Australian Equities

Australia All Cap

April 2026 | Investor Update

Dear Investor,

We provide this monthly report to you following conclusion of the month of April 2026.

The TAMIM All Cap Fund was down -1.42% (net of fees) during the month, versus the Small Ords up +3.33% and the ASX300 up +2.25%.

The fund was tracking positively during the month but performance was impacted on the last week of the month. The ASX 200 fell for 8 consecutive days at the end of April. This was its longest losing streak since 2018.

During the month the fund suffered one dissapointing downgrade from our holding in EML and benefitted from several strong updates from holdings in PPL, PLT, FCL and PME. We discuss these further in the portfolio update section of the report.

We believe the valuations of many of our core holdings are trading at extremely depressed levels. Whilst some companies have seen short term negative newsflow, the majority of the portfolio is tracking well – whilst the share prices are not reflective of the improved fundamentals. At some point sentiment will shift and the price will re rate or as we have seen in the past, corporate activity and M&A will emerge.

On a more broader view, equity markets appear resilient amid a stream of negative macro news. Yet beneath the surface, volatility tells a different story. Sentiment is outrunning fundamentals, interest rates are weighing heavily on growth stocks across the ASX and more specifically industrial small and mid caps.

Geopolitical tensions continue to generate short-term noise. With the Iran war now in a prolonged ceasefire and a US blockade on Iranian shipping routes. This has seen oil prices stay above $100 per barrel – not ideal for inflation and rate expectations.

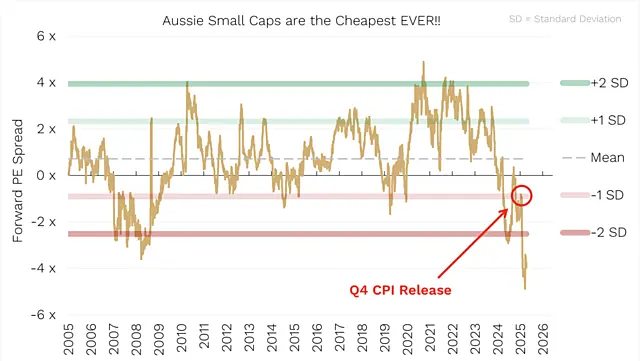

The real pressure has hit smaller companies the hardest. The Small Ordinaries index plunged -17% in just 3 months from its late January peak. Over the past 20 years, Australian small caps have typically traded at a +0.7x P/E premium to large caps. Today, they sit almost 4 P/E points lower, the cheapest relative valuation in two decades.

Sharp swings in RBA rate expectations, now pricing in around 2 to 3 hikes in 2026, have triggered a flight from rate-sensitive sectors into a handful of perceived safe stocks. While this creates risks of crowded trades, the current environment presents selective opportunities in quality small and mid cap names.

Periods of market volatility and falling share prices are an important time to reassess the overall portfolio. Rather than focusing only on individual stocks, we review the portfolio as a whole to understand how different positions, themes and risks may perform under tougher market conditions. This includes reviewing position sizes, liquidity and downside risk, while also challenging the assumptions behind each investment. In times like these we have chosen to reduce position sizing in the short term until there is more economic certainty.

These periods often help identify where conviction remains strong and where it may have weakened. Some businesses may no longer meet our expectations due to changing conditions or structural issues, leading us to reduce or exit positions. We have been very active on this front.

At the same time, market sell-offs can create attractive buying opportunities in quality companies whose share prices have fallen well below our view of fair value. We are finding some incredible opportunities we are slowly building positions in and we will disclose these over the next few months. We have materially changed some of the companies in the portfolio which we believe will drive strong performance over the next 6-12 months.

We understand that market downturns can be challenging for investors and often test confidence and discipline. We believe it is important to communicate openly about portfolio performance, what is driving results, the risks we are monitoring and where we are finding opportunities.

It’s important to remain invested in times like these, as much as it feels uncomfortable, noting that share markets have historically rallied in the later stages of geopolitical conflicts. Less liquid small cap names tend to initially lag the larger more liquid stocks but overtime have shown to outperform.

For example after a similar large drawdown in the first half of 2022, the fund took several months to recover, but once the recovery began, the Fund was up close to +100% over the following 3 years. Investors who persevered and took opportunity of the volatility – were rewarded.

Finally we provide a brief commentary on portfolio updates during the month in the portfolio section of the report. We look forward to providing further updates in our next monthly report in June.

Sincerely yours,

Ron Shamgar and the TAMIM Team.

Fund Performance

Portfolio Highlights

Fineos (ASX: FCL) released its Q1 2026 update with record customer cash receipts of €56.5 million, up significantly, driven by strong subscription collections. Closing cash balance strengthened to €47.1 million. Key operational highlights included successful implementations of AdminSuite, new contract wins (including a North American client and Motor Accidents Insurance Board of Tasmania), and continued pipeline momentum.

Fineos reaffirmed its FY26 revenue guidance of €147-152 million, underscoring its transition to a more predictable, cash-generative SaaS business model with improving free cash flow generation. The stock rallied to $2.90 during the month and we took some profit. FCL is now a cash generative business and any large contract wins could see a continued re rate of the company.

Pureprofile (ASX: PPL) released its strong Q3 FY26 business update. Group revenue reached approximately $14.8 million, up 17% on the prior corresponding period, with balanced contributions from ANZ and ROW markets. Platform revenue doubled, while EBITDA surged 67% to $1.0 million (7% margin). The CRNRSTONE acquisition contributed positively. Top 25 clients grew strongly, annuity revenue increased, and cost discipline supported margins.

The company reiterated full-year FY26 guidance of $64-65 million revenue and 10-11% EBITDA margin, highlighting platform leverage, AI-driven solutions, and positive momentum across its data and insights business. The stock has de rated materially last few months as the business fundamentals have continued to improve. Trading on 5x EBITDA and a net cash balance sheet makes PPL highly vulnerable to a takeover in the near term.

Raiz Invest (ASX: RZI) issued its Q3 FY26 quarterly update with Key metrics showing continued growth with Active Customers around 340,000 levels, improved ARPU, and Funds Under Management (FUM) reaching approximately $2.04 billion (up over 20% YoY, with further growth noted). Jars portfolios expanded strongly.

The company maintained positive cash position of $14.6 million and highlighted upcoming product enhancements with direct ASX and US trading of individual stocks, instant payments, award wins for features like Round-Up and Kids investing, and solid engagement metrics. Raiz remained on track for its FY26 Underlying EBITDA guidance of $4.5 - $5.5 million. The company is on 9x EBITDA and we believe is a highly attractive platform for a large global bank, or investment platform to target a younger underserved demographic.

EML Payments (ASX: EML) announced a material revision to FY26 Underlying EBITDA guidance, lowering it by around 20% to $47-50 million (from $58-60 million). Reasons included delayed program go-lives shifting revenue to future periods and softer-than-expected Northern Hemisphere trading due to weaker consumer demand and macroeconomic uncertainty. New business wins continued ($2.5 million additional forecast annual revenue), and strategic initiatives like Project Arlo remained on track.

We have underestimated the difficulty of the EML turnaround story. We like to back successful management teams that have skin in the game. EML exec chair has done this before and has spent $4.2 million of his own money acquiring shares at prices averaging over 80 cents. It seems even he underestimated the time it wil take to turn the business around.

In saying this, a large part of the downgrade is not lost revenue but timing related so we expect a good bounce back in FY27. In addition the new mobility vertical has significant potential and is expected to launch within 6 months. We see a $5-$10 million EBITDA contribution just from existing salary packaging clients in Australia alone. The global fuel card market is huge and ripe for disruption. We have reduced and de risked the position and will re assess in the August results.

Pro Medicus (ASX: PME) is a new position we initiated at $118 during the recent SaaSPocalypse selloff. PME is the market leader in US radiology software with approximately 10% share. The company exhibits the highest quality financial metrics we have ever seen in the entire world. Profit margins are over 70% with incremental margins close to 80%. The company generates significant FCF and has a cashed up balance sheet to match.

In April PME delivered significant US contract momentum announcing a 5-year A$23 million Visage 7 (Viewer and Workflow) cloud contract with University of Maryland Medical System on a transaction-based model, with Medicine at improved terms (higher minimums and per-exam fees).

These wins reinforced strong demand for Visage’s enterprise imaging and AI solutions with increasing traction in its cardiology product suite. We believe AI can only make the company more profitable in the future. The company has never been “cheap” but on 66x PBT multiple growing at 30% pa for the next 3 years is an attractive entry point for this incredible business. Insiders have been net buyers recently.

Plenti Group (ASX: PLT) provided Q4 FY26 update highlighting record performance, including record Cash PBT/profitability of $30.6 million. Quarterly loan originations were strong ($475 million) across auto, personal, and green loans, supported by the NAB partnership ($121 million loan book). The loan book surpassed $3.1 billion milestones ahead of schedule.

Credit quality remained solid with well-controlled arrears. The company will report its results in May and will announce a new product vertical. PLT has only $20 million of corporate debt and is highly cash generative. Trading on 5x Cash NPAT, we see significant upside once the rate hiking cycle in Australia ends and non bank lenders see improved sentiment. We believe as the NAB loan book grows materially over time it will place the company in the crosshairs of NAB.

Fund Facts

Investment Parameters

| Management Style: | Active |

| Reference Index: | ASX 300 |

| Number of Securities: | 20-50 |

| Single Security Limit: | 10% (typically 5%) |

| Investable Universe: | ASX (focus on ASX300 ex20) |

| Market Capitalisation: | Any |

| Leverage: | No |

| Portfolio Turnover: | < 25% p.a. |

| Cash Level: | 0% - 100% (typically 5 - 30%) |

Fund Profile

| Investment Structure: | Unlisted Unit Trust (available to wholesale investors) |

| Minimum Investment: | $100,000 |

| Management Fee: | 1.25% p.a. |

| Admin & Expense Recovery: | Up to 0.35% |

| Performance Fee: | 20% of performance in excess of hurdle |

| Hurdle: | Greater of RBA Cash Rate + 2.5% or 4% |

| Entry/Exit Fee: | Nil |

| Buy/Sell Spread: | +0.25% / -0.25% |

| Applications: | Monthly |

| Redemptions: | Monthly with 30 days notice |

| Investment Horizon: | 3 - 5 years + |

| Distributions: | Annual |