Australian Equities

Australia All Cap

March 2026 | Investor Update

Dear Investor,

We provide this monthly report to you following conclusion of the month of March 2026.

The TAMIM All Cap Fund was down -10.16% (net of fees) during the month, versus the Small Ords down -10.96% and the ASX300 down -7.30%.

During the month equity markets have experienced heightened volatility, driven by macroeconomic and geopolitical pressures caused by the war in Iran. The escalation of conflict in the Middle East has triggered an energy shock, disrupting oil supply chains, pushing energy prices higher, and renewing inflation and rate hike concerns.

As a result, equity markets have declined sharply with increased dispersion, leading to significant mark-to-market falls. For perspective the ASX200 had its second worst March decline in history (-7.8%). The Fund drawdown was driven by market sentiment rather than any changes in fundamentals of any particular holding.

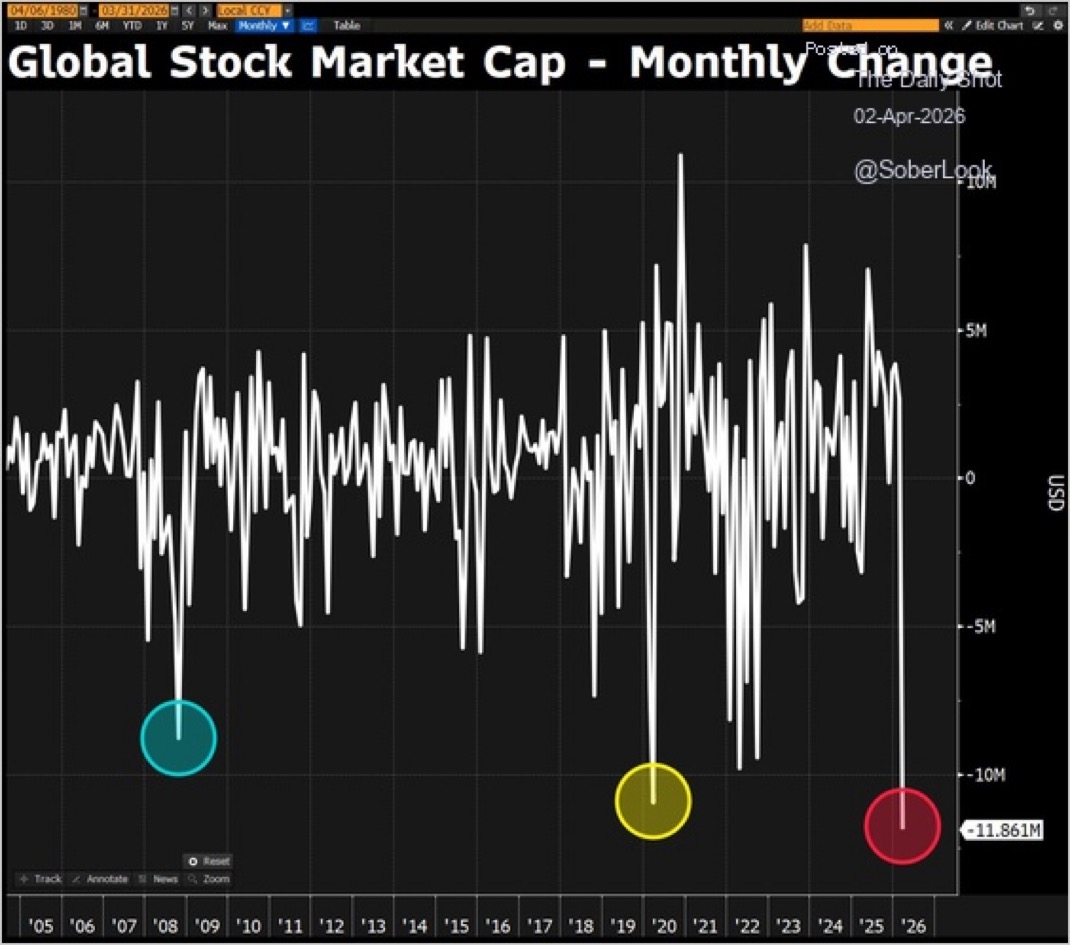

Footnote: Global equities lost $12 trillion in March, marking the largest monthly dollar decline on record.

The good news is – we have seen this before.

This environment echoes 2022, when Russia’s invasion of Ukraine caused sharp sell-offs amid spiking rates and oil prices. That episode was followed by a strong recovery as oil prices normalised.

History shows that event-driven sell-offs are typically short-lived and often present the best buying opportunities.

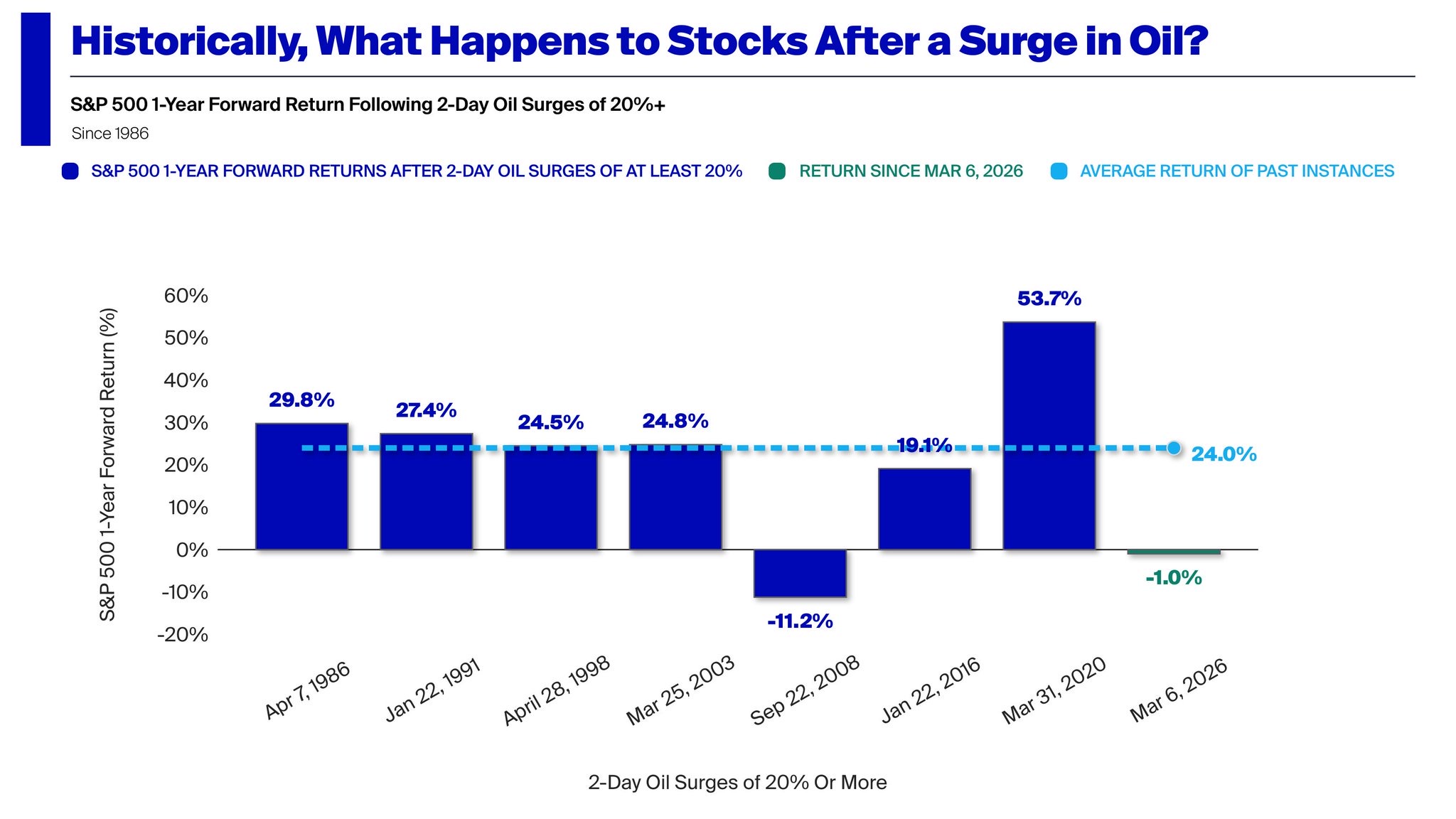

Footnote: The S&P 500 has averaged +24% in the 12 months after an oil shock.

Importantly, the fundamental outlook for many companies in our portfolio remains unchanged, despite significantly lower valuations. The majority of our holdings are not directly impacted and in most cases have significant net cash positions and the lowest valuations we have seen in a while.

We continue to optimise the Funds’ portfolios cautiously buying oversold positions whilst actively monitoring the evolving risk environment. The current conditions are creating attractive opportunities to acquire high-quality profitable growth companies at heavily discounted prices. We have identified several new and exciting positions we are currently buying. We will disclose those in the near future.

We believe these actions position the Funds strongly to outperform as markets stabilise and recover. As an example post the 2022 market selloff the Fund was up significantly over the next 3 years, annualising almost +27% pa during that period.

While near-term volatility may persist, markets are showing signs of being oversold. a setup that has historically preceded strong recoveries. As we go to print in mid April and we are already seeing a recovery in markets as the war is winding down and oil prices retreat.

Finally we provide a brief commentary on portfolio updates during the month in the portfolio section of the report. March was a relatively quiet newsflow month. We look forward to providing further updates in our next monthly report.

Sincerely yours,

Ron Shamgar and the TAMIM Team.

Fund Performance

Portfolio Highlights

Tyro Payments (ASX: TYR) updated on the RBA’s landmark reforms ending surcharging on debit, prepaid and credit cards from October 1, 2026, and capping interchange fees, including for foreign issued cards, while requiring large acquirers and schemes to publish fees.

Management says the changes promote transparency, competition and simpler pricing, benefiting small merchants and playing to Tyro’s strengths: vertical, tech driven solutions and clear pricing. Tyro expects the reforms to be disruptive for issuers, schemes and surcharging reliant acquirers but believes it can implement changes without affecting short or medium term targets.

Interchange reductions will lower merchant costs, and Tyro plans to pass savings through under its cost plus and lowest cost routing models, aiming for a net neutral impact on gross profit. The company will proactively update customers, reach out to zero cost EFTPOS users with alternative plans, and view the reforms as an opportunity to win merchants amid increased market transparency.

We think the reforms make TYR a net beneficiary which will initially see some potential aggressive pricing between competitors but will also make the company more attractive takeover target as the regulatory risk overhang is now removed. At 4x EV/Ebitda and more than 25% of the market cap in net cash, TYR is materially undervalued.

TUA limited (ASX: TUA) reported a strong 1H26 result and beat every consensus metric, with revenue rising to S$91.9m (up 26% YoY) and statutory NPAT improving to S$8.2m from S$3.0m. Mobile subscribers reached 1.412m (13% growth) and broadband services climbed to 46k, adding 20k in the half. EBITDA margin and gross mobile output improved, and positive operating cash flow supported S$18.9m CapEx.

Operational highlights include expanded roaming, surpassing IMDA’s 95% outdoor coverage benchmark, and Ookla awards for speed and reliability, fuelling broadband momentum. Management reaffirmed FY26 standalone CapEx guidance of S$50-55m, margin discipline, and noted the M1 deal remains under regulatory review with ongoing engagement.

We see the M1 acquisition as the key catalyst for the stock to re rate. The broadband opportunity is material and is starting to gain traction.

Monash IVF (ASX: MVF) is the second largest premium fertility provider in Australia with circa 20% market share. Recent highly publicized lab incidents damaged brand trust, causing modest revenue decline (−1.8%) in recent 1H26 result but a larger EBITDA hit due to elevated costs and legal expenses. Performance is regionally mixed, Victoria and NSW hit hardest, while Asia and some Australian states remain resilient.

Management prioritises stabilising new patient registrations, improving conversion times, and extracting 5% EBITDA margin improvement through procurement, labor and operational efficiencies. Strategy focuses on doctor engagement via aligned incentives, balance-sheet readiness for regulatory-driven consolidation/M&A, and disciplined organic growth while finalizing incident settlements and filling key finance leadership roles.

We initiated a position in the company at circa 64 cents as the company is trading at historically low valuation of 12x PE and 5x EV/Ebitda. The company is also paying a small dividend of 3% yield. Genesis Private Equity and Soul Patts have previously bid 80c cash but were denied due diligence access. With 19% holding and a history of improving bids (Pacific Smiles PSQ.ASX takeover) - we believe an improved takeover is only a matter of time.

Humm Group (ASX: HUM) has seen continued newsflow in relation to its takeover proposal from Credit Corp (CCp) and the activist campaign to remove the current board and controlling shareholder and founder. During the month the Takeover Panel ruled against the incumbent board handling of the CCP proposal and has enforced the company to engage and allow Due Diligence.

In addition, the court found the founders purchase of additional 3% of the company was not acceptable and an undertaking to dispose of those shares has been ordered. The EGM vote is now scheduled for May 1 and we expect a favorable outcome with the current board removed and further engagement from CCP. We see the end game as a takeover by CCP around 80 cents, although it won’t be without further distraction from the founder and their 26% shareholding.

Fund Facts

Investment Parameters

| Management Style: | Active |

| Reference Index: | ASX 300 |

| Number of Securities: | 20-50 |

| Single Security Limit: | 10% (typically 5%) |

| Investable Universe: | ASX (focus on ASX300 ex20) |

| Market Capitalisation: | Any |

| Leverage: | No |

| Portfolio Turnover: | < 25% p.a. |

| Cash Level: | 0% - 100% (typically 5 - 30%) |

Fund Profile

| Investment Structure: | Unlisted Unit Trust (available to wholesale investors) |

| Minimum Investment: | $100,000 |

| Management Fee: | 1.25% p.a. |

| Admin & Expense Recovery: | Up to 0.35% |

| Performance Fee: | 20% of performance in excess of hurdle |

| Hurdle: | Greater of RBA Cash Rate + 2.5% or 4% |

| Entry/Exit Fee: | Nil |

| Buy/Sell Spread: | +0.25% / -0.25% |

| Applications: | Monthly |

| Redemptions: | Monthly with 30 days notice |

| Investment Horizon: | 3 - 5 years + |

| Distributions: | Annual |