Australian Equities

Australia Small Cap Income

Investor updates

Below you will find this month’s commentary and portfolio update for TAMIM Australia Small Cap unit class.

September 2024 | Investor Update

We provide this monthly report to you following conclusion of the month of September.

The TAMIM Small Cap Fund was up +6.93% (net of fees) during the month, versus the Small Ords down -5.09%.

Over the last 12 months the fund is up +24.88% net of fees versus the Small Ords up +18.84%.

September is historically known as the most challenging month for equity market returns, but this year, it proved to be a positive outlier. The primary driver behind this robust market performance was the U.S. Federal Reserve’s decision to cut interest rates by 50 basis points, with indications of further reductions in the next six months.

We have consistently emphasised that rate cuts tend to be a strong catalyst for stock market performance, particularly for small and mid-cap stocks. This was evident in September as smaller companies outperformed, while large caps lagged. We anticipate this trend to persist in the months ahead.

Additionally, positive sentiment was bolstered by the Chinese authorities’ announcement of significant stimulus measures aimed at revitalising their economy and boosting consumer spending. As China is a key economic partner for Australia, this has promising implications for our economy.

As we have noted throughout this year, we believe we are in the early stages of a new bull market—driven by AI innovation and investment—that, based on historical patterns, could extend for the next 5 to 10 years. Our portfolio is strategically positioned to capture growth opportunities and undervalued stocks within the small and mid-cap segment.

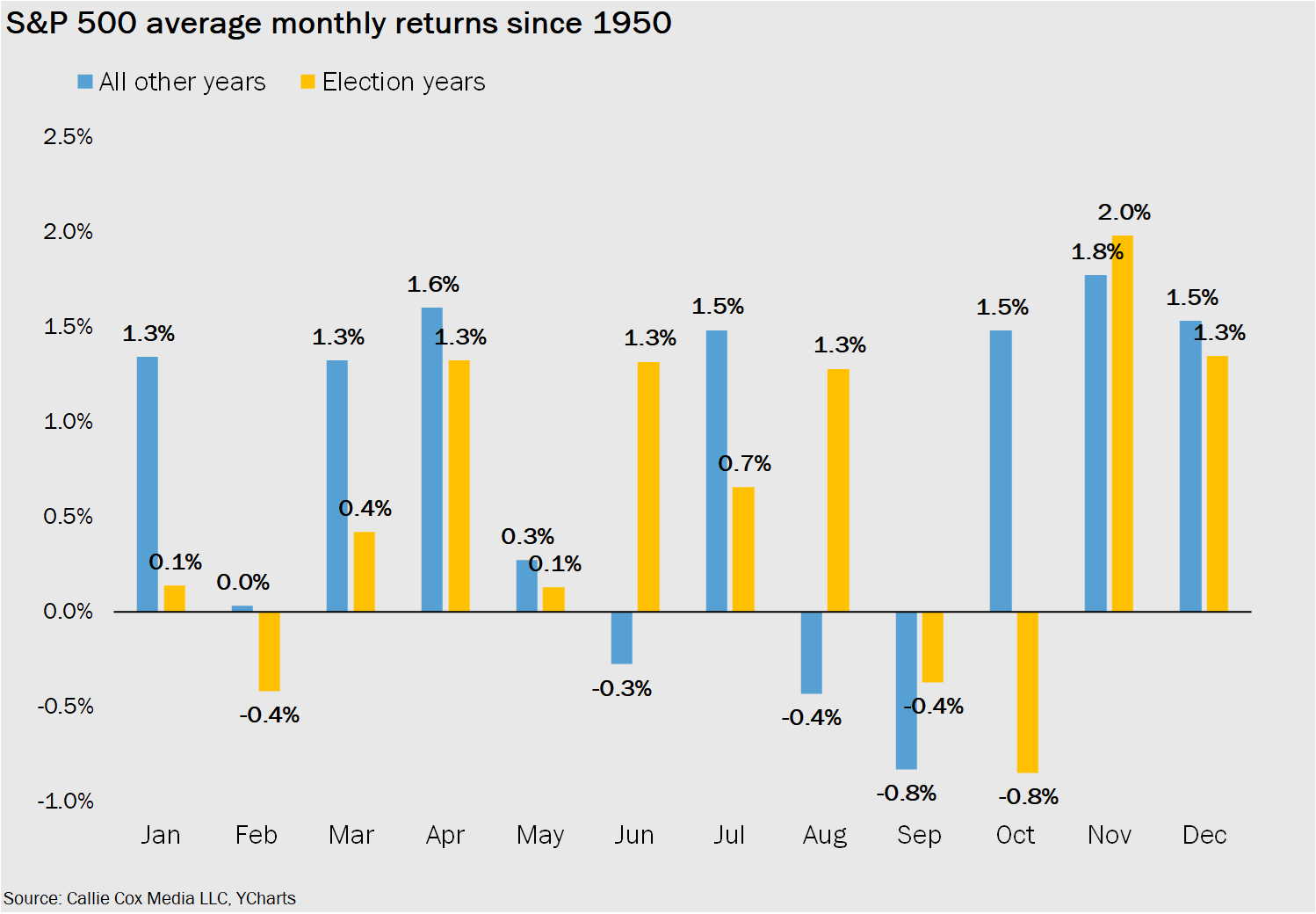

As we enter the final quarter of the year, we anticipate some volatility in October due to geopolitical tensions in the Middle East and uncertainty surrounding the upcoming U.S. elections. However, once this uncertainty subsides and the election results are clear in early November, we expect the market to rally into the year-end and beyond.

Further details on portfolio updates for the month can be found in the portfolio section of this report. We look forward to sharing more insights in our next monthly update in November.

Sincerely yours,

Ron Shamgar and the TAMIM Team.

Fund Performance

Portfolio Highlights

")

Praemium Limited (ASX: PPS) a provider of investment platforms and portfolio administration services, has been making waves in the financial technology sector. The company delivered solid financial results for the year, with EBITDA reaching $21.5 million. This represents a notable improvement on market expectations, driven by a particularly strong second-half performance. EBITDA increased by 42%, rising from $9 million in the first half to $12.5 million in the second half. This uptick in profitability reflects Praemium’s ability to control expenses while capitalising on strong revenue growth.

In fact, Praemium’s revenue for the second half grew by 15%, reaching $84.9 million, an indication of the company’s robust market position and price increases. This growth was underpinned by Praemium’s investment in capability, resilience, and IT security during the first half, which laid the groundwork for its subsequent financial success. Praemium’s scalable business model has positioned it well within the industry, with $57.4 billion in assets under administration, reflecting the company’s broad reach and strong standing in the financial services space.

One of the key strategic moves that has contributed to Praemium’s growth was the acquisition of the OneView business from Iress (IRE), a decision that has proven to be both strategic and revenue boosting. The acquisition enhanced Praemium’s revenue and EBITDA, further solidifying its position as a key player in the sector. The company’s ability to integrate the new business seamlessly while maintaining strong financial discipline is a testament to its management team’s expertise.

Looking ahead, Praemium’s growth prospects appear strong. The company has identified a gap in the market for next-generation IDPs (Investment Data Platforms), which it is poised to address with its new offerings. This product innovation is expected to drive further revenue growth and expand Praemium’s customer base to address the non custodial market for high net worth investors. Additionally, the company has remained committed to disciplined capital management, evidenced by its 1-cent dividend declaration and its ongoing on-market share buyback program. Praemium’s net cash position of $44 million provides the company with ample financial flexibility to pursue further growth opportunities.

Praemium’s management team is optimistic about the company’s future, with our estimate projecting EBITDA of $28 million for FY25. With the company trading at an EBITDA multiple of 8.5x, it remains an attractive option for investors seeking exposure to the financial technology sector and dividend income. Praemium’s combination of strong revenue growth, operational efficiency, and product innovation makes it a compelling investment opportunity in a consolidating sector.

Australian Clinical Labs Limited (ASX: ACL) a leading provider of pathology services in Australia, reported solid financial results for the fiscal year. Despite a significant 59% decline in COVID-19-related revenue, ACL managed to deliver flat total revenue of $696.4 million, a testament to the company’s ability to maintain stability in its core business operations.

ACL’s underlying EBIT came in at $62.6 million, in line with the company’s FY24 guidance. However, the second half of the year was particularly strong for ACL, with underlying EBIT improving to $39.1 million, representing an 11% margin. This is a significant improvement compared to the first half, where underlying EBIT was $23.4 million, with a margin of 7%. The company’s ability to drive margin expansion in the second half of the year reflects the success of its cost control measures and its focus on operational efficiency.

ACL has carried this positive momentum into FY25, with strong growth already evident in the early months of the fiscal year. In July, ACL reported revenue per working day growth of 7.6%, alongside volume growth of 5.9%. The company’s FY25 EBIT guidance of $65-$72 million suggests that ACL is well-positioned to continue delivering strong financial performance in the coming year.

The clinical sector, in which ACL operates, has benefitted from improving general practitioner attendance volumes and a focus on cost controls, which has enhanced profitability across the board. Furthermore, recent mergers and acquisitions in the radiology sector have bolstered investor sentiment to healthcare stocks. For example, IDX’s acquisition of CAJ at 10x EBITDA and HLS’s sale of Lumus at 15x EBITDA have highlighted the value within the sector. In contrast, ACL is currently trading at a single-digit EBITDA multiple, making it a relatively undervalued player in the healthcare space.

ACL also benefits from a strong balance sheet, with a healthy cash position that provides the company with the financial flexibility to pursue growth opportunities and return capital to shareholders. The company’s dividend yield remains attractive, offering investors a steady income stream alongside the potential for capital appreciation.

One recent development that has positively impacted ACL’s stock performance is the exit of Crescent, the company’s largest shareholder, which sold its 30% holding. This move has removed a significant stock overhang and improved liquidity, making ACL more accessible to a broader range of institutional investors. Additionally, the company is now well-positioned for potential inclusion in market indices, which could further enhance its stock’s visibility and attractiveness.

Looking ahead, ACL appears poised for a re-rating, particularly if it continues to deliver strong financial results in FY25 where we estimate it is highly likely to upgrade guidance at the AGM or first half result. The company’s competitive positioning, strong balance sheet, and improving market conditions make it an appealing option for investors seeking exposure to the healthcare sector.

SRG Global (ASX: SRG) completed raising $66m of equity for the recently announced acquisition of Diona for $111 million. The Acquisition Price implies an FY24 EBIT multiple of 6x and is expected to be circa 10% EPS accretive to FY24 earnings pre any synergies and is expected to be accretive to margins.

The acquisition is highly strategic, with Diona’s market leading position in program and asset management services in water security and energy transition with utilities / government agencies under long-term collaborative program and asset management agreements, complementing SRG Global’s current end-to-end full asset life cycle capability in water, defence, resources, transport and energy transition.

The combined group brings together two highly complementary businesses that provide significant cross selling opportunities with existing and complementary clients and further embeds SRG Global’s strategic transformation towards annuity / recurring earnings with the Company’s overall group profile post-acquisition of 80% annuity / recurring earnings.

We took the opportunity to top at the equity raise price of 83 cents with the shares trading at $1.10 during the month. Having first bought into SRG around the 50s cents mark, the stock has delivered exceptional returns for the fund last couple of years. Following the strong run in the shares we have taken the opportunity to reduce our position. Market consensus for FY25 is 9 cents eps and so the stock is trading on circa 12x PE - around fair value for now.

Fund Facts

Investment Parameters

| Management Style: | Active |

| Investments: | Australian Equities |

| Investment Universe: | Australian Small Cap |

| Reference Index: | ASX Small Ords |

| Number of Securities: | 20-40 (10-20 Value, 10-20 Growth) |

| Single Security Limit: | +/-5% |

| Market Capitalisation: | Small Cap |

| Leverage: | No |

| Portfolio Turnover: | <50% p.a. |

| Cash Level (typical): | 0-100% (0-50%) |

Fund Profile

| Investment Structure: | Unlisted Unit Trust (available to wholesale investors) |

| Minimum Investment: | $100,000 |

| Management Fee: | 1.25% p.a. |

| Admin & Expense Recovery: | Up to 0.35% |

| Performance Fee: | 20% of performance in excess of hurdle |

| Hurdle: | Greater of: RBA Cash Rate + 2.50% or 4% |

| Entry/Exit Fee: | Nil |

| Buy/Sell Spread: | +0.25% / -0.25% |

| Distributions: | Semi-annual |

| Applications/Redemptions: | Monthly |

| Redemptions: | Monthly with 30 days' notice |

| Investment Horizon: | 3 - 5 years + |

Invest via TAMIM Fund

Request additional details by using the form or if you're ready to invest select the apply now button.

Invest via IMA

The TAMIM Australia Small Cap strategy is available as an Individually Managed Account (IMA). Please see the Strategy Summary for terms or request Investment Documentation via form.