Global Equities

Global Tech and Innovation Founders Class

Below you will find this month’s commentary and portfolio update for TAMIM Global Tech and Innovation Founders Class.

September 2024 | Investor Update

Dear Investor,

We provide this monthly report to you following the conclusion of the month of September 2024.

We have been using the typical pre-election volatility to selectively ramp exposure in the new fund, with a target of near ~full deployment around the US election. With the election less than a month away and the outcome still highly uncertain, volatility in the market remains elevated. Once the official results are in, we expect volatility will likely quickly recede — as certainty (one way or the other) will provide the market with clarity and likely lead to risk deployment and a potential year end rally. In the meantime, we are most focused on investing in areas that both candidates deem important — notably Artificial Intelligence (AI) and reshoring/reindustrialisation, key durable themes for our fund. In the background, liquidity injections have begun to increase, China has outlined various stimulus initiatives, and the Federal Reserve has begun its rate-cutting regime — which has already led to a weakening of the USD, and should help spur a cycle of purchases that require financing (e.g., auto, housing) as interest rates move lower. Overall, we are beginning to see signs of an emerging reflationary backdrop and this forced de-risking in a seasonally weak period (August-October) has created opportunities in areas we are focused on. As uncertainty around the election begins to lift over the coming ~month or so, we expect volatility will likely recede and money will flow back into risk assets.

Delving into a quick update on the pillars of our strategy:

- Technology — most notably, AI — is our primary focus. We continue to believe this Technological cycle will dwarf the Internet, Mobile, and other preceding technological revolutions — and we are already beginning to see hints of this with step-function advancements in robotics, self-driving vehicles, and the automation of many white-collar tasks. While phase 1 of the AI buildout has been primarily focused on Compute infrastructure, we are beginning to shift into phase 2 — with a focus on Networking and Memory, two major bottlenecks that can unlock significant gains, notably on the inference side. With Nvidia’s Blackwell architecture (and partners) now known and launching later this year, along with major cloud data center players finalising roadmaps, we expect investment in these two areas to accelerate and are adjusting our exposure accordingly.

- Energy, another major pillar of power, is a critical input into any system — the base layer for both Technology and Money. In order to power the AI data center demand + reshoring in the US + electric vehicle proliferation, we need to both increase reliable base load power (i.e., nuclear and natural gas) and upgrade the grid. We are beginning to see signs of this cycle emerging in the US: Amazon buys nuclear powered data center to accelerate AI, Microsoft partnering to re-open the ‘infamous’ 3-mile island nuclear power plant to power its AI data center, Google to buy power from small modular reactor company, Palisades Michigan nuclear power plant potentially reopening supported by the Department of Energy.

- Money – the final pillar of power – is critical but often overlooked, as it helps store energy and finance Technological progress. The US is in a uniquely powerful position with the US dollar as the global reserve currency — which is the foundation of the current interconnected global system. And to better leverage the system, the US is contemplating launching its own Sovereign Wealth Fund — which would potentially be a massive boon for Tech and Energy investment and progress. This is the base premise of our Fund and our three pillars of power – the West needs to accelerate investment (Money) in critical areas (notably key Technology and Energy) to maintain and/or expand its Power, which is being directly challenged by China. From the National Security strategy report (US):

“We must complement the innovative power of the private sector with a modern industrial strategy that makes strategic public investments in America’s workforce, and in strategic sectors and supply chains, especially critical and emerging technologies, such as microelectronics, advanced computing, biotechnologies, clean energy technologies, and advanced telecommunications.”

Overall, the above are positive signposts for our thesis and should provide further tailwinds for our themes and universe. We are incredibly excited about the opportunity set that lies ahead given where we are within this technological innovation wave, and what must happen on the global landscape front.

Portfolio Highlights

MACOM Technology Solutions (MTSI) is a leading semiconductor company that designs and manufactures high-performance analog RF, microwave, millimeter wave, and photonic semiconductor products. Their components are critical enablers in various high-growth markets, including data centers, telecommunications infrastructure, aerospace and defense, and industrial applications. In the context of AI/automation, MACOM’s products play a crucial role in enabling high-speed data transmission, signal processing, and wireless communications. Their semiconductor solutions are used in 5G infrastructure, data center interconnects, and radar systems, which are fundamental to the development of AI and automation technologies. MACOM’s power amplifiers, switches, and other RF components contribute to the advancement of next-gen energy technologies and smart grid systems. Additionally, their high-performance analog and mixed-signal ICs are essential for precision control and sensing in robotics applications. By providing these critical components, MACOM supports the ongoing trends in AI, electrification, automation, and robotics across multiple industries, positioning itself as a key player in the semiconductor ecosystem supporting these transformative technologies.

MTSI is particularly well positioned as we move into the next phase of the AI infrastructure buildout — with a focus on resolving the bottlenecks around networking to help improve the compute throughput. MTSI is focused on the high-speed optical interconnects within data centers, which will be part of the solution to continuing to improve the price/performance equation that helps enable the next step function improvement in AI models. In addition, MTSI has secured incremental content in Nvidia’s Blackwell architecture, which should provide a positive tailwind for growth into 2025. Finally, MTSI is a key both a key supplier into the Defense industry and a key enabler of reshoring with their domestic US fabrication facilities — both of which have secular drivers from geopolitical instability and reshoring in the West.

")

ARM (ARM) for central processing unit (CPU) cores and other chip technologies. Their energy-efficient processor designs are widely used in various electronic devices, from smartphones and tablets to embedded systems and Internet of Things (IoT) devices. In the context of automation and robotics supply chains, ARM plays a crucial role by providing the underlying processor architecture and IP for many of the chips used in these systems. ARM’s designs also power many of the AI and machine learning accelerators used in autonomous systems. By licensing their technology to semiconductor manufacturers and system designers, ARM enables the development of customised, high-performance, and energy-efficient processors tailored for specific automation and robotics applications.

ARM is a high quality company that sits at the base layer of semiconductors — providing the software and instruction set that powers essentially all low-power chips. Over the last few years, ARM has increasingly made inroads into the data center — which has historically been dominated by x86 (Intel). Data center, robotics, and automotive are three huge green field growth areas for ARM where they are beginning to see accelerating traction and are well positioned with this fundamental step function change in data center architectures with AI (hence why Nvidia tried to buy ARM in 2020).

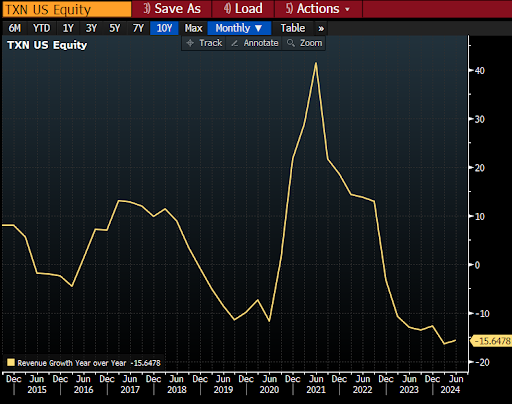

Texas Instruments (TXN) is a global semiconductor company that designs, manufactures, tests, and sells analog and embedded processing chips for various markets, including industrial, automotive, personal electronics, communications equipment, and enterprise systems. Their portfolio includes embedded processors, microcontrollers (MCUs), and connectivity products that enhance computing performance, motor control, real-time communication, and AI capabilities. TI’s technologies are integral to the development of smart, efficient, and safe robotics systems, as demonstrated by their role in Amazon Robotics’ autonomous mobile robots. Additionally, TI’s power conversion, sensing, and control solutions support next-gen energy systems, contributing to the broader trend of electrification. By offering scalable, high-performance, and cost-effective semiconductor solutions, TI plays a pivotal role in advancing the capabilities of automation and robotics across various industries.

As the graph illustrates below, TXN revenue has been in a protracted downcycle over the last ~2 years, and unsurprisingly the stock has been rangebound as a result. On top of the downcycle in revenues (primarily industrial and automotive exposure, both of which are in the process of ~bottoming), TXN has been investing heavily on the capex side to further build out its domestic (US) 300mm fabrication facility capacity. While in the short run this capex suppresses TXN’s free cash flow, over the medium term it will further solidify its competitive advantage with local, resilient manufacturing capacity (reshoring beneficiary) and enhance gross margins and its cost structure advantage (300mm huge advantage in analog over 200mm wafers). Overall, they are particularly well positioned to capitalise on the next upcycle.

Fund Facts

Investment Parameters

| Management Style: | Active |

| Investments: | Global Equities |

| Investable universe: | Nasdaq Composite |

| Number of securities: | 40-50 |

| Derivatives: | Yes |

| Leverage: | No |

| Portfolio turnover: | Typically < 25% p.a. |

| Cash level: | 0-100% (typically 0-20%) |

Fund Profile

| Investment Structure: | Unlisted Unit Trust available to wholesale or sophisticated investors |

| Minimum Investment: | $150,000 |

| Management Fee: | 1.50% p.a. |

| Admin & Expense Recovery: | Up to 0.35% |

| Performance Fee: | 20% of performance in excess of hurdle |

| Hurdle: | Greater of: RBA Cash Rate +2.5% or 4% |

| Buy/Sell Spread: | +0.25% / -0.25% |

| Applications: | None |

| Redemptions: | Monthly with 30 days notice |

| Investment Horizon: | 5+ years |

| Distributions: | Annual |