistic takeover before then.”

During the month WJL saw two strategic investors emerge on the register with Bain Capital acquiring 10.8% and Helloworld (HLO.ASX) acquiring 15%. Both parties aggressively buying their stock on market during April and May. Bain followed with an underwhelming 80 cents conditional bid. The stock reached 90 cents and having acquired our position during March/April at an average price below 55 cents we decided to take the easy win and move on.

Comms Group Limited (ASX: CCG) announced the acquisition of TasmaNet, a Tasmanian communications and managed IT services provider, in a strategic $10 million deal. This move significantly enhances Comms Group’s presence in the government and corporate sectors, adding over 600 customers—40% of revenue linked to long-standing contracts with the Tasmanian Government.

The acquisition brings key network assets including fixed wireless and fibre networks, cloud infrastructure, and cybersecurity capabilities. It is expected to increase annualised revenue to ~$75 million and EBITDA to $9–$10 million. To fund the acquisition, Comms Group raised $7 million through an institutional placement and entitlement offer, complemented by a $10.7 million debt facility.

The acquisition aligns with Comms Group’s strategy to expand its service offerings and geographical reach across Australia and sees this transaction as transformational, with future growth potential in larger corporates and additional state government contracts. The stock currently trades on 3-3.5x EV/Ebitda or 5x PE. We expect the stock to re rate over the next 6 months as the company executes on guidance. We think fair value is at least 10 cents or higher.

Gentrack Group (NZX/ASX: GTK), a global software provider for utilities and airports, reported strong growth for the half-year ending 31 March 2025. Revenue rose 9.8% to $112m, with recurring revenue up 16.7% to $76.4m. EBITDA grew 5.1% to $13m, while statutory NPAT increased 34.7% to $7.2m. Cash reserves strengthened to $70.7m, from $39.3m in H1 2024.

In the Utilities segment, recurring revenues climbed 17%, though non-recurring revenues declined. Veovo, its airport technology arm, saw revenue rise 24%, driven by wins in the UK and Middle East. Gentrack continued product investment, including the rollout of g2.0 at Genesis Energy.

Major contracts included Utility Warehouse in the UK and renewals with companies across the UK, NZ, and Singapore. Veovo achieved significant milestones with deployments at airports in Edinburgh, Saudi Arabia, and London Gatwick.

Despite global uncertainty, Gentrack sees continued transformation in energy and airport sectors. It forecasts FY25 revenue of at least $230m and an EBITDA margin above 12%, with mid-term growth targets of >15% CAGR revenue and 15–20% EBITDA margin. Management hinted at significant contract wins over the next 3-6 months which will be a catalyst for the next share price re rate.

EROAD Limited (NZX/ASX: ERD) delivered strong financial and operational results for the year ended 31 March 2025. Revenue rose 6.8% to $194.4m, with annualised recurring revenue (ARR) increasing 6.1% to $175.1m. EBIT climbed to $5.9m, and normalised EBIT (excluding 4G upgrade costs) increased to $9.9m. Net profit after tax improved to $1.4m, reversing a loss of $0.8m in FY24. Free cash flow to the firm reached $16.0m, up significantly from $1.3m last year.

High asset retention (92.5%) and expansion across all markets drove growth. Key enterprise wins in NZ, Australia, and North America added $13.2m in ARR, with enterprise clients now contributing 54% of total ARR. The number of enterprise customers grew by 7%.

Co-CEOs Mark Heine and David Kenneson highlighted progress under EROAD’s reset strategy, focusing on enterprise growth and disciplined cost control. FY26 guidance includes revenue of at least $205m, ARR of $188m, and free cash flow yield of 8–10%. Medium-term ARR CAGR is expected at 11–13%.

Management highlighted 5 large contracts that are potentially near term. We see this result as a watershed moment for the stock. With $250 million market cap, negligible debt, and growing profitability and FCF we believe the stock is cheap at 1.4x ARR and 12x FCF. We believe upside is 200% from here next 12-18 months.

AI Thematic Stock Spotlight:

AI-Media Technologies (ASX: AIM) AI Media, once a traditional live captioning business, is undergoing a remarkable reinvention. Its mission: to transform into a scalable, SaaS-first AI media solutions provider. That pivot is already underway, with half of its current revenue now coming from technology-based products.

The company’s new AI-driven product suite, Lexi Captions, Lexi Voice, and Lexi Brew, is the engine of that transformation. Launched in April, Lexi Voice helps move the company away from hardware-based revenue toward recurring high-margin SaaS income.

AI Media commands an 80% market share in U.S. live broadcasting and is actively expanding into new verticals, courtrooms, classrooms, and lecture theatres, as well as geographies, particularly Europe and APAC. Management is aiming for $150 million in revenue by FY29, with Lexi products expected to drive 80% of that.

Strategic joint ventures, encoder acquisitions, and partnerships with global distribution networks could further accelerate growth. With a strong balance sheet and founder-led leadership, AI Media is one of the few AI-driven small-cap stocks in Australia with proven product-market fit and visible long-term growth levers.

Straker Limited (ASX: STG) a New Zealand-based company with a 25-year legacy, is also undergoing its own evolution. Once a traditional services business, Straker is now focused on selling AI translation tools powered by its proprietary datasets. In the AI world, data is the currency, and Straker has plenty of it.

The company’s competitive edge lies in its ability to create and validate customer-specific AI language models. This is made possible through its crowd-sourced network of 100,000 freelancers and a highly valuable historical dataset built over decades. Straker’s Verify AI product adds an extra layer of transparency, offering both automated and human-validated outputs.

One of the most exciting near-term catalysts is its Swift Bridge AI initiative in Japan. With new government mandates requiring English-Japanese financial translations for 2,000 listed companies, this program alone could unlock a significant revenue channel.

Trading at just 0.5x revenue, and with strong balance sheet backing, Straker looks undervalued. The company is also pushing hard on ecosystem development, aiming to lock in 100 partnerships within six months. In a market that’s expected to consolidate rapidly, Straker stands out as a future-ready player with real operating leverage.

Pureprofile Limited (ASX: PPL) is a lesser-known ASX-listed company that specialises in AI-powered insights and data solutions. The company collects first-party data via proprietary platforms and sells this to governments, brands, and other organisations for decision-making.

In the first half of FY25, Pure Profile generated $29.2 million in revenue (22% growth YoY) and $1.6 million in net profit. More importantly, it’s now targeting the UK and U.S. markets, 5x and 30x the size of Australia, respectively, where the appetite for data is surging.

One of the most innovative parts of its business is avatar-based video surveys, allowing companies to interact with synthetic respondents and dramatically reduce cost and turnaround time. Beyond that, Pure Profile is exploring synthetic data products, a space likely to become a foundational input in the training of large AI models.

With EBITDA forecast at $7 million next year and a market cap of only $50 million, Pure Profile looks like a high-growth AI token enabler trading at a discount. M&A opportunities, particularly in the UK and Southeast Asia, could help accelerate its expansion.

Fund Facts

Investment Parameters

| Management Style: | Active |

| Reference Index: | ASX 300 |

| Number of Securities: | 20-50 |

| Single Security Limit: | 10% (typically 5%) |

| Investable Universe: | ASX (focus on ASX300 ex20) |

| Market Capitalisation: | Any |

| Leverage: | No |

| Portfolio Turnover: | < 25% p.a. |

| Cash Level: | 0% - 100% (typically 5 - 30%) |

Fund Profile

| Investment Structure: | Unlisted Unit Trust (available to wholesale investors) |

| Minimum Investment: | $100,000 |

| Management Fee: | 1.25% p.a. |

| Admin & Expense Recovery: | Up to 0.35% |

| Performance Fee: | 20% of performance in excess of hurdle |

| Hurdle: | Greater of RBA Cash Rate + 2.5% or 4% |

| Entry/Exit Fee: | Nil |

| Buy/Sell Spread: | +0.25% / -0.25% |

| Applications: | Monthly |

| Redemptions: | Monthly with 30 days notice |

| Investment Horizon: | 3 - 5 years + |

| Distributions: | Annual |