Listed Property

Investor Updates

January 2025 | Investor Update

Dear Investor,

The TAMIM Listed Property unit class delivered a 2.71% return for the month of January 2025. For comparison the A-REIT index was 4.66% while the G-REIT index was 1.39%.

Australian Listed REIT Portfolio (AUD)

The A-REIT market was off to a positive start in 2025 and recouped most of the negative returns from the last month of 2024. The A-REIT market was up 4.66% in January, similar to the ASX 200 which was up 4.57%. Looking at the global REIT market, the Australian component beat it handsomely in January, where the GPR 250 REIT World Index was up 1.39% in AUD. On a 12-month rolling period the A-REIT market has now delivered 18.15% total return, compared to the ASX 200 which came in with 15.17% and the GPR 250 REIT World Index which delivered 15.87% in AUD.

We saw solid performance across all sectors of the A-REIT market in January. The top performing sector was Office (+9.0%), followed by Diversified (+6.7%) and in third Retail (+6.2%). The only real negative sector was the Storage sector (-3.8%), which comes from a single stock in the sector namely National Storage REIT (-3.76%). We have seen volatility in the asset class in recent times that seems to be continuing into 2025. For many months the winners of the previous month are the losers of the following month and vice-versa. There continues to be macro uncertainty in the market, and this generates speculation and volatile market movements.

Ingenia Communities Group (INA) was the best performing stock in the portfolio for the month, delivering 25.79%. INA upgraded their FY25 guidance with EBIT expected to see growth of 20-23% (versus 10-15% previously) and underlying EPS now expected to be 29-30c (versus 24.4-25.6c previously). INA’s guidance upgrades were based on lower operating costs from simplification, contributions from new projects, lower levels of drawn debt and a lower tax expense. CHC (+9.96%) and DXS (+9.61%) also delivered excellent returns for the month but had no major company news being released. For Dexus, recent office data has pointed to a faster recovery in Sydney and improvement in the Office sublease space available, as was evidence by the performance of the overall Office sector. NSR (-3.85%) was the worst performer for the month, there was no significant drivers from news releases for the month justifying the underperformance.

There was no interest rate decision meeting by the RBA in January. The last meeting was in December and the rate was kept constant at 4.35% at the meeting, as expected by the market. The last hike by the RBA was in November 2023. The RBA has not cut rates since the start of the hiking cycle in May 2022, but it is widely anticipated that a cut is on the cards for the meeting to be held in February based on inflation sustainably moving to the mid-point of the target range of 2-3%, even though there is still an uncertain economic outlook.

The Australian monthly CPI Index data for November and December was released in January 2025. November read a year-over-year increase of 2.3% and December a year-over-year increase of 2.5%. December hit the mid-point of the target range and was in line with market expectations. December was the highest reading since August 2024 and stems to some extent from the waning of the government energy rebates becoming more evident. Electricity prices fell the least in a year (-17.9% vs -21.5% in November) while automotive fuel costs dropped much slower due to base effects (-1.4% vs -10.2%). Prices grew further for food, alcohol and tobacco, clothing, housing, household services, health, recreation & culture, education, and insurance and financial services.

The A-REIT market seems to have limited relief expected from debt costs for the year ahead with a possible 3 rate cuts expected. The phrase “higher-for-longer” as we have heard on the global stage is seemingly also holding up down under. Most A-REITs however have learnt from the past and have positioned themselves to be well hedged with less debt than historically held.

The A-REIT market outlook for 2025 is slightly positive, with analysts expecting a 10-15% return. Australia’s strong economic institutions support long-term stability, though short-term challenges are anticipated due to continued tight monetary policies.

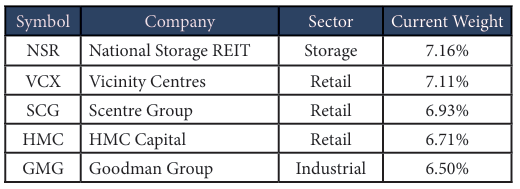

The current Australian portfolio component consists of 24 stocks. Below are the top 5 holdings:

Reitway Global Property Portfolio (USD)

The Portfolio delivered 2.02% during January compared to 2.14% by the GPR 250 REIT World Index. It was a relief to see some positive returns after the December slump and on a 1 year rolling basis the Index is now up 9.47% compared to 1.61% at the end of 2024. Some normality has returned since December, but we anticipate volatile markets to continue during 2025 with global tensions possibly being raised from time to time by the Trump Administration’s way of approaching matters. This creates uncertainty, but on the other hand it also creates opportunity.

There are quite a few elections planned for 2025, including Canada, Australia, Singapore, Russia and Germany to name a few. China will have a role to play in global trade this year and we have seen the impact of an advanced AI assistant from Deepseek had on the market in January. Specifically related to REITs, when the news broke on 27 January that Deepseek had new technology which demonstrated performance comparable to leading US models at a fraction of the cost, the Data Centre sector took a punch in the face. Digital Realty (DLR) dropped -8.73% on the news and Equinix (EQIX) was down 4.33%.

For the month of January, the Industrial sector was the top performing sector, delivering 8.56%. This was driven by both performance in Belgium (Warehouses de Pauw +9.90%) and the United States (Prologis +12.82%). Prologis is the largest REIT in the world and reported its fourth quarter 2024 earnings in January. PLD’s EPS beat for the fourth quarter and the market reacted, raising the stock by 7.12% on the day. There was a pull back the following day of -1.83% but then it rose again by 2.96%. The stock has been gaining momentum, and it has a strong growth trajectory, with core funds from operations (FFO, widely considered the most important profitability line item for REITs) rising by 10% year-over-year. The results triggered several analyst updates, such as Evercore and JP Morgan Chase. Another sector to mention for the month was Healthcare, where Welltower, the second largest REIT in the Index, delivered +8.29%.

The worst performing sector was Data Centres, where Digital Realty (DLR) took a hit from the Deepseek-V3 AI assistant news shaking Silicone Valley during the month. The reason behind the drop is the performance capability and the cost at which this technology is created compared to its US peers. The Nasdaq Composite declined -3.4% on the day and big US tech companies were all taken by surprise by the new kid on the block. American Homes 4 Rent (AMH) was the second worst performing stock in the Portfolio for the month after DLR as explained above, down -7.46%. Apartments was one of the overall worst performing sectors for the month.

When looking at the global regions for the month, Spain (+9.45%) and Mexico (+8.04%) was the best performing regions. They are however very small and if we look at regions over 2% Australia (+7.36%) and Japan (+5.095) were stand out regions. The worst performing regions were Hong Kong (-2.58%) and Canada (-1.69%). The US, which is the largest component of the Index, making up 75.71% delivered 1.77%. The portfolio delivered excellent performance above the Index constituents in Japan through Mitsui Fudosan (+12.66%) and in France through Unibail Rodamco Westfield (+11.96%).

The US Annual PCE inflation accelerated for the third month in a row to 2.6%. This was in line with the expected consensus reading for December. This is the highest it has been in seven months. Interesting to note is that the PCE Price Index Annual Change in the United States averaged 3.29% from 1960 until 2024, reaching an all time high of 11.60% in 1980 and a record low of -1.47% in 2009. PCE Price Index provides a measure of the prices paid for domestic purchases of goods and services while the Consumer Price Index assumes a fixed basket of goods and uses expenditure weights that do not change over time for several years. The Federal Reserve currently uses the PCE data as its main gauge of inflationary data. The unemployment rate in the US for December dropped from 4.2% to 4.1%, below the consensus expectation for it to stay at 4.2%.

The Federal Reserve kept the Fed funds rate steady at 4.25% during their meeting at the end of January 2025, in line with expectations. This was the first pause after three consecutive rate cuts totalling 1.00% by the Fed. Chair Powell re-iterated that the Fed is not in any hurry to cut rates, and the pause is to see more progress being made on inflation before further action is taken. Economic activity has continued to expand at a solid pace and the unemployment rate has stabilised at a low level in recent months. The central bank acknowledged that inflation remains somewhat elevated and removed its previous reference to ongoing progress toward the 2% target. The ECB also lowered its key interest rates by 25 basis points in January, based on an updated inflation outlook.

Certain segments of the Real Estate Investment Trust (REIT) market have demonstrated moderate positive performance, which coincides with what appears to be the conclusion of the current interest rate tightening cycle. Historically, REITs tend to outperform broader equities in the aftermath of such cycles. However, there is a growing consensus suggesting that interest rates may stay elevated for a prolonged period. Many central banks have begun reducing rates, and inflation metrics are generally aligning with target levels. Nonetheless, a degree of uncertainty persists, driven by global factors, including the potential for inflationary pressures to resurface. As a result, the precise implications for the global REIT market remain unclear. Nevertheless, we maintain a cautiously optimistic outlook for 2025 as investors in the global REIT space.

Fund positioning remains roughly the same (quality, value, structural trend riders, and blend between offensive and defensive). The REIT market now has an increased appetite for risk in an easing cycle starting to unfold with global central banks starting their rate cutting cycles.

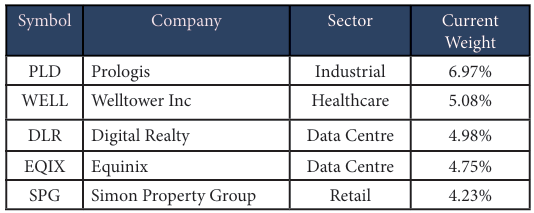

The Tamim global property portion invested in the Reitway Global Property Portfolio currently consists of 49 stocks. Below are the top 5 holdings:

We believe real estate fundamentals are still sound and remain steadfast in our belief that the asset class can post meaningful returns relative to stocks and bonds, even against a slower growth, higher inflation backdrop.

Fund Facts

Investment Parameters

| Management Style: | Active |

| Investments: | Listed property & property related securities |

| Number of securities: | 40-50 |

| Single security limit: | 10% |

| Region limit: | 70% |

| Sector limit: | 70% |

| Investable universe: | Listed property & property related securities |

| Market capitalisation: | N/A |

| Derivatives: | Yes – special instances & hedging |

| Leverage: | No |

| Portfolio turnover: | Typically < 25% p.a. |

| Cash level: | 0-100% (typically 0-20%) |

Fund Profile

| Investment Structure: | Unlisted Unit Trust (available to wholesale investors) |

| Minimum Investment: | $100,000 |

| Management Fee: | 0.98% p.a. |

| Admin & Expense Recovery: | Up to 0.25% |

| Performance Fee: | Nil |

| Hurdle: | N/A |

| Entry/Exit Fee: | Nil |

| Buy/Sell Spread: | +0.25% / -0.25% |

| Applications: | Monthly |

| Redemptions: | Monthly (with 30 day notice) |

| Distribution: | Quarterly |

| Investment Horizon: | 3-5+ years |