Global Equities

Global Tech and Innovation

Below you will find this month’s commentary and portfolio update for TAMIM Global Tech and Innovation Fund.

January 2025 | Investor Update

Dear Investor,

We provide this monthly report to you following the conclusion of the month of January 2025.

For the month of January, the Global Technology & Innovation fund was down just over 1%. For context, the Nasdaq (QQQ) was up 2%, the Semiconductor Index (SOXX) was up 1%, and the Technology index (XLK) was down 1% in January. Taking a step back, since the July 2024 peak*, the Semiconductor index is down 20% and the Technology index is down 3% – it’s clear there has been significant rotation underneath the surface. In a section below, we update our views on market concentration, which we first called out in our June update (published in mid-July) – with the summary being:

- Market-capitalised weighted US indices are increasingly risky given the highest ever concentration levels

- There are plenty of opportunities underneath the surface, notably in areas that have been depressed by higher interest rates

- Stock-selection and active management will likely be a lot more important over the years ahead

As noted in the last update, our exposure was relatively light coming into 2025 as we awaited more clarity on the order of policy priorities. We began to ramp exposure back up in mid/late January – a portion of which (AI exposure) was negatively impacted by the DeepSeek news, discussed further below in our Technology update. We used this sell-off as well as weakness in early February to further increase our exposure – now expanding our Technology bucket to include Phase 2 of the AI cycle, AI Applications (e.g., Software, Biotech).

On the geopolitical front, this new administration in the US has hit the ground running with their executive orders, policies, and clear mandate – executing the Agenda 47. We expect a lot of volatility in the market in 2025 – which should present many opportunities for active managers. And we’ve built this strategy to capitalise on the confluence of these massive, once-in-a-generation shifts – which we have been studying and preparing for for years – that are set to accelerate in 2025/2026.

We reiterate that this current administration provides both clarity to our focus areas as well as accelerants to our thematic views – many of our expectations in our election video from November are coming to fruition. We remain focused on investing in Artificial Intelligence (AI) – which is a critical area for both deterrence and productivity – as well as US onshoring and reindustrialisation – which Trump plans to incentivise via tariffs. What is quite clear is the focus on investing in productivity and efficiency (i.e., Technology-first agenda, spearheaded by Elon Musk) and hitting the ground running – which we already see and expect more in his first 100 days. In the background, liquidity injections are picking up again via the TGA drawdown in the US, while China is seemingly awaiting further fiscal action until there is clarity on Trump’s plans. We believe all of these policy actions are inter-linked and are being used for geopolitical negotiations which likely accelerate in April/May – this all foots with our broader holistic framework laid out in our fund docs. In the weeks ahead, we will publish some updated predictions on what we expect over the coming two years – which we expect will be the most compressed change in human history.

Delving into a quick update on the pillars of our strategy:

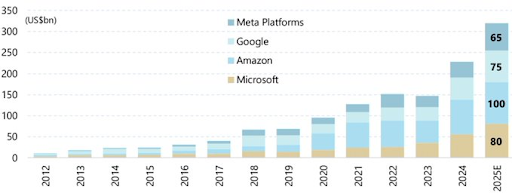

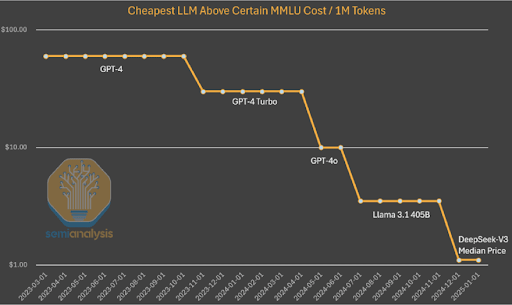

- Technology – The DeepSeek news, which we will also cover in an upcoming video update on AI, signifies a few notable items: a Sputnik type moment in the ongoing US/China Cold War and a transition acceleration from Phase 1 to Phase 2 in the AI cycle. As a reminder, Phase 1A (our labelling) was the base compute layer build out for AI – essentially rearchitecting data centers compute layer away from CPU toward GPU for AI applications; Nvidia was by far the biggest winner here. We noted the peak of that portion of the cycle back in ~June/July 2024 – since that peak, NVDA is down ~10%. This does not mean that Phase 1A is over – the build will continue for years – but rather that the growth will continue to decelerate, and the focus has shifted to the next ‘bottleneck’ area – networking, Phase 1B. That shift toward 1B began to pick-up steam in the 2H24 – mentioned in our updates throughout and our call in November. We now believe phase 1B is in the process of peaking, with a shift toward phase 2 – AI applications, which should benefit the users of AI (notably the application builders/layers). On the technological front, DeepSeek’s main innovation is around unique implementations of reinforcement learning and mixture of experts – with the simple summary being AI costs should go down, which likely means usage will go up. Known as Jevons Paradox, this is typical behavior in commoditised areas, notably energy – and we believe we are getting closer to commoditising base AI, similar to the Internet, which will enable a Cambrian explosion of companies built on top. All of the Western players (OpenAI, Anthropic, etc.) have or will release similar models in the coming months that implement these learnings (all open-sourced), which should further accelerate cost declines and expand the AI application market (Phase 2) – starting on the software side then eventually moving to robotics/hardware (Phase 3). Cloud players’ capital expenditure plans (below) on AI also hint that they believe lower AI costs will likely lead to more demand.

We have shifted our portfolio toward Phase 2 winners, while maintaining some Phase 1B exposure. On the geopolitical front, DeepSeek was likely purposefully timed around the inauguration as a show of Power by China – we are in Space Race 2.0 which forces an acceleration of investment toward asymmetric technology. Once again, our Pillars of Power framework at work. For our bigger picture views on AI – the primary focus of our Technology pillar – check out prior updates.

- Energy, another major pillar of power, is a critical input into any system — the base layer for both Technology and Money. In order to power the AI data center demand + reshoring in the US + electric vehicle proliferation, we need to both increase reliable base load power (i.e., nuclear and natural gas) and upgrade the grid. We are beginning to see signs of this cycle emerging in the US: Amazon buys nuclear powered data center to accelerate AI, Microsoft partnering to re-open the ‘infamous’ 3-mile island nuclear power plant to power its AI data center, Google to buy power from small modular reactor company, Palisades Michigan nuclear power plant potentially reopening supported by the Department of Energy. And under the Trump administration we expect ensuring cheap, reliable energy will be a key focus – as they fully understand that without reliable, inexpensive energy, you cannot have industry. His selection for the Department of Energy – Chris Wright – is an excellent sign; we finally expect US innovation and creativity to infiltrate the energy space, creating huge opportunities for our sub-universe. Further, we expect energy supply chains to decentralise – meaning, a lot of these large data centers will be off-grid, utilising their own separate power sources (likely natural gas and some nuclear) so as to not strain the public grid.

- Money – the final pillar of power – is critical but often overlooked, as it helps store energy and finance Technological progress. The US is in a uniquely powerful position with the US dollar as the global reserve currency — which is the foundation of the current interconnected global system. And to better leverage the system, the US is contemplating launching its own Sovereign Wealth Fund — which would potentially be a massive boon for Tech and Energy investment and progress. This is the base premise of our Fund and our three pillars of power – the West needs to accelerate investment (Money) in critical areas (notably key Technology and Energy) to maintain and/or expand its Power, which is being directly challenged by China. From the National Security strategy report (US):

-

- “We must complement the innovative power of the private sector with a modern industrial strategy that makes strategic public investments in America’s workforce, and in strategic sectors and supply chains, especially critical and emerging technologies, such as microelectronics, advanced computing, biotechnologies, clean energy technologies, and advanced telecommunications.“

Overall, the above are positive signposts for our thesis and should provide further tailwinds for our themes and universe – and we believe the Trump administration will likely accelerate essentially all of these themes (notably, US reshoring and AI) as they are deeply focused on the Pillars of Power we’ve created. Check out our latest webcast for a refresher on the global backdrop, the Pillars of Power, and the path ahead. We are incredibly excited about the opportunity set that lies ahead given where we are within this technological innovation wave, and what must happen on the global landscape front.

Portfolio Highlights

Confluent (CFLT) is a leading provider of data streaming platforms, specialising in real-time data processing and integration solutions based on Apache Kafka. The company’s products, including Confluent Cloud and Confluent Platform, enable organisations to stream, connect, and process large volumes of data across various systems in real-time. In the context of AI and supply chain management, Confluent plays a crucial role by providing the infrastructure for real-time data flows that power AI-driven applications. For example, Confluent’s technology enables companies like GEP Worldwide to process billions of events daily for AI-powered supply chain optimisation, including demand forecasting, supplier discovery, and inventory management. By facilitating the seamless flow of real-time data, Confluent empowers businesses to create more responsive, efficient, and intelligent supply chains, leveraging AI and machine learning for improved decision-making and operational efficiency. Further, Confluent’s recent integration with Databricks significantly enhances its ability to provide real-time data for AI-driven decision-making.

Confluent is a new addition to the portfolio this year, spurred by our view that we are shifting into Phase 2 of the AI cycle – with a focus on AI applications. As mentioned above, the early winners of the combination of ‘cheaper but better AI’ will be companies within the application layer – notably those that can quickly scale it across their organisation. While it will take a bit longer to scale it in the physical world (i.e., edge smartphones), it will be much faster in the digital realm – and industries like Software and Biotechnology are well positioned. Confluent falls into the Software side of this, and we believe that they are particularly well positioned to utilise their positioning in data streaming to enable scalable inference and AI agents.

Tesla (TSLA) is a pioneering electric vehicle, clean energy, and automation company that has revolutionised the automotive industry through its innovative approach to manufacturing and holistic vision of the electrification, automation, and robotics spheres. The company designs, develops, manufactures, and sells high-performance electric vehicles, solar panels, energy storage systems, and robotics. In the electrification supply chain, Tesla has vertically integrated many aspects of production, including battery cell manufacturing, to reduce costs and ensure supply (a similar approach as Apple in smartphones). For automation and robotics, Tesla heavily utilises advanced manufacturing techniques in its factories, employing sophisticated robots for tasks across the end-to-end process. The company’s commitment to automation extends beyond manufacturing to its vehicles, with Tesla a leader in developing autonomous driving technology (with a vision-first approach). Tesla now has over 5 millions vehicles on the road. These vehicles are essentially robots on wheels, gathering data. And, when they are ready, they can basically flip a switch and overnight these cars can become partial or full self-driving. Additionally, Tesla is expanding into humanoid robotics with its Optimus project, further solidifying its position in the robotics supply chain. Through these initiatives, Tesla has positioned itself as a central player in the intersection of electrification, automation, and robotics, driving innovation across multiple industries.

Tesla will be a key winner in the later stages of Phase 2 and into Phase 3 of the AI cycle – signals of which will arise as we progress through this year as full self-driving goes more mainstream (Austin robotaxi launch in June). Only BYD in the East, and Tesla in the West have cost structures that we believe will be competitive in this “new world” order. As we’ve laid out historically, we continue to think the majority of the other electric OEMs in the space will likely head toward zero — similar to what happened with internal combustion engine OEMs in the early 20th century. The legacy auto OEMs will also end up being displaced over time as well — as electric technology is simply superior to internal combustion and continues to improve. We are already seeing this with Ford recognising how far behind they are, and VW is shutting German factories due to under-utilisation. Further, both Tesla and BYD continue to separate themselves from the pack by now beginning to really lean into the software/AI side of their respective businesses — which will ultimately power their autonomous driving experiences and the surrounding ecosystem. The recent progress on the self-driving front has been notable — across both Tesla vehicles (see step functions improvements in chart below), as well as what’s coming on the humanoid robot front (Elon’s latest robot views) which is a massive multi-trillion dollar opportunity (second chart below estimates). Overall, we believe Elon Musk will help guide the Trump administration to help accelerate automation in the US – given it is both a National Security concern (i.e., China pushing ahead by allowing for autonomous vehicles on the streets) and a potential huge boon for productivity (i.e., imagine all the extra time you’d have if you weren’t driving stuck in traffic). This position had been reduced, but we began to increase it on the latest sell-off.

Kinaxis Inc. (TSX: KXS) is a leading provider of cloud-based supply chain management solutions, offering its flagship RapidResponse platform as a software-as-a-service (SaaS) product. Kinaxis’s solutions address various aspects of supply chain management, including demand planning, inventory management, and sales and operations planning. In the context of automation and reshoring, Kinaxis plays a crucial role by providing AI and machine learning-powered capabilities that enable companies to optimise their supply chains, reduce lead times, and improve responsiveness to market changes. Their tools support the trend towards reshoring by helping businesses manage complex, localised supply networks more efficiently. By offering end-to-end supply chain visibility and powerful simulation capabilities, Kinaxis empowers companies to make faster, more informed decisions, which is particularly valuable in today’s volatile business environment where agility and resilience are paramount.

Kinaxis is a new position in the portfolio and a company that we believe will be a key enabler in the accelerated reshoring agenda of the Trump administration. Simplistically, Kinaxis will help both accelerate the reshoring process and help companies optimise their “new” supply chains in the multi-polar world we are entering.

Market Concentration

We want to provide an update on our views from our initial call in July 2024 that market concentration levels were in the process of peaking.

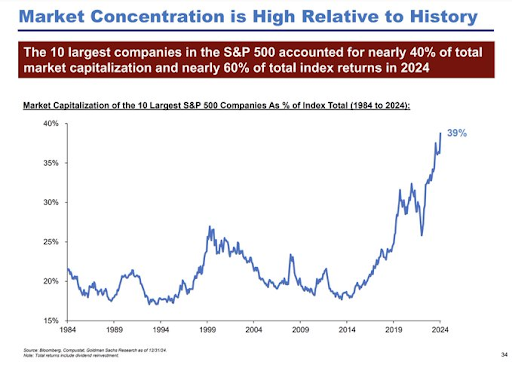

The market-capitalization weighted US indices are extremely concentrated. In fact, they are the most concentrated they have ever been – with the top 10 stocks representing almost 40% of the index (graph below).

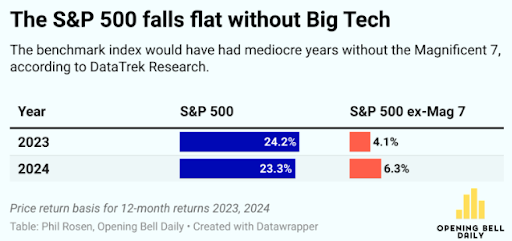

The majority of the stock market gains over the last 2 years has been driven by a few stocks (i.e., Mag-7; see table below).

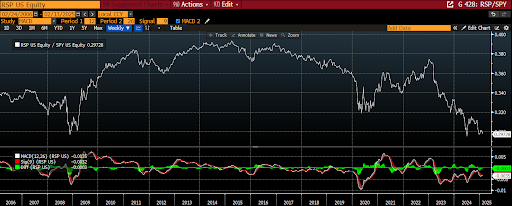

Another way to visualize this same phenomenon is to compare the S&P market-capitalization weighted index (SPY) versus the S&P equal-weighted index (RSP). As you can see in the graph below, the RSP has massively underperformed the SPY since the end of 2022, and is now bouncing around 2008 relative lows. What is interesting, is the equal-weighted index tends to outperform over time – suggesting that stock-picking under the surface may be about to meaningfully resurface.

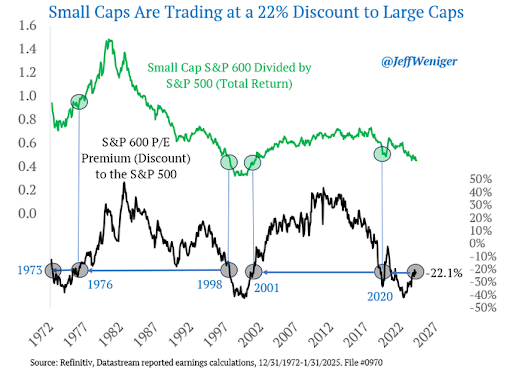

And this is further illustrated by one of the widest divergences ever between small capitalization valuations and large capitalization valuations (see graph below). We believe the majority of this imbalance in the market is a byproduct of higher short term interest rates – similar to the K-shape economy, you have a K-shape stock market. As rates begin to come down, and Trump reshoring policies begin to take hold, this can reverse with avengeance.

Further tying this back to the Technology (AI) cycle, given the significant value and market capitalization generated by Phase 1 (most notably in NVDA and other Mag-7), there is risk that money rotates quickly out of those areas and into Phase 2 as we progress through this year – which would pose a risk to the market, but opportunity under the surface.

Overall, we have concerns around the broader market entering this Spring (~April) due to a confluence of items – from market concentration risks, to tariffs, to an air pocket between Phase 1 and Phase 2 of AI. We believe active management, notably with a framework like the Pillars of Power to contextualize events, will be key.

In summary:

- Market-capitalized weighted US indices are increasingly risky given the highest ever concentration levels

- There are plenty of opportunities underneath the surface, notably in areas that have been depressed by higher interest rates

- Stock-selection and active management will likely be a lot more important over the years ahead

- We are extremely excited about our strategy given this backdrop

Fund Facts

Investment Parameters

| Management Style: | Active |

| Investments: | Global Equities |

| Investable universe: | Nasdaq Composite |

| Number of securities: | 40-50 |

| Derivatives: | Yes |

| Leverage: | No |

| Portfolio turnover: | Typically < 25% p.a. |

| Cash level: | 0-100% (typically 0-20%) |

Fund Profile

| Investment Structure: | Unlisted Unit Trust available to wholesale or sophisticated investors |

| Minimum Investment: | $150,000 |

| Management Fee: | 1.50% p.a. |

| Admin & Expense Recovery: | Up to 0.35% |

| Performance Fee: | 20% of performance in excess of hurdle |

| Hurdle: | Greater of: RBA Cash Rate +2.5% or 4% |

| Entry/Exit Fee: | 5% exit fee is payable on an exit from the investment in the unit class prior to the first year anniversary of the investors initial issue of units. |

| Buy/Sell Spread: | +0.25% / -0.25% |

| Applications: | Monthly |

| Redemptions: | Monthly with 30 days notice |

| Investment Horizon: | 5+ years |

| Distributions: | Annual |