Australian Equities

Australia All Cap

January 2026 | Investor Update

Dear Investor,

We provide this monthly report to you following conclusion of the month of January 2026.

The TAMIM All Cap Fund was down -4.63% (net of fees) during the month, versus the Small Ords up +2.74% and the ASX300 was up +1.72%.

January saw the continued volatility we experienced since November despite a string of positive updates and profit upgrades from our portfolio holdings. The last week of the month saw a sharp selloff in any company that is technology focussed or growth biased.

The Fund’s exposure to growth companies detracted from performance and our underweight exposure to sectors currently

contributing most significantly to benchmark returns, namely Resources, Gold and the Big Banks. For example, Small Resources rose +12.5% for the month and are now up +79.6% over the past year outperforming the Small Industrials by +76.3%. This the largest annual outperformance by Small Resources over Small Industrials in the last 35 years.

In recent weeks we have seen “fear sentiment” from AI disruption spreading initially to Software exposed businesses and as we go to print in mid February, this fear has also spread to non tech companies such as freight forwarders, insurance brokers and other industries.

This fear contagion is speculated on the fact that AI will enable both new competitors to emerge and for existing clients to build internal solutions and replace incumbent technology vendors. This naive view in our mind, by the market, assumes that new competitors can magically sell unproven and unsecured enterprise grade solutions to large clients who take years to make purchasing decisions.

It also assumes that clients have the adequate resources and domain expertise of large technology vendors, to suddenly build internal tools, support them over time, and continue to update them with the latest features, whilst doing so all along on a lower cost basis – than paying long term vendors instead.

More importantly, this “AI SaaSPocalypse”, also assumes that existing technology vendors stand still and do nothing. We are not pretending that over time new technologies can emerge and will disrupt some companies that do not innovate and embrace new technologies. But to assume that an entire global industry will just stand still and not innovate and/or launch new AI solutions – is just ignorant.

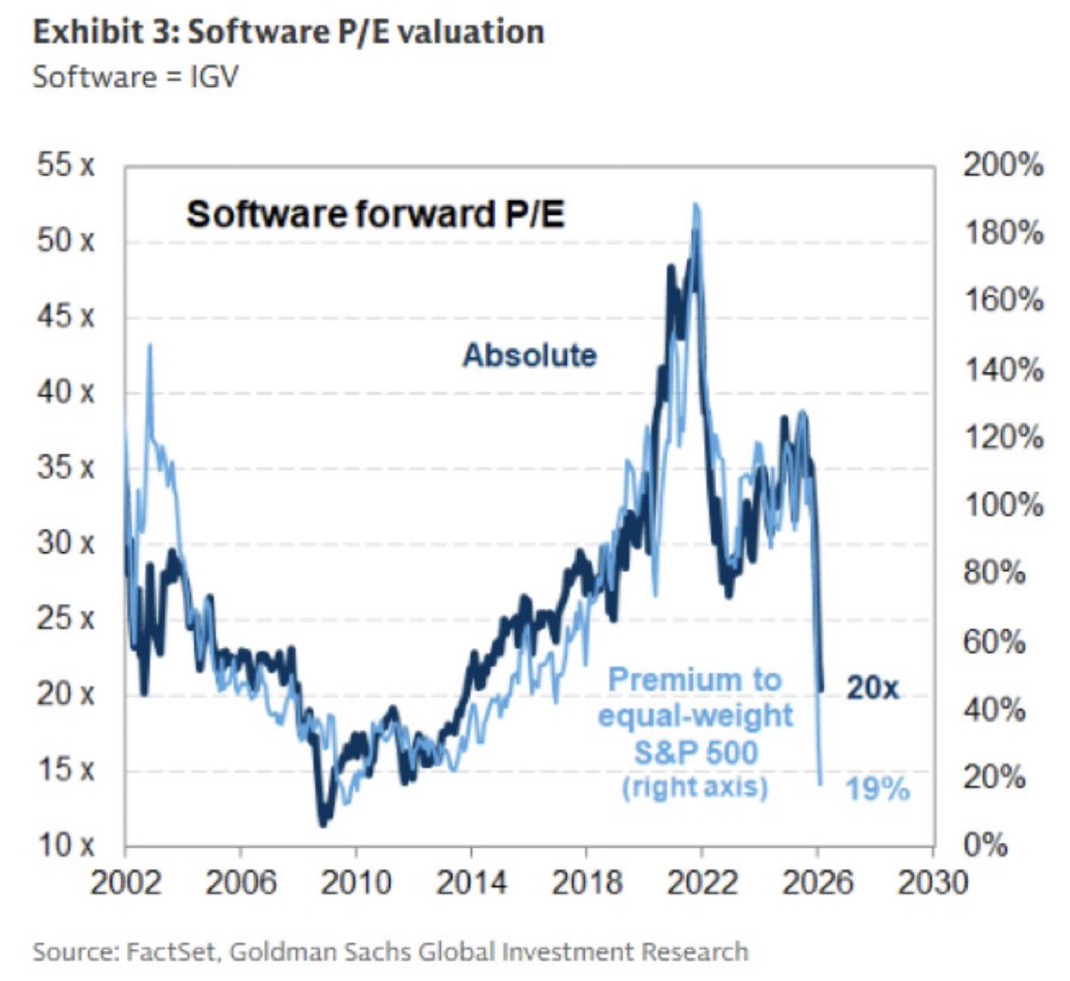

In Australia the IT sector was down -9.4% in January, while it fell a much more modest -1.7% in the U.S. This understates the fall in the U.S., where the S&P 500 Software Index was down -13.1% on the month. Software multiples just hit their lowest level since 2014. From 52x at the peak to 20x today.

Our general view is that AI is a productivity tool that will only enhance technology companies that embrace it and over time will make them even more profitable and productive. In many cases, highly profitable, growing and defensive tech businesses have fallen by -50% or more in recent months. We are taking advantage of these opportunities to capitalise on buying oversold quality growth companies. At the same time we aknowledge that short term fear selling leads to more selling elsewhere, as investors search for liquidity in unrelated sectors and stocks.

During periods like these our approach to contrarian style investing will lead us to underperform the market in the short term, but over time and time again we have shown that not only we claw back any Fund drawdowns, but eventually finish the year strong and outperform the market substantially in the medium and long term.

We provide some context to the current selloff in our spotlight article “The Ozempic moment for SaaS”. Here we explain a similar situation from 2023 where sleep apnea stocks sold off on the back of fears that weight loss drugs would reduce demand for their products – spoiler alert – they didn’t.

We also remind investors that less than a year ago the market was in complete consensus about the fear of high inflation and a deep recession from the Trump Tariff policies. At the time we claimed the market was wrong and that Tarrifs are not only deflationary but will also lead to strong US economic growth. In both cases we were vindicated to be correct and the US has just seen the lowest level of inflation since 2021 and the strongest GDP growth in the last 50 years.

We believe the portfolio is well positioned to perform in 2026 although we remind investors to expect some “air pockets” along the way – just like we experienced during 2023 and 2025 – yet we still came back and finished the year strong. We believe this year will play out in a similar manner and encourage investors to take advantage of these market drawdowns in the fund and deploy further investment incrementally.

Finally we provide a brief commentary on portfolio updates during the month in the portfolio section of the report. We look forward to providing further updates in our next monthly report in March.

Sincerely yours,

Ron Shamgar and the TAMIM Team.

Fund Performance

Portfolio Highlights

Elsight Limited (ASX: ELS) provided a FY25 and Q4 update during the month. After a breakout year, revenue climbed to roughly USD $23 million—an 11 fold increase over 2024—while the business reached profitability and closed the year with USD $59 million in cash. Management entered 2026 with USD $22 million of confirmed orders (96% of FY25 revenue), with 40% of those contracts paid upfront, signaling strong near term visibility and converted pipeline discipline. The company generated an astonishing USD $20 million of free cashflows for the year. The company aims to convert a $137M active new business pipeline into sustained growth.

Management framed the surge as the result of a “perfect storm” in defense and commercial uncrewed systems: accelerating defense budgets, demand for commercial off the shelf solutions, and the convergence of wartime and commercial delivery speeds. ELS is expanding beyond core connectivity—adding positioning, mission software, autonomy, and sensor/video capabilities—while leveraging OEM partnerships and contract manufacturing to scale without heavy capex. The Halo platform’s hardware serves as a sticky entry point to higher margin, recurring software and cloud services, with AI work grounded in 500,000 operational hours of real mission data.

Pureprofile (ASX: PPL) reported a strong H1 FY26: record revenue of $33.3m (up 14%) and EBITDA of $3.8m (up 14%), with EBITDA margin around 11%. Rest-of-world revenue grew 30% and now slightly exceeds ANZ; platform revenue surged 54% to $9.4m. Recurring annuity revenue reached $14.1m. Management upgraded full-year revenue guidance to $64–65m and targets 10–11% EBITDA margin.

Growth is driven by global expansion, platform automation, AI-enabled products (Data Rubico, synthetic respondents, conversational AI), and operating leverage from automation reducing salary growth. Priorities include UK/US expansion, cautious M&A, continued product investment, and stronger cybersecurity while maintaining client service quality and disciplined capital allocation. Trading on 7x Ebitda we see the valuation as undemanding with international growth set to accelerate group profitability.

Qoria Limited (ASX: QOR) a specialist in K-12 school safety and student wellbeing platforms serving 32,000 schools, has entered a binding merger agreement with US-based Aura Consolidated Group. Aura, a provider of AI-powered consumer security, identity protection, and family safety tools, will acquire 100% of Qoria's shares via an Australian scheme of arrangement.

Qoria shareholders will receive 1 CHESS Depositary Interest (CDI) in Aura for every 17.2 Qoria shares, equating to 35% of the combined entity's issued shares. Aura is also raising US$75 million through an equity placement from existing shareholders at 72 cents per QOR share.

The merged group boasts US$316 million in annual recurring revenue (as of December 31, 2025) and targets positive free cash flow in calendar 2026 and minimum 20% sales growth. Valued at around A$3 billion pre-placement, the combination creates a comprehensive leader in online safety across homes, schools, and beyond, with plans for Aura/QOR to list on the ASX under ticker AXQ. The deal makes sense both in strategic and financial sense and we will reassess our position over time.

Alcidion Group (ASX: ALC) had a busy month during January both winning a huge contract and releasing a pleasing Q2 FY26 Quarterly update. Some highlights include:

- Selected as preferred supplier by University Hospitals Sussex NHS Foundation Trust for EPR solution, with TCV expected to be at least $35M and potential for higher value as more modules are taken by the client.

- Q2 new TCV sales of $15.4M

- $12.3M expansion for Miya Precision modules for Leidos.

- Q2 FY26 operating cash outflow of $1.9M with cash receipts of $8.5M. The company tends to see a higher cash collection period during 2H.

- FY26 contracted revenue of $43.1M as of 31 December 2025, up 40% on pcp and 6% on FY25 full year revenue.

- Cash balance of $14.2M and no debt as of 31 December 2025 and we expect this figure to increase by June 30.

- Confirming FY26 guidance for positive EBITDA and operating cashflow in line with FY25 and potentially higher if further wins are secured during 2H.

Plenti Group (ASX: PLT) has provided a trading update for the quarter ended 31 December 2025 (3Q26). Highlights include:

- Fifth consecutive quarter of record loan originations at $480 million, 25% above PCP

- Loan portfolio increased to $2.98 billion, 24% above PCP Revenue of $79.9 million, 22% above PCP

- Annualised net credit losses of 91 basis points, down from 103 basis points in PCP Completed $559 million automotive ABS transaction

- Achieved $3 billion loan portfolio target in January 2026 which was earlier than original target of March 2026. CFO Miles Drury has resigned, effective after a four-month notice period.

PLT continues to execute well and is tracking ahead of the company forecasts. The recent rate hike in Australia has changed sentiment towards non bank lenders and we have seen PLT shares sold down despite the company shooting the lights out on profit growth. The departure of the CFO was dissapointing as he was well regarded by investors. Overall we are confident the company will keep growing and remain a takeover target for a larger player.

The Ozempic moment for SaaS

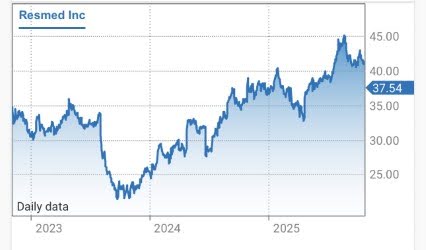

The Ozempic moment for SaaS refers to a pivotal disruption scenario where a transformative technology threatens to erode or fundamentally reshape an established market leader’s core business model, much like the hype around Ozempic (and other GLP-1 drugs like Wegovy) did to ResMed (ASX: RMD) around 2023.

Back in mid-2023, as Ozempic exploded in popularity for dramatic weight loss, investors panicked over its potential impact on ResMed, the dominant provider of CPAP machines and sleep apnea devices. Obesity is a major risk factor for obstructive sleep apnea (OSA), affecting a large portion of patients. The fear was straightforward: if millions lost substantial weight via these drugs, demand for ResMed’s hardware; masks, flow generators, and related consumables could collapse, shrinking the addressable market and pressuring recurring revenue from resupplies and adherence.

The market reaction was brutal. ResMed’s shares plunged roughly 30-40% in the second half of 2023 (from highs around $33-34 AUD to lows near $21), with some periods seeing over 25% drops tied directly to GLP-1 headlines. Analysts and headlines screamed “Ozempic overshoot” or “end of ResMed,” drawing parallels to how weight-loss drugs might cannibalize device sales. Valuations compressed sharply, with forward P/E dropping from historical averages near 30x to lows around 18-21x amid “nonsense sell-off” commentary. Investors priced in a structural decline, fearing GLP-1s would reduce OSA prevalence or adherence rates.

Yet the reality diverged. By late 2023 and into 2024, ResMed’s data showed GLP-1s as a tailwind, not a headwind. Patients on these drugs entered the healthcare system more motivated, showed higher propensity to start CPAP therapy (up to 10.5% in some analyses), and maintained stable adherence/resupply. Many used combined therapies, and not all OSA stems from obesity (about 50% of cases aren’t weight-related). CEO Mick Farrell repeatedly downplayed the threat, calling fears overblown. By 2024, shares recovered strongly, with the company beating forecasts and declaring the “headwind thesis completely gone.” The initial panic proved exaggerated; the disruption was real but incremental and slower than feared, with adaptation (e.g., hybrid treatments) preserving demand.

Fast-forward to January 2026, and SaaS faces its own Ozempic moment – this time from agentic AI and generative tools. Investor sentiment toward software/SaaS companies is overwhelmingly bearish, mirroring 2023’s ResMed rout. Stocks like ServiceNow, SAP, Salesforce, Adobe, and others have seen double-digit plunges post-earnings (e.g., ServiceNow down ~10% despite beats, SAP cratering 16% on guidance shortfalls). The Philadelphia SE Software sector is down sharply, with phrases like “SaaS meltdown” and “software apocalypse” dominating commentary.

The core fear: AI agents could replace human workflows, eroding seat-based/per-user pricing models that underpin SaaS giants. One AI agent might handle tasks previously requiring multiple licensed users, enabling in-house builds or cheaper alternatives. Horizontal/point SaaS without deep proprietary data or complex integrations looks especially vulnerable to commoditization. Investors demand immediate, exponential AI-driven growth to justify elevated valuations, yet guidance often shows steady (but not explosive) 18-20% subscription increases, triggering sell-offs.

Like ResMed’s case, though, the threat may be overstated in the short term. Agentic AI adoption remains slower than hyped due to enterprise caution around trust, governance, security, and integrations. Many incumbents (e.g., Salesforce’s Agentforce, ServiceNow) are embedding AI deeply, shifting toward outcome-based or hybrid pricing. Vertical/deep-domain SaaS with proprietary workflows could endure or thrive as AI augments rather than replaces. Insiders predict evolution, SaaS reinvented as intelligent orchestration hubs, rather than outright death.

The parallel is striking: hype drives sharp deratings, but real-world data often reveals adaptation, tailwinds, and slower disruption. For SaaS today, as with ResMed then, the market may be over-discounting extinction while under-pricing resilience and reinvention. The next 12-24 months of agentic progress and adoption will tell if this is another temporary panic—or a more profound shift.

Every investing cycle has its Ozempic moment, a narrative shock so compelling that the market briefly forgets how slow real-world change actually is.

ResMed lived it in 2023. The story was clean, frightening, and wrong in its timing. GLP-1 drugs did not kill sleep apnea. They nudged behaviour, pulled more patients into the system, and ultimately reinforced demand for therapy. The sell-off was real. The extinction thesis was not.

SaaS is now in the same psychological phase.

Agentic AI is genuinely transformative. But transformation does not arrive overnight, and it rarely destroys incumbents before they adapt. Enterprises move slowly, governance matters, integrations are messy, and mission-critical workflows are not casually handed to autonomous agents. The seat-based model will evolve, pricing will change, and margins will be pressured at the edges. That is not the same thing as obsolescence.

History suggests the winners will be platforms with deep customer embedment, proprietary data, and the ability to orchestrate AI rather than compete with it. Just as importantly, history suggests markets overshoot on fear before they recalibrate on facts.

For patient investors, these moments are not warnings to flee. They are invitations to think clearly while others extrapolate headlines. The SaaS extinction trade may yet prove as exaggerated as the ResMed panic, and the opportunity may lie in separating real disruption from narrative excess.

Fund Facts

Investment Parameters

| Management Style: | Active |

| Reference Index: | ASX 300 |

| Number of Securities: | 20-50 |

| Single Security Limit: | 10% (typically 5%) |

| Investable Universe: | ASX (focus on ASX300 ex20) |

| Market Capitalisation: | Any |

| Leverage: | No |

| Portfolio Turnover: | < 25% p.a. |

| Cash Level: | 0% - 100% (typically 5 - 30%) |

Fund Profile

| Investment Structure: | Unlisted Unit Trust (available to wholesale investors) |

| Minimum Investment: | $100,000 |

| Management Fee: | 1.25% p.a. |

| Admin & Expense Recovery: | Up to 0.35% |

| Performance Fee: | 20% of performance in excess of hurdle |

| Hurdle: | Greater of RBA Cash Rate + 2.5% or 4% |

| Entry/Exit Fee: | Nil |

| Buy/Sell Spread: | +0.25% / -0.25% |

| Applications: | Monthly |

| Redemptions: | Monthly with 30 days notice |

| Investment Horizon: | 3 - 5 years + |

| Distributions: | Annual |