Author: Sid Ruttala

But hang on a minute, how have inflation fears catalysed a sell-off in gold? Isn’t it meant to be a hedge? And why are energy prices so resurgent despite a considerable segment of the planet still in lockdown? Moreover, the yields at the long-end of the curve that’s on everybody’s minds are at a stellar 1.37% on US 10-years, I don’t know about the readership, that doesn’t sound like a particularly attractive prospect to me. This is especially the case when official targets for inflation are around 2% (depending on country), you’re effectively telling me I should lend you money and you will pay back less than what I gave you 10-years from now? So let us try and unpack that for a moment.

Do treasury yields actually mean what they used to?

Let me give you a couple of simple statistics.

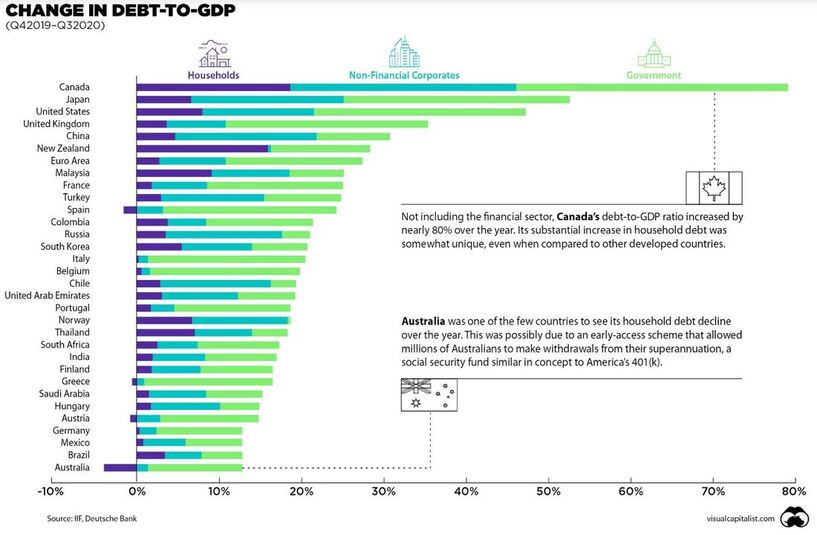

365%. That is the estimate of the global debt-to-GDP ratio to finish 2020.

106%. That was the public debt-to-GDP ratio in the US to end 2019. It is now closer to 130% (and likely to continue to grow disproportionately given the packages and budgetary measures currently under review on the Hill).

Think through this for a moment, what does even a 10 basis point increase in yield on the long-end imply in terms of debt servicing? More importantly, is any central bank likely to stomach that increase?

We have already seen Christine Lagarde of the ECB make a statement mentioning that they will be closely monitoring yields on the long-end. Stateside, Powell might very well be in a similar situation. This is not the same as the days of Volcker where debt-to-GDP ratios were a more manageable 70-80%. The tax base is not enough across most of the western world to support increases to debt-servicing requirements. The ruling out of yield curve control Stateside will, in my view, go the same direction as Lowe’s ruling out of QE in Australia back at the beginning of last year.

The government will issue, the central bank will buy, thus creating more money supply. Yes, I’ve just said it, debt monetisation. In fact, since the beginning of covid-19 the Federal Reserve has bought close $3.5tn in bonds in 2020 alone, the Bank of England allowed an overdraft of the government account and Australia has seen its central bank buy government securities, though on the shorter end of the curve, to put a lid on the yields.

Why inflation now?

It was during the depths of the GFC that central banks embarked upon then unconventional policy in the form of quantitative easing (after a certain amount of time, unconventional becomes conventional). Many doomsayers suggested that this might give rise to runaway inflation. It didn’t. Because they forgot one thing, increasing bank reserves doesn’t necessarily translate into the real economy, it just shows up in asset valuations rather than consumer discretionary spending.

However, where things change and the real economy gets impacted directly is direct stimulus measures. Take, for example, the stimulus cheques now under consideration. That is new money supply into the economy. Similarly, infrastructure projects that add to GDP but also contribute actual jobs. This comes along at the same time as increasingly frosty relationships between the major geopolitical powers of the day. I am of the view that technology wasn’t entirely the reason for the deflation of the past, rather the greatest deflationary event of the past two decades was China, which not only enabled cheaper production but stagnant wage growth across most of the western world. Something that, somewhat ironically, was good for the investor, may not have been the case for the average wage earner but, lets face it, we’ve done well out of it.

This situation of globalised supply chains led to things like Just-in-Time inventory systems, centralisation of healthcare systems, lowest cost production. All seemingly good things but what it also does is underinvestment in those very things as the costs continue to be driven down.

What happens when bottlenecks are introduced out of the blue, tough? A bottleneck like an economic lockdown due to a pandemic perhaps? Re-localisation of supply chains because of a shift in geopolitical priorities/government policy? Last week I wrote about the shortage in semiconductors within the automotive segment. We are seeing similar things in commodities, such as copper, which saw massive underinvestment for close to a decade due to uneconomic prices. But what happens if you add in potential for infrastructure projects, like renewables, while at the same time lacking an existing supply pipeline to deal with the increase? Is it any wonder that the Chinese have been the most aggressive buyers within that particular market?

So what am I trying to say?

I remain exceptionally bearish on global treasuries and USD overall. What we have seen through much of the year so far are short-term pivots. Precious metals are not selling off because the yields make such an attractive proposition, it is rather investors taking cash off the table after a run-up in the market to move towards re-allocation. If you sell-off your treasuries, the process is first to cash before you make a further allocation (thus putting a short-term upward pressure on the currency). In circular trajectory, once that happens and the yield goes up even slightly, it is the high-growth stocks (precisely those that have done well during Covid) but stand on premium valuations that get sold off (all of a sudden you can use a discount rate). Similarly, a short-term spike in the USD leads to a short-term sell-off in Gold due to the inverse correlation.

I remain of the conviction that we will see inflation coming back into the picture but not yet and yields certainly will not be going up in proportion. This is not necessarily a bad thing for the investor. It should only be concerning if said picture gets out of hand. We will continue to see accommodative monetary policy that drives markets but with the caveat that some of the higher-growth names you are used to might not see the same returns. More importantly, as fiscal expansion continues across most of the developed world, we will see every indicator of broad money supply increase and ridiculous valuations across anything that has scarcity value (even Bitcoin, though this author doesn’t quite understand that particular market).

What has been interesting to watch is the money flow towards pockets such as the Dow, industrials and emerging/Asian markets.

How to allocate?

In every economic expansion cycle over the past two centuries, inflation doesn’t hurt in the initial stages. As governments continue to occupy a greater proportion of GDP, we will see two things happen, household debt will proportionally decrease (i.e. crowding out) and corporate debt remains somewhat manageable (take a large firm such as Berkshire, for example, which issued debt at 105bps in 2020) as you effectively eat away the real value of the debt. We might quite literally have the Roaring Twenties roar back to life.

Remember that your portfolio should have three different pockets; the contrarian, income/defensive and a growth pocket. These react in different ways depending on the situation. Your defensives won’t do well in a bull market but that’s how they’re supposed to behave, precious metals fall in this category too (it doesn’t yield anything and it has no intrinsic value but it is an evergreen hedge against uncertainty, not inflation but uncertainty). Your growth will be healthcare and technology with the caveat of long secular growth stories, not the hype of the day, but SECULAR. Think about artificial intelligence, mobility or emerging markets. The third pocket, the contrarian, is the one that is an allocation assuming you have everything wrong (i.e. not contrarian to the market but contrary to your base case). Again for Australian investors, strap your belts, we are the beginning of a bull cycle in commodities.

Disclaimer: The Roaring Twenties (a name coined by Fitzgerald) weren’t “roaring” for everyone, with the most common job in the US being farming/agriculture. Harding was exceptionally kind to the investor, much like one recent ex-President, and the economy had deflation as opposed to inflation. In the words of Twain, “History doesn’t repeat itself, but it often rhymes.”

Conclusion? The music is still playing for now, it might even get louder. Dance while you can.

This is definitely worth thinking about at some point but it shouldn’t affect your investing decisions just yet.

And now a non-exhaustive list of other things life is too short to worry about:

- Having one more TimTam

- The lack of fundamentals behind Tesla’s share price

- Gossip

- Missing the train/bus

- What happened last night on MAFs